Article contents

The best budgeting apps in the UK are Emma and Moneybox. They’ll connect to your bank account and save automatically for you. Plus, you can save your money within a savings account and earn interest or invest it to grow over time too.

Looking to save more money? You’re in the right place. Here’s the best budgeting apps:

Emma is a great app to help manage your everyday finances, save more and improve your credit score.

Emma is a great app to help manage your everyday finances, save more and improve your credit score.

You can connect your bank account(s) and Emma will work out where your money is going and where you could save money (such as showing all of your subscriptions).

It’s pretty great for helping you to budget and save for things such as holidays.

You’ll be able to earn interest on the money you save (with a high interest rate), or you can invest it if you like.

Cons

Moneybox is super popular, with over 1,500,000 customers. It offers the full range of savings and investing accounts, from saving cash (at a great savings rate), to saving for retirement with a pension.

The mobile app is great and easy to use, with a range of investment options to choose from, which includes investment funds and individual shares (e.g. Apple and Amazon).

It’s low cost overall (free to save cash), and the customer service is excellent.

Emma is a great app to help manage your everyday finances, save more and improve your credit score.

Emma is a great app to help manage your everyday finances, save more and improve your credit score.

Emma is a great app to help manage your everyday finances, save more and improve your credit score.

Snoop isn't a savings or investment app. It tracks your spending and helps to reduce your bills. You can use this in addition to the others.

You connect all your bank accounts and it will work out how to reduce your bills, along with exclusive deals on things like broadband and insurance.

It's free too. Worth checking out.

To determine the best budgeting apps, we’ve used 6 key criteria, which are:

There’s a fair few apps out there, but we’re just showing the best.

These are one we recommend to our own friends and family, and use ourselves here at Nuts About Money. So you can have confidence that whichever one you choose, you’ll have great results building up your savings.

Saving is hard, a budgeting app can help make it simple! Simply let the app work out how much you could be saving each month (and sometimes even every day) with their smart technology.

You just need to link your bank account and then the app will scan all your bills and spending and figure out how much you can realistically save. It will then automatically transfer some money to your savings app (little and often), and before you know it, you’ve got loads of cash saved up, without lifting a finger.

The best and most popular budgeting apps will also invest your money too (if you want to), which means it could grow even more in the future! Pretty great right?

It’s a great idea to use a budgeting app to help you save more – as it takes the hassle out of saving and works out the right budget for you. And let’s be honest, no one likes playing around with spreadsheets or doing maths in their spare time!

All you have to do is simply connect your bank account through their app and you’re away (you can even connect all your accounts). They’ll analyse your spending and work out how much you can save. Your savings will start building up and hopefully you won’t even notice the money coming out of your account.

It’s always tempting to spend money that’s in your account isn’t it? But when it's inside your own little savings account on a budgeting app, you’re much less likely to spend it on a round of drinks or on that next unnecessary purchase on Amazon.

The top 2 budgeting apps we’ve listed above are the best free ones – Emma¹ and Moneybox¹

Well, they’ve got free accounts to get you started and budgeting properly. You can then upgrade to a paid plan if you like for more features (such as better savings features), or to access a wider range of investment accounts and things to invest in (we’ll run through the investing side of things below).

The paid plans are relatively cheap too – they help you save money rather than spend it. Perfect!

Give an app a try. You never know, you might save much more than you could ever imagine!

If you’re completely new to saving and budgeting, the best option is Emma¹.

The app is super easy to use – their technology will work how much you can save and automatically save it for you. And that’s the hardest bit done.

And if you’re ready to invest your savings, there’s easy to understand investment options, where their experts will handle everything for you. All you need to do is decide how much risk you’d like to take in return for higher potential growth in your savings (it's not as scary as it sounds).

A budget is technically how much you are spending and what you are spending it on. And here we mean it’s a personal budget – so a budget for your own finances, your spending on bills and life in general.

You’ll normally have a set income each month, for instance your salary, and then you can figure out how much of that income you can put towards your savings and your outgoings (e.g. your bills).

