Article contents

Over the last 6 years, from our analysis, the industry average (per year) for each category was… lower risk: 1.50%, medium risk: 2.53%, higher risk: 3.53% and highest risk: 4.42%. If you had invested with the Moneyfarm, the top performing ISA from our research, you could have made an average of 8.23% per year.

Got a Stocks and Shares ISA already, and looking to check performance? Or maybe looking to start saving with one of the top performing ISAs (historically speaking)? You’re in the right place.

We’ve looked at research and analysis of a wide range of Stocks and Shares ISAs to determine an average returns figure, which are categorised into 4 common ISA investment options (more on those below).

Note: by ‘returns’ we mean by how much money you would have made from your original investment.

Using this average, we've compared some of the most popular ISA providers (ISA companies) to see which one comes out top.

So, without further ado, here’s the top performing ISAs, and we’ll cover the average ISA return below.

Note: we’re just looking at managed Stocks and Shares ISAs, where the experts handle things. The alternative is an ISA where you make your own investments, called a self-managed Stocks and Shares ISA, and how much you make (returns) depend on which investments you make.

Invest easily and sensibly with investments managed by experts. With a great app and excellent customer service.

Invest easily and sensibly with investments managed by experts. With a great app and excellent customer service.

Invest easily and sensibly with investments managed by experts. With a great app and excellent customer service.

Invest easily and sensibly with investments managed by experts. With a great app and excellent customer service.

Right, let’s get to the good stuff, what is the average Stocks and Shares ISA return?

Typically, within a Stocks and Shares ISA, you’ll be investing in an investment fund, which is where your money is pooled together with other investor’s money, and experts buy and sell investments, with a range of different goals for each fund (e.g. long-term growth).

So, to get the overall average, we take an average of all the investment funds out there. Simple right?

To do that, we looked at data provided by an investment firm called Asset Risk Consultants (ARC). They collect and manage investment performance from a huge range of investment funds, grouped by different categories of risk (more on that just below), and together these groups are called indices (each one is an index).

Risk is all to do with the fluctuation of your investments over time – with a higher risk investment fund, there can be bigger ups and downs, but typically aiming to grow more over time. Lower risk means less ups and downs, but typically slower growth over time.

The indices we'll look at are:

These 4 categories are typically what most managed Stocks and Shares ISA offer, which you pick from – so we can match these 4 categories, which that of ISAs and look at how they performed.

All make sense? Let’s look at the industry averages over the last 6 years.

We’ll also compare some of the most popular managed Stocks and Shares ISAs, to see who’s performing well (or not) – and those are Nutmeg, Wealthify, and Moneyfarm.

Average performance over the last 6 years.

Here’s the categories we’ve used for each ISA:

Nutmeg: Level 3

Moneyfarm: Level 3

Wealthify: Tentative

Industry average: ARC Cautious Private Client Index

Average performance over the last 6 years.

Here’s the categories we’ve used for the medium risk ISAs:

Nutmeg: Level 5

Moneyfarm: Level 4*

Wealthify: Confident

Industry average: ARC Balanced Asset Private Client Index

Average performance over the last 6 years.

Here’s the categories we’ve used for the higher risk ISAs:

Nutmeg: Level 7

Moneyfarm: Level 6*

Wealthify: Ambitious

Industry average: ARC Steady Growth Private Client Index

*Moneyfarm has fewer risk options than Nutmeg, and so the numbers are different, however they’re the same higher risk option.

Average performance over the last 6 years.

Here’s the categories we’ve used for the highest risk ISAs:

Nutmeg: Level 9

Moneyfarm: Level 7*

Wealthify: Adventurous

Industry average: ARC Equity Risk Private Client Index

*Moneyfarm has fewer risk options than Nutmeg, and so the numbers are different, however they’re the same highest risk option.

To summarise, Moneyfarm performed great, and won every single category – lower risk, medium risk, higher risk and highest risk. Not bad right?!

They’ve beaten the industry average in every category, and beaten the other popular ISA providers we’ve compared, Nutmeg and Wealthify.

