Business savings accounts can be a great way to add extra profit to your business. Here’s all our top options (and research criteria just below).

Get top saving rate

4.61% AER with BlackRock Money Market Funds. T&C’s Apply. Capital at risk. The provider of investment services is Lightyear Financial Ltd for the UK and Lightyear Europe AS for the EU. Seek qualified advice if necessary.

Lightyear offers simple ways to buy and trade UK, EU and US assets, earn interest and invest in low-risk, high liquidity money market funds. With Lightyear you can manage your business’ money with Money Market Funds that are low risk, highly liquid and AAA-rated investments that pay interest.

You can add and withdraw money instantly to your cash account (in rare cases, your withdrawal will be processed the next business day), and there’s no minimum deposit. The fees are low, and already accounted for in the rate advertised.

The website and app itself are pretty awesome, and very easy to use.

• Awesome mobile app

• Can also use their website (web app)

• Low trading fees

• Low cost overall

• ETFs are commission-free

• Multi-currency account

• Great interest rate on uninvested cash

• Business account

• Not commission-free

• Not a huge range of UK stocks (although over 250)

• No Stocks & Shares ISA

• No personal pension

• No live-chat support

There’s a good range of investment options (over 3,500 stocks and ETFs), you can store multiple currencies, and the app itself is modern and super slick.

ETFs are commission-free, and stocks are £1/$1/€1 per order. There's also very low currency conversion fees of 0.35%, or you can hold the currency itself, and avoid this fee.

Get a great variable return with money market funds. T&C’s apply. Capital at risk.

InvestEngine is easy to use and very low cost.

• Easy to use

• Very low cost

• ISA and GIA are free

• Pension is 0.15% per year (maximum £200)

• Commission-free

• Great range of ETFs

• Experts can manage your investments

• Business account available

• Great customer support

• Only ETFs (but a wide range)

• No financial advice

InvestEngine is one of the cheapest investment platforms out there, and a great range of investments too (ETFs only).

There’s no fees at all if you want to manage your investments yourself with an ISA or a General Investment Account (GIA), and a super low fee of 0.25% if you want their experts to handle things.

For a pension, it’s only 0.15% per year (with a maximum of £200).

And, there’s no commission to buy and sell investments.

Plus, they offer a business account too (no fees).

It’s more than just low cost though, there’s some great features to help you invest, and the customer service is excellent.

Minimum deposit: £100

Get £175 free cashback*

£75 with business account (deposit £100) and £100 with a saver account (deposit £5,000). Code NUTSABOUTMONEY. T&Cs apply.

Tide is a super popular business account – with over 10% of all small and medium sized businesses in the UK with accounts, including tonnes of freelancers and contractors (and there’s over 1 million businesses using Tide globally).

It’s an easy to use and straightforward account that is free to open. You simply pay as and when you use it (e.g. a small fee per transaction), and the fees are low overall.

The app itself is great, and although it’s easy to use, it’s packed with features to help you manage your business finances and admin, such as invoice management, expense cards, accounting integrations, admin tools and more.

You can even find loans suitable for your business, and if you’re an in-person business Tide has a range of payment solutions available such as card reader terminals, tap to pay and payment links to take payments.

You'll also get a business savings account with one of the highest savings rates out there, perfect for any extra cash you might have lying around, and you can send money to and from your Tide current account and savings account in seconds whenever you need it.

• Free account (paid plans with more features)

• Low cost overall

• High interest rate on savings

- Apply in minutes

• Free debit card

• Great mobile app

• Accounting integrations

• Take payments in-person

• Often quick to open

• 24/7 in-app support

• £1 ATM withdrawal cost

• Can’t receive or hold multiple currencies

• £2.50 fee for cash deposits (or up to 3% through PayPoint)

*Get £75 for free after spending £100 within 30 days, and an extra £100 when depositing at least £5,000 into the savings account and keeping it there for at least 2 months. Use the code NUTSABOUTMONEY when registering to claim your cashback.