Budgeting apps do this for you in an automated way, by reviewing your income and spending, and figuring out how much you can save.

If you’re over budget, that means you’re spending more than your income allows. Your income should be the maximum you can spend (your maximum budget).

And if you’re under budget, great! That means there’s room to save cash – you have more income than your outgoings.

If you’re not quite sure on budgeting apps yet. Here’s how to make a budget yourself:

First, work out your total income, that’s your salary and any other money you might get from anywhere else. And work out how much you have after tax. If you’re unsure how much you actually pay in Income Tax and National Insurance contributions, and how much you should have after tax, check out our take-home pay calculator.

If you’re not sure about Income Tax and National Insurance contributions, we run through this below.

Then, we’re going to use the 50/30/20 rule. It’s a great way to budget effectively.

With this, you want to aim for 50% of your spending on essentials, such as rent or a mortgage, and all of your household bills and living expenses (your needs).

Then, 30% for your ‘wants’. This is things like buying new clothes, going out for drinks, or even a date and your subscriptions like Netflix etc. Anything you like really! But remember, it’s not a target to spend 30%. 30% is your budget that you can’t go over (ideally), and the lower the better!

And the remaining 20% is for savings – or if you’ve got any debts, use this money to pay off debts. If you’ve got things like credit card debt, it’s better to pay this off first, rather than build up a savings pot, as the interest rate is often very high – and you won't get the same interest rate from your savings, so you will technically keep losing money.

By the way, interest is either what you pay to borrow money, or what’s paid to you for lending your money (which is what happens when you put it in a savings account – you are effectively lending it to a bank or financial institution).

So, 50/30/20 – pretty simple right? 50% for needs, 30% for wants and 20% for savings.

If you can’t quite save 20%, don’t worry. As Tesco would say ‘Every little helps’. Just save as much as you can to begin with. And if you can do even better than this, great! Such as 30% for needs, 20% for wants and 50% for savings. You’d soon build up a huge savings pot!

And this is where budgeting apps become super useful. They can help to save and often a lot more, without you even realising, or having to do anything!

Income Tax is a tax on quite simply, your income! Everyone has to pay it, and it goes towards public finances which the government then decides where it’s spent.

Income Tax is one of your biggest bills even though you might not even realise it. But don’t include it in your budget. Budget with your after tax pay (the income tax has already been paid).

Nuts About Money tip: use this cool tool to work out your after tax pay, or use our own take-home pay calculator.

Income Tax comes straight out of your pay packet if you’re employed, so you might not even know you pay this! If you’re self-employed, you’re probably a bit more familiar – as you’ll have to handle it yourself every year (you’ll handle this through your Self Assessment tax return).

If you’re not quite familiar, here’s how it works.

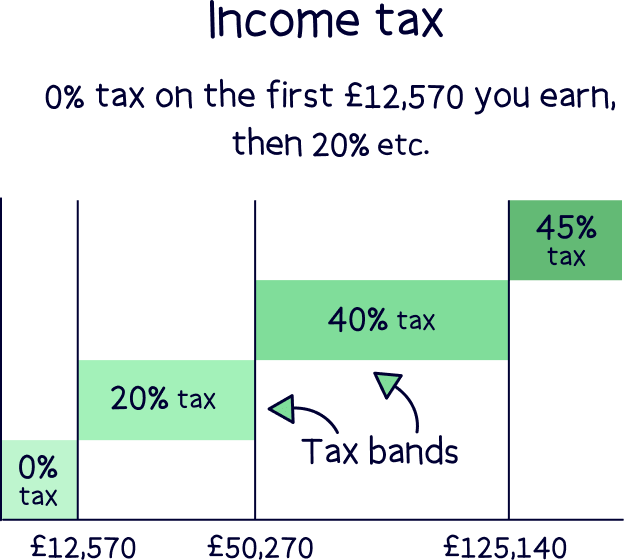

You first get a Personal Allowance, and this is currently £12,570. That’s how much you can earn every tax year (April 6th to April 5th the following year), without having to pay any tax at all. Whoop!