Well done Moneyfarm¹ – let’s hope it continues into the future too. (As with all investing, past performance doesn’t guarantee future success, but it can be a good indicator).

You can learn lots more about how we get these results with our guide to the best performing Stocks and Shares ISAs.

To measure the past performance of your investments, it can be a good idea to compare them against an average, and this is often called a ‘benchmark’ (like what we did with our research).

However, it can be a bit misleading, and you may find that the benchmark isn’t right for your investment strategy and investment goals – you should find a benchmark that matches the investment strategy of the investment fund(s) you’ve invested in.

Typically speaking, a benchmark is often an index (a measure of a group of investments), that is put together and tracked by a data company.

We’ve used ARC Indices to compare managed Stocks and Shares ISAs, but there are others, such as MSCI Indexes. And, depending on your investments, you could simply compare them against the FTSE 100 (top 100 companies in the UK), or the S&P 500 (top 500 companies in the US).

For instance, if you’re looking for the highest long-term growth possible, you might want a benchmark (index) that focuses on higher risk long-term growth. Or, if your investments have an ESG focus (green investments, e.g. no fossil fuels), you might want an index that focuses on ESG too.

As we’ve been looking at investment platforms (online investment companies like Nutmeg, Moneyfarm and Wealthify), they’re fairly new, and haven’t yet all been around for 10 years.

However, if you’re looking for a simpler idea of performance over 10 years, the FTSE 100 returned 84.40% in total between 2013 and 2022 (London Stock Exchange) – that’s if you include dividends (company profits being paid out to shareholders) being reinvested.

The S&P 500 saw a return of 221.98% over the same 10 years (S&P Global), which is especially high and fuelled by a technology boom in the United States.

As you can see, using a benchmark of 84.40% (FTSE 100), would produce a different outcome than using 221.98% (S&P 500). They’re all different investments, representing different investment strategies. You need to find one that matches yours.

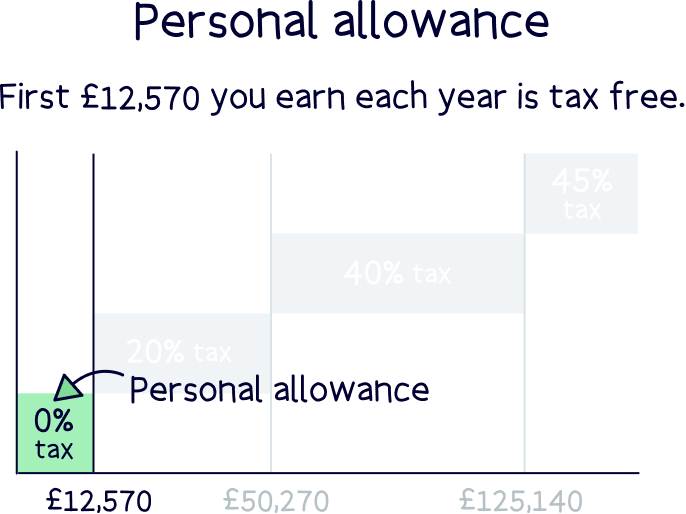

If you’re not quite sure what a Stocks and Shares ISA is, let’s run through it now quickly. It’s also often called an Investment ISA.

It’s technically a type of Individual Savings Account, which is a government scheme where you can save completely tax-free, forever! And even withdrawing your money is tax-free too.

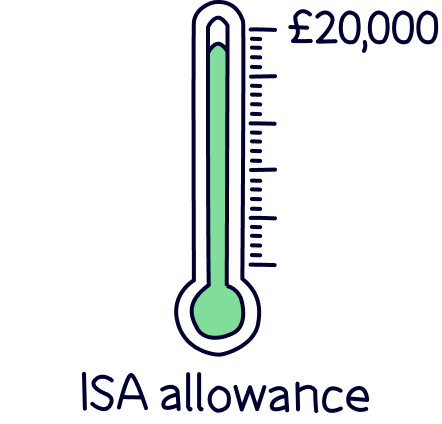

You can save up to £20,000 per tax year (your annual ISA allowance), and this is shared across all the different types of ISAs, for instance a Cash ISA (for cash savings), and a Lifetime ISA (to save for your first home, although this has limit of £4,000 per tax year).