Flagstone is a savings platform that brings together a wide range of the top savings accounts in the UK, into one single Flagstone account, allowing you to always get one of the best rates possible, without having to keep switching accounts, or apply directly to a bank.

You simply have one Flagstone account, and can pick and choose where to put your savings. You can keep your money with multiple banks at the same time too.

• Always be on a top savings rate

• Wide range of banks available

• Pick from easy access to fixed term

• Easy to use

• Split your money across banks

• Business customers must start with £100,000 (£10,000 for personal customers)

• Not every bank available

Wise business is the best option for multiple currencies. Send and receive money in over 40 different currencies, including Euros and US Dollars, all for a low cost (it’s the cheapest option).

You can even store multiple currencies in one account, meaning you don't have to keep swapping currencies and paying exchange fees.

Another great feature, is being able to save and invest your business money, so instead of your money sitting in your account doing nothing, you can invest it to grow more over time (with the help of experts) – adding a whole new revenue stream to your business – and still allowing you to spend it whenever you need to.

• Bank transfer cost: From 0.43% to send. Free to receive

• Free ATM withdrawals (up to a limit £200)

• Hold multiple currencies (40+)

• Free debit card

• Accounting integrations (like Xero)

• Save or invest cash

• Set up fee (£45)

• No cash deposits

Revolut is a modern business account designed to suit modern day businesses – unlike traditional banks that run on slow and outdated systems and processes.

Revolut have thought of everything, and the app is packed out with many helpful tools and features to help grow your business. And easy to use.

It’s pretty much perfect for every size of business, from a freelancer to large enterprises.

• It’s low cost (free to £100 per month)

• Free bank transfers (up to a limit)

• Free ATM withdrawals (up to a limit)

• Hold multiple currencies (25+)

• Debit card

• Accounting integrations (like Xero)

• Save or invest your business cash

• No cash deposits

It’s also great for international businesses, and receiving payments in different currencies, such as customers based in Europe, paying in Euros. You can hold over 25 different currencies inside your Revolut business account – you can swap one currency for another in a couple of clicks, for a low exchange rate too!

You can also receive payments from customers in-person without needing a card machine, and online without needing other software, and even via text messages.

And, there’s loads of extra features you wouldn’t expect from other accounts, such as payroll and invoicing features, and team expense management.

It’s got pretty much everything you need, and more. Highly recommended.

Note: it’s not technically a bank, it’s an e-money account. Your money is still just as safe and secure.

Stacking up the cash in your business bank account and keen to make the most of it? You’re in the right place. Business current accounts aren’t great for growing your money from either earning interest (or investing it), they’re designed to manage your cashflow, sales and operating costs.

Business savings accounts on the other hand can be great at adding extra profit to your business, all for no extra work – as long as you’ve got spare cash in the business. And, some have very high interest rates (some of the best out of there).

We’ve reviewed all the top options for your business savings to put together our list of the best accounts – seeking out the very best interest rates for businesses (among other criteria, listed below).

Oddly, there’s a lot less options for business savings than there are for personal savings, and some are pretty hard to find, but we’ve done the research to find the top options for you, and narrowed our list down to suit businesses of all types.

Here’s the criteria we looked at:

That’s a pretty long list, but making sure your business money is secure, in the right place and earning the most it can is likely your top priority.

So, you can be confident that picking an option from our list means your business cash will be in one of the top options for UK businesses.

Interested in learning more? Here’s our full review methodology and how we test.