After that, any money you earn above that, you’ll pay 20% Income Tax on. This is called the ‘Basic rate’. And this goes all the way up to £50,270.

Then, if you're lucky enough to earn above £50,270, you’ll pay 40% tax on everything up to £125,140. This is called the ‘Higher rate’. And above £125,140, you’ll pay a staggering 45%. This is called the ‘Additional rate’.

Fairly straightforward right? Here’s a table to make it a bit easier:

Oh, and if you’re lucky enough to earn over £100,000 per year, your Personal Allowance, the £12,570 you get before you have to pay tax, starts reducing. Meaning you’ll pay even more tax!

For every £2 you earn over £100,000, your Personal Allowance reduces by £1. Which means if you earn £125,140 (or more), you won’t have any Personal Allowance at all, and you’ll pay tax on the whole of your income (sorry for the bad news).

National Insurance is another ‘tax’ on your income – although instead of going straight into the government pocket for anything they like, it goes towards helping people in the UK. So that’s things like the NHS and the State Pension.

You’ll only pay this when you earn over £12,570 per year, just like Income Tax. And here’s what you’ll pay:

Some of us have some fairly bad spending habits! But that’s okay, as least you know you have a problem (or do once you’ve set up a budget).

It’s a hard problem to solve on your own without a budgeting tool (either an app or simply managing your money yourself) – but is certainly doable.

Common tactics are going completely ‘cold turkey’ and not buying anything that you don’t need for a certain period of time (for instance a month).

Or, you could start introducing ‘no spend’ days, where certain days per week you absolutely cannot spend any money at all (except for essentials like travelling to work).

You could also take out cash each month after you’ve set a budget limit, and you can only spend the cash you have, think of it as ‘spending money’ like on a holiday. And never touch your bank cards or bank accounts for the whole month.

There’s lots of options out there, but ultimately it’s about changing your behaviour over time, think of it like trying to change a habit. It gets easier over time! And the most popular budget apps (above) are helping lots of people across the UK – you’re not alone!

Nuts About Money tip: review and cancel wasteful subscriptions! They’re a real budget killer.

Instead of just rounding up your spare change, or saving and investing your money automatically. You can also use a budget app to help with everyday spending and improve your personal finances and financial situation in general.

Apps like Snoop¹, a free budgeting app, have a spending analysis tool and some handy budgeting features.

You can connect all your financial accounts, for instance all of your credit card accounts and multiple current accounts (if you have them). It will then show you exactly where all your money is going – you can view all your accounts in one place.

You’ll be able to see upcoming bills from multiple accounts, see spending categories, view daily spending and spending activity, view wasteful subscriptions, create budgets with advanced budgeting features, and check if you have enough money to spend before the next payday, the list goes on! Ultimately it will improve your spending habits so you can make spending improvements yourself.

The spending insights are pretty great, and the ability to add multiple accounts is really cool. Most budget apps will support all the major banks (current account) and financial providers.

And on top of that, it can also check if you are overspending on your household bills, such as broadband and energy bills. Which it does by checking all the suppliers out there to see if there’s a cheaper one for you and your personal circumstances.

You could also check out Money Dashboard, another money management app (but we think Snoop¹ is the best free budgeting app). Mobile banking apps like Revolut¹ are great too (and have very advanced features to track spending, and things like savings pots).

Saving for something special? Perhaps a holiday, new car, rental deposit, or even a wedding?

Budgeting apps in the UK are great for these. You can create a saving goal within the app itself, sometimes called pots, or pockets – and these will separate your money so that your savings go towards that, rather than just having a general account with all your savings in.

It gives you a good focus, and a reason to save will keep you more motivated to keep up the saving. You’ll soon have that goal saved in no time!

So, once you’re all set up on the budgeting app and linked to your current account. With most budgeting apps you’ve now got some decisions to make on how your money is actually saved and how it grows in future.

