Our mission here at Nuts About Money is to give you the confidence to make the right money decisions for yourself – not having the right knowledge and confidence could mean you're financially worse off over time. For instance, your savings might not be in the best place, but you aren’t confident about switching to a new savings account with a better rate, or you might not get the best mortgage deal, or your pension could be with a better provider… The list goes on.

Our reviews give you a central place where through our transparent, impartial and consistent rating framework (system) and criteria, we hope, means you are able to rely on our ratings to give you a solid indication about a company or product.

We also hope we’re able to introduce you to lots of new companies that you might not be familiar with, as often these smaller, or less well known companies provide a better service for you than the high street banks, or old stuffy financial companies with large brands (although some of these have kept up with the times, many have stayed in the past relying on people not switching)...

For instance with modern companies, you may get better savings rates, it’s easier to manage your finances, better mortgage rates, again the list goes on – we’ve thoroughly vetted and reviewed every company that we feature, and shopping around often pays off big time when it comes to financial services.

And just to note, our reviews and opinions are our own, and not specific recommendations or advice for your own personal circumstances, but we hope you'll gain the confidence to make your own money decisions.

Note: if you need personalised advice, speak to a financial advisor.

We offer a range of ‘best buy’ tables, for instance ‘best savings accounts’, and articles featuring companies that could be a good option for you, and we also provide in-depth reviews on specific companies and their products and services.

For our reviews and each of our tables, we look at 4 different key criteria, based on which topic it is (e.g. mortgage brokers). These are scored from 0.1 to 5.0.

As an example, if a company doesn’t charge any fees, it will be rated 5.0 for fees. If a company has bad customer service it could be 1.0, for a good service it could be around 3.5 and for excellent customer service it's nearer to 5.0.

From there, we combine the total for each rating, and then work out the average for an overall rating of out 5. For instance, 4.0 for experience, 4.5 for mortgage range, 3.5 for fees and 4.0 for customer service would give a total of 16.0, and therefore an overall score of 4.0 out of 5.

This method means we’re able to go in-depth on each specific factor (e.g. customer service), giving us the ability to have a wider range of scores, so we are able to suitably differentiate between all the different financial companies and their service for that specific factor (explained below). This allows us to properly assess and determine the best of the bunch.

Getting technical for a moment, the factors included within our review framework (system) are mostly qualitative, meaning they’re based on the outcome of our research and our experience of using the service and company we are reviewing (rather than relying solely on numerical or objective data (called quantitative data)).

Although saying that, we do use quantitative data where we can, such as when it comes to savings rates, and fees. So it’s a bit of both really.

We review each company and their rating for each specific factor at least every 3 months, to ensure that the companies featured are maintaining the high standards expected of achieving a high score – so you can be sure that our tables are up to date, and be confident in making the right decision for you.

Note: this means companies in our tables and pages can move around from time to time.

Sometimes, you may see the rating as a whole number (rather than say 4.3 out of 5), to make things easier to display and readers to quickly understand. In that case, we’ve mapped the more accurate rating to a whole number (or stars), and here’s how we do it:

We typically look at 4 key criteria for each category of companies or products we review (all below). And each factor can also have a few factors within it that make up the overall score for that factor – which we’ll typically outline on the relevant page.

Savings accounts are a bit different, we’ve weighted the savings interest rate higher (as 50% of the rating) as that’s the most important thing (earning the most money back). But, we still look at:

We make sure you and your money are safe and secure when using a company or product.

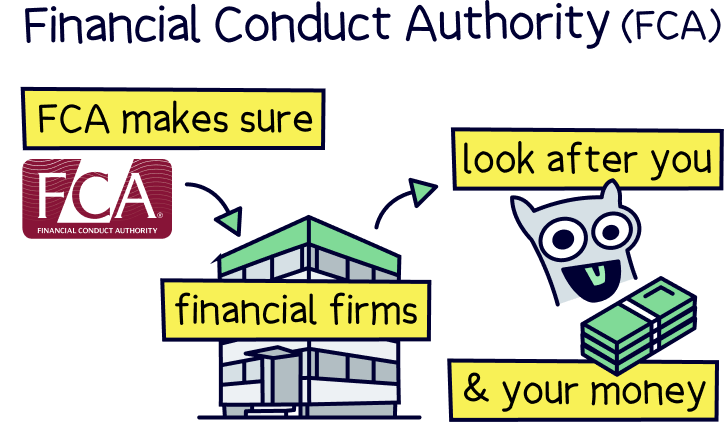

We check if they are authorised by the Financial Conduct Authority (FCA), which means they’ve been provided a licence to become a financial services company, and to look after you and your money.