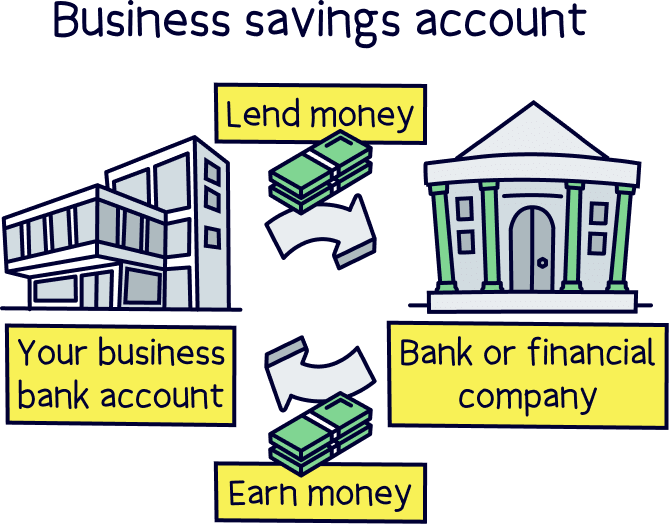

You’ve probably guessed it, but a business savings account is somewhere to put your business cash and earn money in return. To clarify, the cash must be in your business’s name, rather than your own name (e.g. currently in your business bank account, rather than your own personal bank account).

The business savings account will be opened in your business name only, not your personal name – although you will be required to provide your own name to open the account as a director of the business. And, you can have multiple people with access to the account, for instance if you have multiple directors, or for your accountant.

They often work just the same as a personal savings account once it’s up and running. For instance, you add money and earn interest, and withdraw money later down the line when you need it for your business.

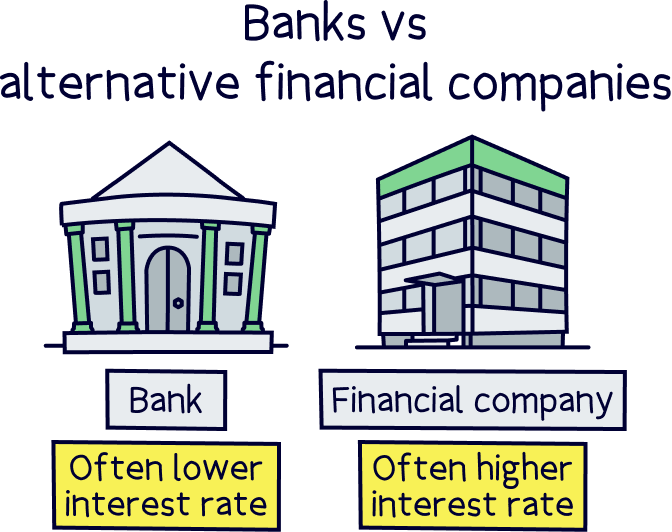

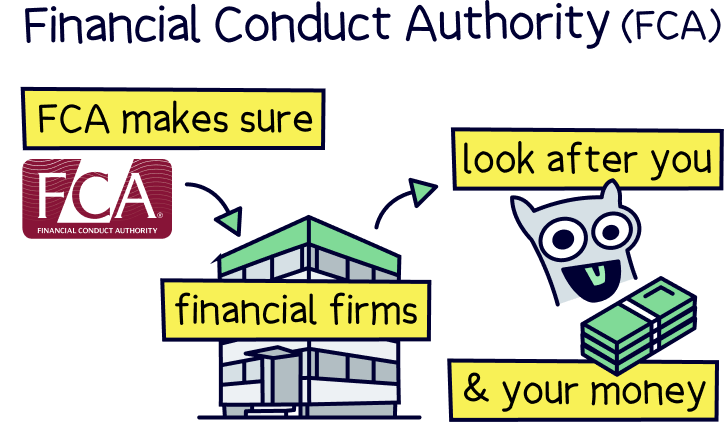

You can get business saving accounts through banks but their interest rates aren't usually the best. An alternative option is to get an account through other types of financial companies, which aren’t technically banks, but authorised by the Financial Conduct Authority (FCA) to look after your business’s money safely and securely (more on that below).