With a Stocks and Shares ISA, you can make a whole range of investments including of course stocks and shares (the ownership of a company, split into small parts, called shares), and investment funds (groups of investments, such as shares, pooled together into a single investment, managed by experts called fund managers).

There’s also bonds, which are effectively loans to governments (government bonds) and large businesses (corporate bonds), in return for regular interest payments – often typically seen as safer than stocks and shares, and can make up a large portion of lower risk investment plans.

Shares and funds are bought and sold (traded) on stock exchanges across the world, such as the London Stock Exchange (LSE) in the UK, and the New York Stock Exchange (NYSE) in the US. Often, the word stock market is used to refer to buying stocks and shares.

Investment funds that are bought and sold on stock exchanges are called exchange-traded funds (ETFs), and super popular with investors, as they’re typically much cheaper than buying all the individual shares that make up the fund (and saves a lot of time).

You can make your own investments within a self-managed ISA, such as with Trading 212¹.

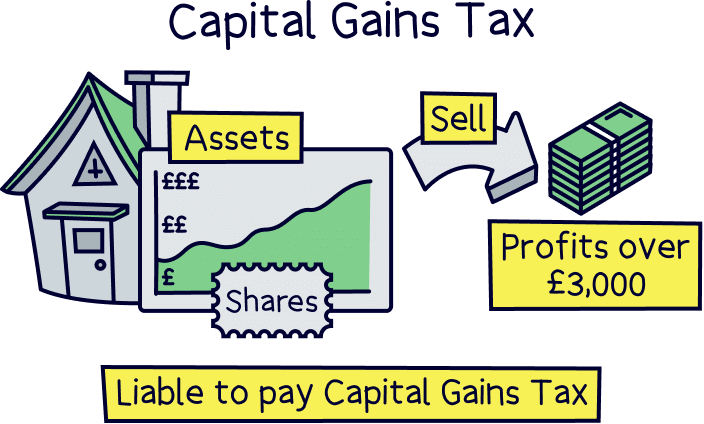

The type of tax you’ll avoid paying when you save into an ISA, or a pension, is primarily Capital Gains Tax, this is a tax you’ll pay when your money grows over time, and is either 18% or 24% depending on your income (18% if you earn less than £50,270, and 24% if you earn more than £50,270).

You’ll pay Capital Gains Tax on any profits you make over £3,000 (which is called your Capital Gains Tax allowance) – and only applies outside of an ISA, for instance within a General Investment Account (GIA), which is a regular investment account without any tax-free benefits.

Within an ISA (and pension), you’ll also avoid paying Income Tax, and Dividend Tax, which are taxes you could pay if investments pay an income, and if a company pays out some of its profits to its owners (called shareholders), which is called dividends.

If you’re a bit concerned about whether saving cash or investing is better, well, as they say, that depends!

It’s all down to whether you’re looking for growth in your money over the long-term, and happy to not touch it (investing), or you want slow and steady growth with the safety of no ups and downs (saving cash).

Nuts About Money tip: if you're interested in a Cash ISA, check out our Best Cash ISAs table.

Typically, investing would grow your money much more over time (if you make investments suited to long-term growth, such as using a higher risk option with a managed Stocks and Shares ISA).