The first option is a simple savings account, where you earn interest on your money. Simple! Your money will go slowly over time.

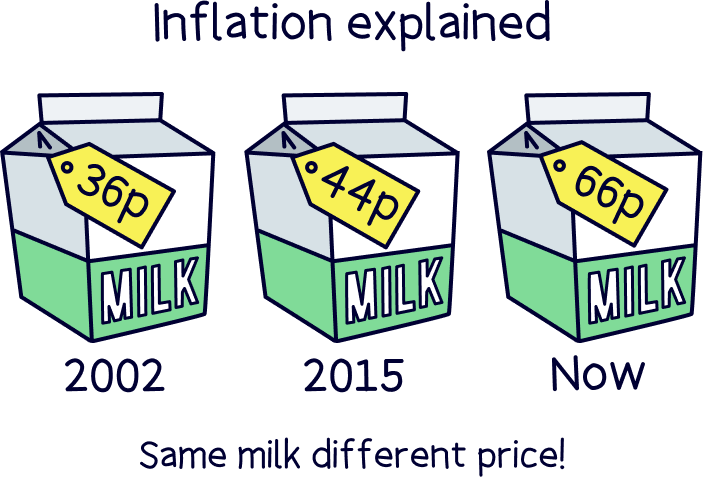

However your money will often grow lower than the rate of inflation. This is where the value of your cash reduces each year. Let’s use milk as an example. In the year 2002 a pint of milk cost 36p, however now it costs 66p! That’s nearly double the price. It's the same milk, it's just your money is worth less due to inflation.

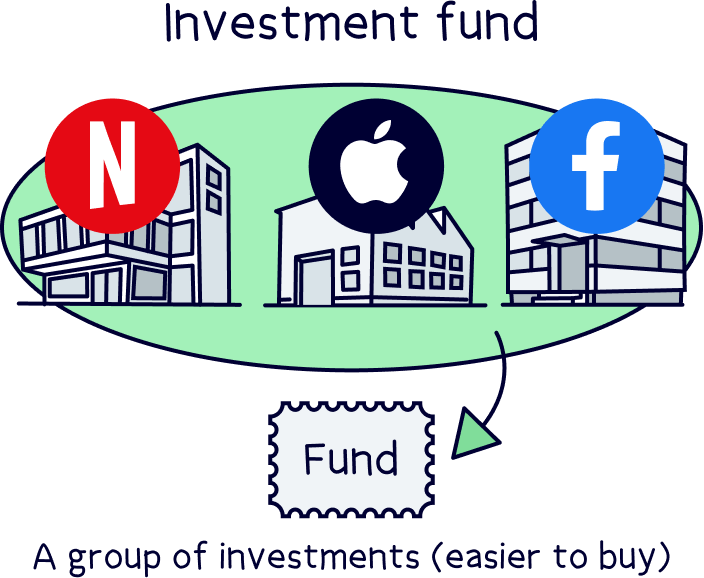

To try and combat the effects of inflation, lots of people invest their money instead of keeping it in a standard savings account. They trust their money to the experts, these experts use your money to buy investment funds, which are groups of different investments all combined together to grow your money over time in a sensible way.