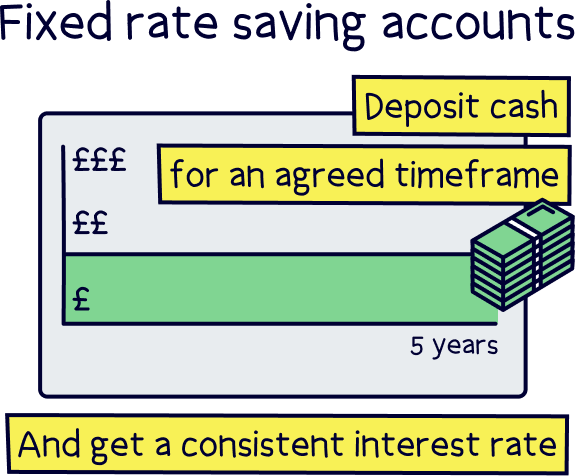

A fixed rate savings account is where you deposit your cash in return for locking it away for a set period of time in exchange for a fixed amount of interest. This might be 6 months, 1 year, 2 years, 5 years and even 10 years.

Typically, these are seen as earning a higher interest rate than accounts where you can get your cash back straight away (easy access accounts), but it’s not actually always the case these days, and you can actually find some of the highest rates with easy access accounts (more on those below).

Note: you can always get your money back, but it may cost you heavily in fees.

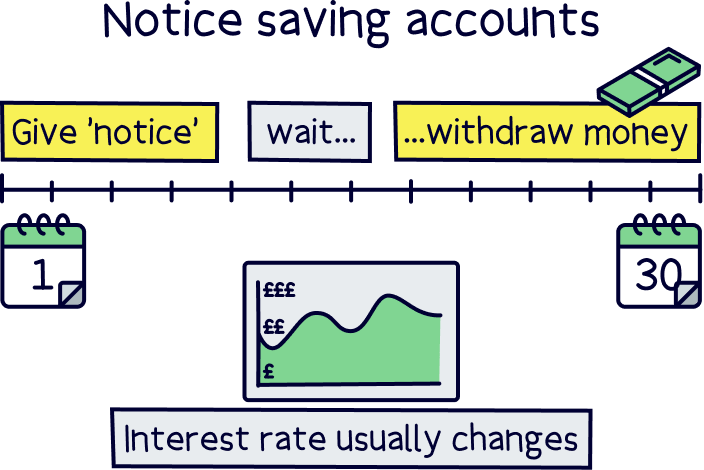

Notice accounts are where you’ll need to give ‘notice’ to get your money back, which is letting the bank know you want your money back, and this is a set number of days (agreed when you open the account), which could be 30 days, 60 days, 90 days or even longer. So, you’ll give notice and then have to wait for the agreed time before you can withdraw the money.

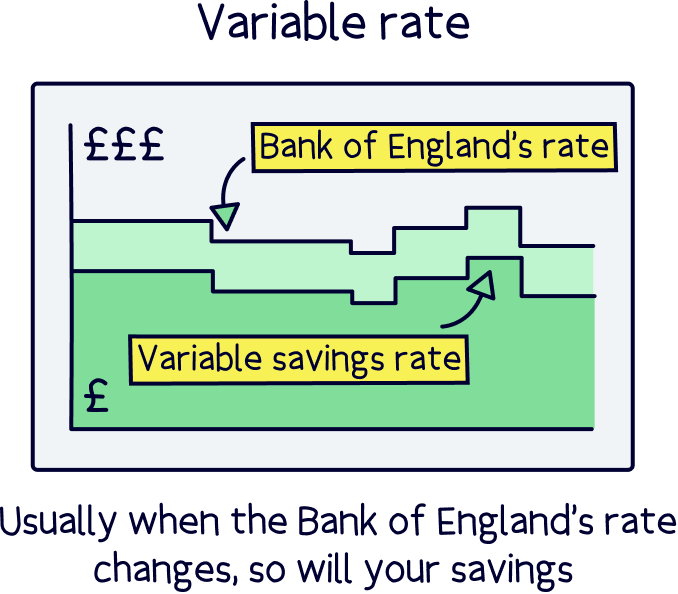

The rate will typically be variable, meaning it can change up and down over time (more below).

Note: you can always get your money back, but you’ll pay a penalty fee.