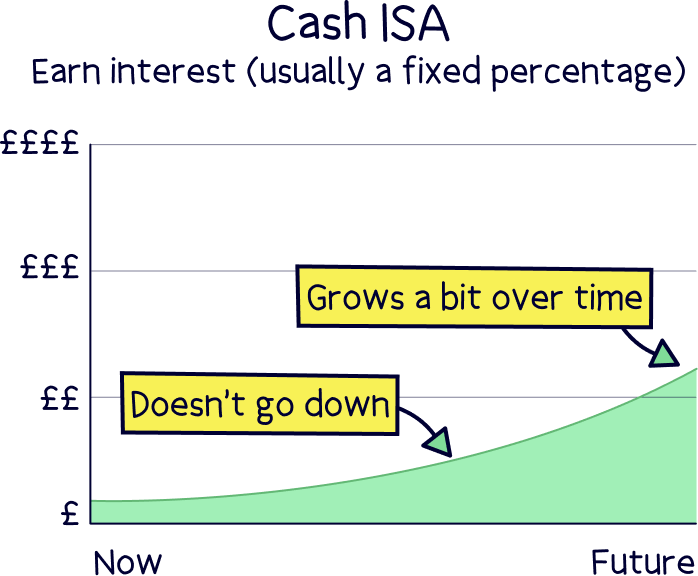

When you save cash, your money will typically grow less than, or in-line with inflation (which is the price of things getting more expensive over time), and that’s if you get a good interest rate.

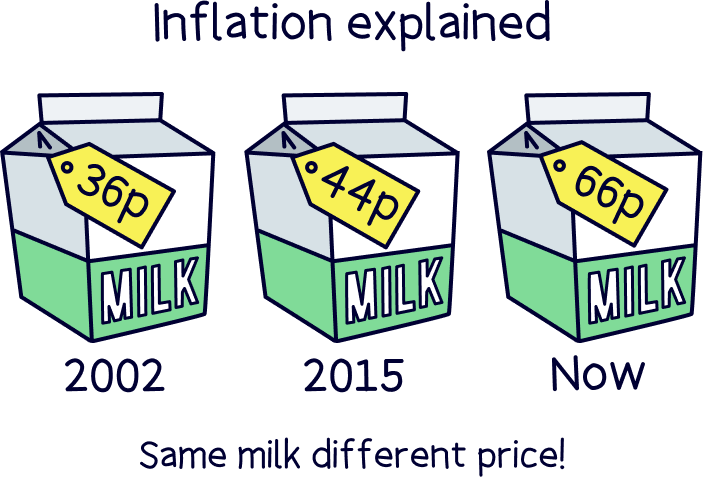

As an example of inflation, in 2002, a pink of milk cost 36p, and now it costs 66p – almost double!

Interest rates from banks and other lenders who provide Cash ISAs (and other savings accounts such as easy access savings accounts), are typically linked to the Bank of England base rate, which is the interest rate set by the Bank of England to combat inflation in the UK – and is the rate banks get when they deposit money with the Bank of England (so when it goes up, your savings rate should go up too (but banks often don’t pass this on)).

If the base rate is high, and so you get a higher interest rate on your cash savings, then typically inflation is much higher! You’re actually losing wealth each year (in relation to what you can buy with your cash), as things like milk and fuel are becoming more expensive.

Investing sensibly (over the long-term) typically sees your money grow more than inflation. So, as a general rule, you could at least keep up with inflation.

You can learn more about this with our guide: Cash ISA vs Stocks and Shares ISA.

By the way, you don’t need to choose either or, you can have both at the same time! The £20,000 ISA allowance is split between them (but that’s a pretty hefty allowance anyway).

Nuts About Money tip: although a Cash ISA is tax-free, you might be able to get a better interest rate with a standard savings account (like Lightyear¹). The interest you make could be tax-free anyway, thanks to your Personal Savings Allowance from the Government…

This is where you can earn up to £1,000 in interest per tax year, without having to pay tax on it. Pretty great right?

You’ll get a £1,000 allowance if you’re a basic rate taxpayer (earning less than £50,270 per year), a £500 allowance if you’re a higher rate taxpayer (earning more than £50,270 per year), and no allowance if you’re an additional rate taxpayer (earning over £125,140 per year).

That means, if you earn less than £50,270, you’ll need more than £20,000 in savings before you have to pay any tax on your interest (at a 5% interest rate). So, you could check out high interest savings accounts before opening a Cash ISA.

If you’re looking to save for your future, yes! It’s typically always a good idea to save and invest sensibly over time – as we mentioned above, it’s normally better returns than saving cash, and your money can grow really quite large over time.