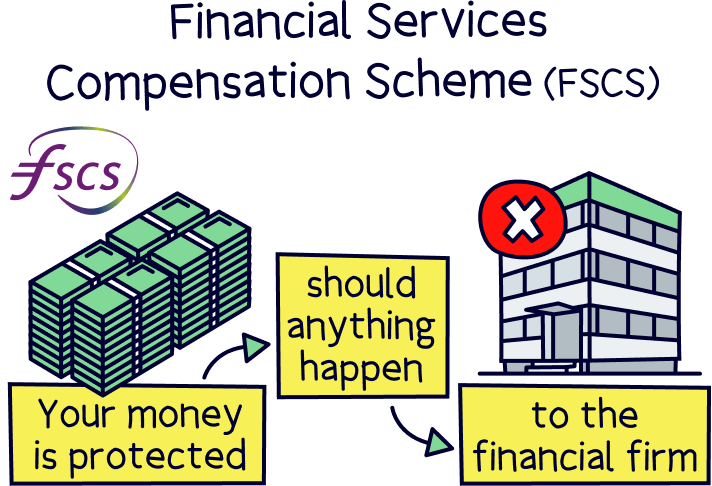

We also look at how your money is safeguarded (e.g. FSCS protection, which can provide compensation should a company go out of business and not return your money).

Companies won’t feature on Nuts About Money if they are not authorised when they need to be.

We also make use of the FCA’s ‘Treating Customers Fairly’ (TCF) framework to assess a company, as we think it’s pretty great, and focuses on getting the best outcome for customers.

It consists of 6 outcomes, which are:

If available, we assess the reviews from third parties such as Trustpilot and Google reviews, where customers can submit their own rating and reviews. We like to read and review customer’s real experiences and compare them with our own.

And we look at any awards that might have been won.

However, we know reviews and even things like awards can be manipulated and can be biassed, so we don’t rely on these, and are a very small factor in our wider assessment framework.

We also collect data directly from the company where we can – they’re often very friendly! This can be results from surveys and questionnaires, customer interview insights, interviews and questions with key staff, and things like product demonstrations.

As an example, many companies survey customers to determine a Net Promoter Score (a score out of 10 of how likely customers are to recommend a company or product to a friend), which is an industry accepted measure of customer satisfaction.

We also look at the educational resources provided to customers, that’s things like useful guides, videos, articles, newsletters and more. And we look at the help provided to customers (included within customer service).

We think companies are in a great position to educate their customers more about finances where possible (for instance, learn more about pensions, if you’re using a pension company).

We hope that’s given you an in-depth overview of our rating criteria – we want everything to be transparent here at Nuts About Money, so you can make the right decisions for yourself.

Our reviews are entirely impartial and we don’t accept payment for positive reviews. Here’s where to learn more about how we make money.

Any questions or feedback? Get in touch. We’d also love to hear your own experiences with financial companies.

We're a team of highly experienced financial professionals, with nearly 100 years combined experience helping people with money advice (working within a range of FCA authorised companies (financial services companies)).

We’ve got a whole range of professional qualifications including degrees, mortgage advice qualifications (CeMAP - Certificate in Mortgage Advice and Practice), and qualifications in financial advice, financial planning, investment planning, pensions and retirement planning, retirement income planning, pension transfers and personal tax planning (APFS - Advanced Diploma in Financial Planning).

Alongside reviews and ratings, our expert team produces our easy to understand, in-depth and informative content, and each article is reviewed to ensure accuracy, and to ensure each article provides as much guidance and help to our readers as possible.

That's it! All the best and thanks for reading.