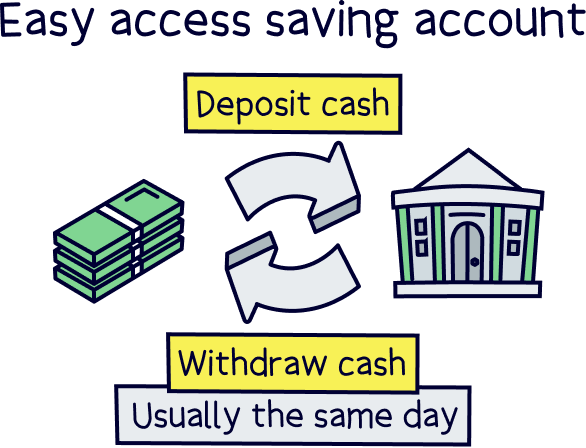

An easy access account is currently one of the most popular types of savings accounts, as you can get your cash back whenever you need it (usually the same day or the next working day) – something a business will probably want to have, just in case.

So, you can deposit cash whenever you want, almost immediately start earning interest, and then withdraw it as and when you like.

The rates you can get vary depending on the bank or financial company, but can be some of the very top rates you’ll find – and they’ll be variable rates (so change over time, more below).

Nuts About Money tip: Lightyear¹ tops the list for the top interest rate with their easy access account – and it’s easy to set up and use, with a great app to manage things.

With a variable rate account, the interest rate isn’t set (fixed) for a period of time, it can change over time, both up and down – this is either decided by the financial company themselves, or if you’re saving within a money market fund, the fund will earn more or less (explained below).

The rate typically moves up and down when the Bank of England base rate changes, which is the interest rate set by the Bank of England and is the saving rate banks earn for storing their money with the Bank of England.

So, if this goes down, all of the banks tend to put the interest rate you get down too. And if this goes up, usually they'll put the rate up too (or sometimes they will be cheeky and pocket the difference until they’re forced to by competition or financial regulators – which is a reason why money market funds often have better interest rates, as the rate isn't dependent on the bank’s good will. Again, more on those just below).

Variable rates are more typical with easy access accounts where you can get your money back whenever you like (rather than locked away for a period of time).

Savings accounts with a bank are where the bank itself holds your money and pays you a set amount of interest, either monthly or annually (although the interest rate can change).

The interest rate is typically lower (and often much lower) than a savings account with an alternative financial company, and often for no extra security or safety (just the perception of it).

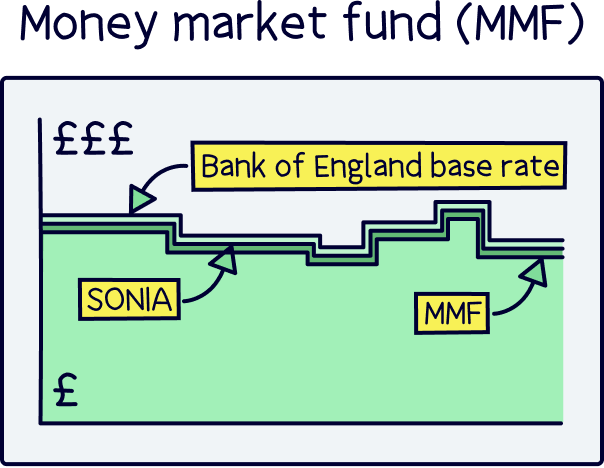

With an alternative financial company, such as an investment platform, the company itself often won’t hold your money directly, but partner with or arrange another company to hold and store your money and pay you interest, which could be a bank, or more commonly, to get the highest rates, they can arrange your cash to be invested in a ‘money market fund’...

A money market fund is where your money is pooled together with others, and this money is invested in places that provide interest in return, and often a very competitive interest rate (often the very best possible, close to or equal to the Bank of England base rate) – and the money is kept as cash, or things very similar to cash (called cash equivalents, more on those below) – it is not invested in things like stocks and shares, where your money can go up and down in value daily (although typically trend higher over time).

For instance, it could simply be stored with a bank that pays a high interest rate for large sums of cash, or it could be things like buying Treasury bills, which is lending money to governments (like the UK government) in exchange for interest (often seen as a very safe investment as they’re guaranteed by the government).