If you opt for a managed Stocks and Shares ISA (where the experts handle thing), all you need to do is select which type of investment strategy you’d like (usually picking from lower risk to higher risk, normally dictated by how long you’re planning to invest for), and then add your money (ideally monthly), and that’s it. All taken care of.

If you’re looking to make your own investments, check out the best investment platforms.

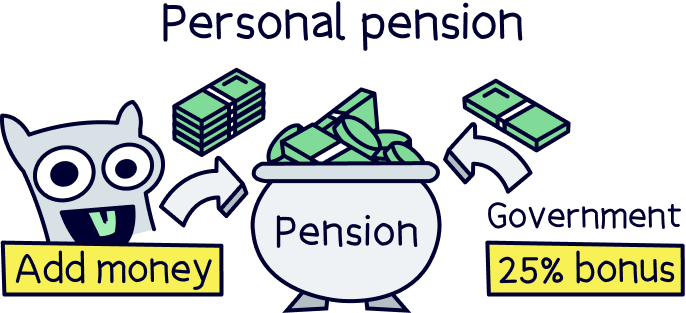

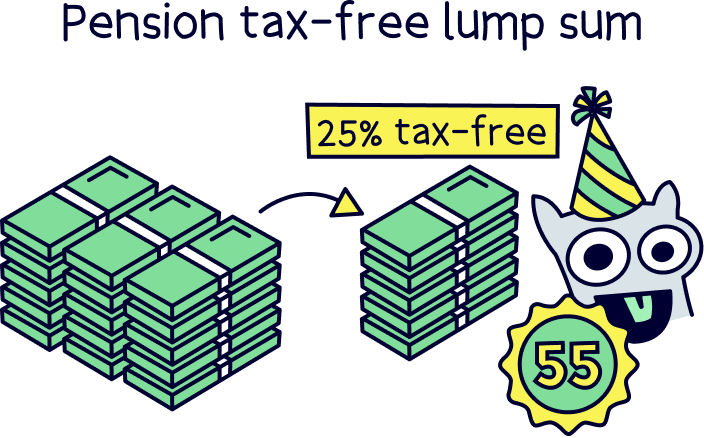

However, if you’re planning to invest for the very long term (for instance when you’re over 55 years old (perhaps planning for retirement), then it’s also worth considering a personal pension, which has amazing tax benefits too…

A personal pension is similar to an ISA, where your money grows tax-free, except, they’ve got one huge advantage – you get free money!

We’re not talking about a pension from your work (called a workplace pension), we’re talking about a pension you set up yourself, called a personal pension.

Nuts About Money tip: save into both and boost your retirement income later down the line.

Saving into a pension is intended to be tax-free, so when you save into a personal pension, with money that you’ve already paid tax on (e.g. after you’ve been paid), you’ll automatically get a massive 25% bonus from the Government added to your pension pot. How great is that?

And if you’re a higher rate (paying 40% tax and earning over £50,270 per year), or additional rate (45% tax, earning over £125,140 per year), you can claim back some of the tax you’ve paid at these rates too (on a Self Assessment tax return).

There are some limitations – you can only withdraw your money after 55 years old (57 from 2028), and you can only pay in as much as your total income per tax year or £60,000, whichever is lower. (A tax year runs from April 6th to April 5th the following year.)

When it does come to withdrawing your money, 25% of it will be completely tax-free. With the remaining 75%, you might need to pay Income Tax on (like your salary now) – it depends on how much your income is at the time.

If a personal pension sounds interesting (and it should), learn more and check out some great options with our best personal pensions (UK). As a spoiler, PensionBee¹ tops the list – it’s easy to use, low cost and has a great record of investing for the long-term. Beach¹ is also great, it's an easy to use pension with a great app. Add money or combine old pensions (and find lost pensions). Plus, the customer service is excellent.

Note: making your own investments within a personal can be done with a self-invested personal pension (SIPP). Here’s the best SIPP providers.

If you’re not sure if a pension or ISA is right for you, it’s a good idea to speak to a financial advisor (who provides independent financial advice), they can help you decide what's best for you and your financial goals in the future, based on your personal circumstances. You can find great financial advisors, local to you, with Unbiased¹.