Note: money market funds are hugely popular with businesses, and each fund often has billions of pounds within it (lots of businesses' money pooled together). The funds themselves are managed by large investment companies and banks (such as HSBC and Legal & General).

With a money market fund (MMF), the fund is able to turn money back into cash very quickly, and investors can get their money back whenever they like – making them a great flexible option for both personal savings and business savings.

Nuts About Money tip: if you’re interested in using a money market fund either for business cash or your own cash, check out Lightyear¹, it’s got a top option for both. Or, learn more with our guide to the best money market accounts.

Business savings accounts that simply hold your money themselves and give you interest in return are typically free (often banks) – but they do earn money using your money, it just works differently to a fee you pay. Typically, they’ll earn interest on your cash themselves, and then pay you a part of it. And if they’re a big high street bank, it’s often a very large amount for themselves, there's a reason they're worth billions!

With an alternative financial company who arranges your money to be saved in a money market fund to earn interest, such as an investment platform, there will often be a fee from the business savings account provider, and a fee within the fund itself – however both of these aren't typically very much, and are often a percentage per year of how much you have saved (e.g. 0.25% of your savings per year). Meaning this usually works out as a higher interest rate compared to a high street bank savings account, even when the fees are accounted for.

With a business savings account, it all depends on which provider you’re using. Some have minimums of just £1, and some have minimums of £100,000, and some even £250,000+.

Yes, some accounts will only let you save up to a certain amount, this can be quite low for business funds, from £50,000, or more commonly £250,000 to £1,000,000. Although there are lots of options for higher balances.

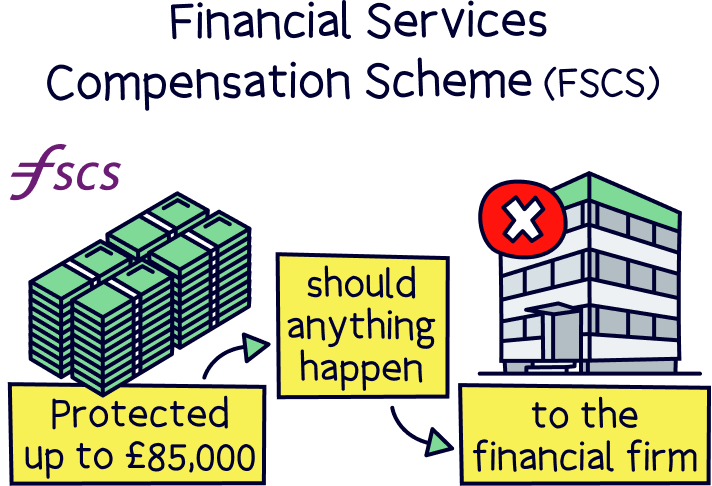

You don’t have to have just one business account however, you can have a full range, and a good strategy for some businesses with lots of cash is to save up to £85,000 in each account, and have multiple accounts, to ensure they’re fully protected by the Financial Services Compensation Scheme (FSCS).

Having said that, there aren’t any limits with a money market fund account, as you can typically save and invest as much as you like into a fund, and you don’t necessarily need to worry about FSCS protection (more below).

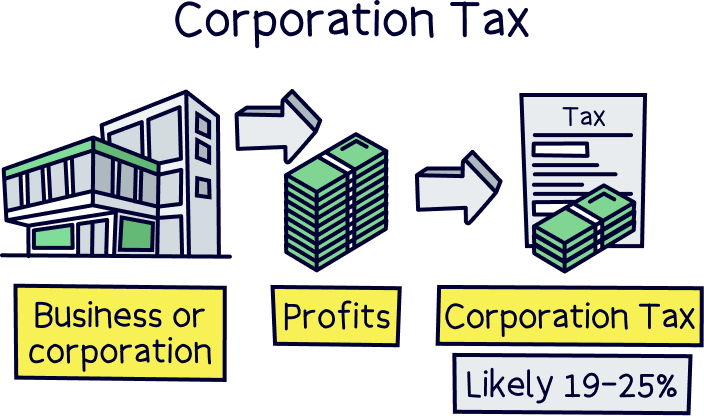

Typically yes, your business will be taxed on the interest you earn, interest is normally paid ‘gross’, which means before any tax is taken off so you will have to pay it.

The amount of tax you’ll actually pay depends on your business, but is likely to be between 19-25% depending on your total business profits, and the tax is called Corporation Tax. Your accountant should be able to help with this if you have one.

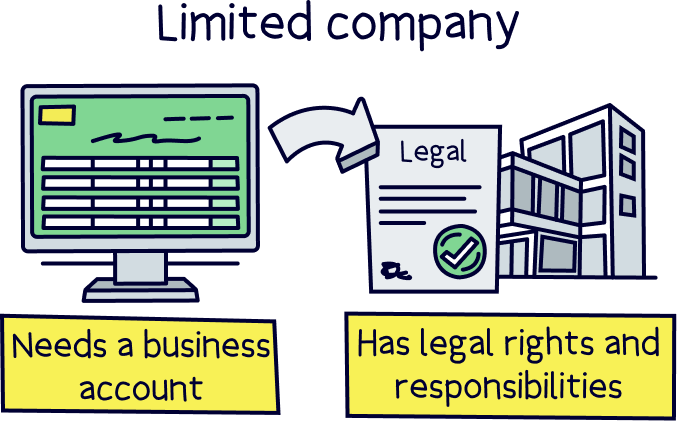

If you’re a sole trader, so running your business under your own name, rather than a limited company (where the company itself is a legal entity), you can still save your business cash, and you technically have more options as you could either open a business savings account, or use a personal savings account too.

Although, from an admin point of view, it’s likely better to keep your business and personal finances separate and open a business savings account for your business cash – as you’ll need to manage your accounts, track the interest and pay the required tax.

Note: some banks won’t let you open a business account unless you are a limited company.

Yes, business bank accounts in the UK are perfectly safe to use.

All UK business bank accounts need to be approved by the Financial Conduct Authority (FCA), who are responsible for making sure financial companies are looking after your business’s money. They need to follow strict rules about how your money is saved, even if they’re not a bank.

This also means your money is protected by the Financial Services Compensation Scheme (FSCS), which protects your business money up to £85,000 should the company holding your money go out of business and not return your money, such as a bank.

However, if your money is in a money market fund, these work a bit differently. If the savings account provider were to go out of business, your money would still exist within the fund itself, with your money assigned to your business, and only your business can access it. Your money would either be returned to your business or transferred to an alternative provider.

If the fund provider itself were to go out of business, and if it’s based in the UK, you may be covered by the FSCS scheme. However, the money in the fund isn’t accessible by the fund provider (to use for themselves if they run into financial problems), the fund would typically be closed down and your money returned to you.

That’s it for the best business savings accounts – there’s a range of options out there, but not too many with great rates, or suited to all types of businesses.

You’ve got two main options, either a fixed rate savings account, where the interest rate remains the same for the duration of the time you lock your money away for, or you can opt for an easy access account where the interest rate can change (it’s variable), but you can get your money back whenever you like (often a good idea for a business).

And with the easy access option, you can opt for a traditional business bank savings accounts, where you’ll get the interest paid by the bank, or a more modern option is with an alternative financial company, where you can save your business cash within a money market fund, and get one of the best rates possible (often near the Bank of England base rate).

We’ve got all the top options above. As a recap, our top pick is Lightyear¹, it’s got one of the best rates out there for businesses, it’s easy to use, and there’s a great app to manage things on the go (it’s great for personal savings too).

Happy saving!

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things banking, cards, and spending and receiving money, for both individuals and businesses – with many years of combined experience writing about it. Some of our team were top financial advisors. We know how to save a small fortune in fees, and how to find the right card and account for you.

More than 20 years of combined experience researching and writing about banking

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of financial companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Lightyear has one of the best saving rates for businesses and the app is great.