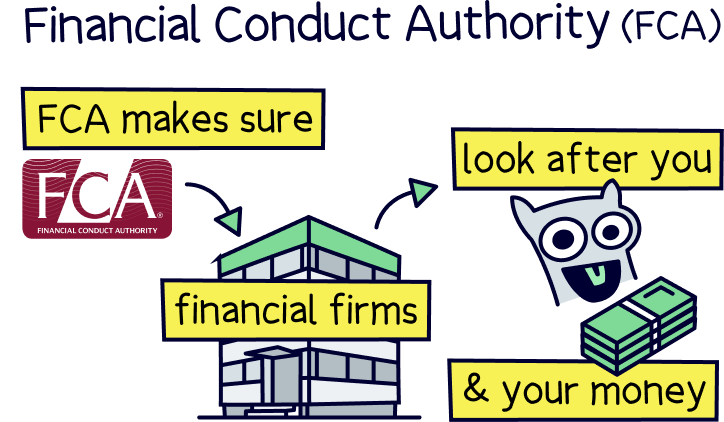

It’s perfectly safe to use a Stocks and Shares ISA. Every ISA provider needs to be approved by the Financial Conduct Authority (FCA) – they’re the people who make sure financial companies are looking after you and your money. Financial companies need to follow strict rules to operate.

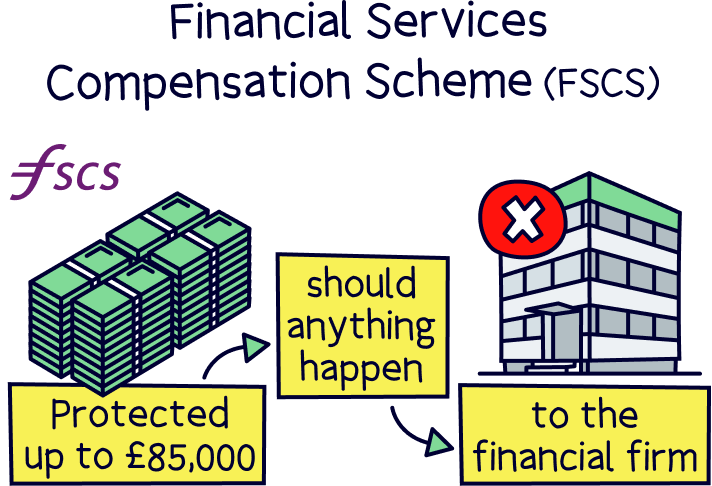

That means you’ll be covered by something called the Financial Services Compensation Scheme (FSCS) too, which can pay compensation up to £85,000 in the unlikely event that your ISA provider goes out of business – however, your money will actually be held in the investments themselves, which are typically managed by large investment companies or banks, all in your name, and can only be returned to you, giving you even more protection.

However, that doesn’t mean that investments can’t go down in value, it all depends on your investments and the investment strategy you’re using.

There’s typically ups and downs with investing, but over time, these smooth out, and if investing sensibly, you’ll ride these out and your money should grow over time.

There we have it for the average Stocks and Shares ISA returns – it’s been a bumpy few years (to say the least!), but on average, expert managed Stocks and Shares ISAs have increased in value by a reasonable amount (and much more than cash savings). The amount they've grown is usually dependent on the category (risk level).

You can’t really beat Stocks and Shares ISAs when it comes to saving for your future, well, except within a personal pension to save for retirement (where you get a 25% bonus on money you add). You’ll likely make more over time than just saving cash, and the longer the save, the bigger the difference typically is.

Finally, you’ve got two options when it comes to Stocks and Shares ISAs, either make your own investments, or let the experts handle things – we typically recommend using the experts for most people, and from our research, Moneyfarm¹ tops the list, and is low cost and has experts on hand to help if you’d like it.

If you want to keep all your savings in one place, for instance, an ISA for short-term goals and a pension for retirement, check out Beach¹.

That’s it. All the best to growing your savings in future!

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Invest easily and sensibly with investments managed by experts. With a great app and excellent customer service.