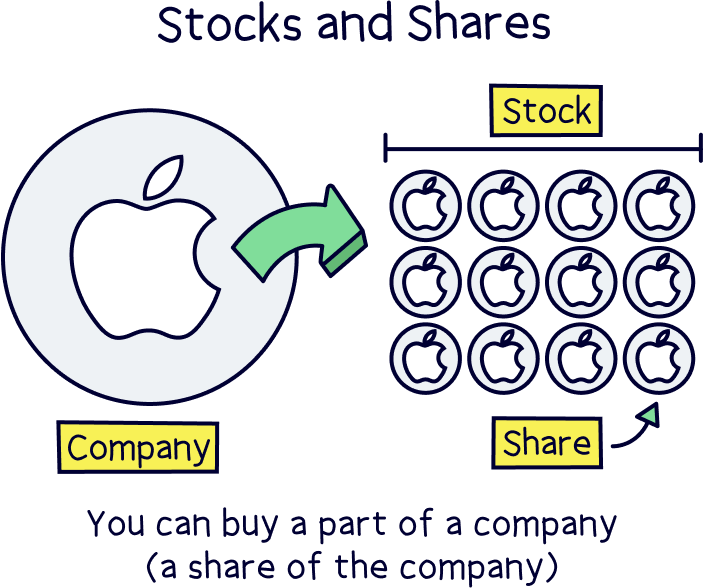

The types of investments are often stocks and shares – which is where you own a tiny part of a company (a share of the company). But can also include bonds, which are loans to governments and large corporations who borrow cash and pay interest in return. Plus many other types of investments, sometimes even property.

The best type of investing account is called a Stocks & Shares ISA – which all of the budget apps offer. These accounts are amazing. When you save within this type of account, it’s completely tax-free! So you’ll never pay any tax on your money when it grows.

Alternatively, you can invest in a standard account (often called a General Investment Account), which has no tax-free benefits, so you might have to pay taxes, such as Capital Gains Tax.

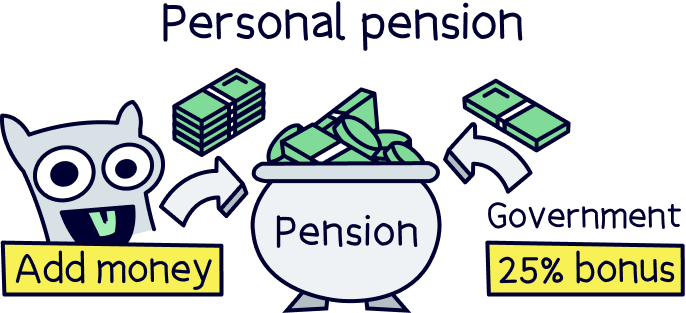

Or, you could even save within a personal pension (which is also tax-free, and you get a whopping 25% bonus from the government every time you pay in, it’s free money!). We recommend using a dedicated pension provider to save for your retirement however, rather than a budgeting app. You can find one with our best personal pensions, and 5 star rated PensionBee¹ (here’s our PensionBee review).

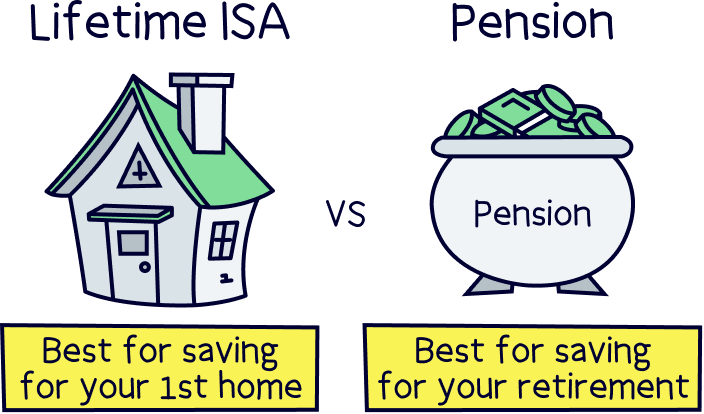

And then if you’re saving for your first home, you could also save within a Lifetime ISA. This is tax-free too, and you’ll also get a 25% bonus from the government on everything you save, but it can only be used to buy your first home. There are also great dedicated providers too, and here’s the best Lifetime ISAs.

Overall, it depends on your saving goals, but often the best account with a budgeting app is a Stocks & Shares ISA as you can withdraw the money whenever you need it.

There’s been a lot of progress in technology over the last few years in banking and personal finance, and something called open banking has been developed in the UK and it’s supported by the government.

Open banking is where all banks must allow technology providers (like budgeting apps) to connect and access your current accounts (if you give permission) to read the transactions and data and sometimes make payments.

It’s all perfectly safe and secure. It means new technologies can be developed that benefit you, such as budgeting apps, and other things like free payments (rather than using credit cards or debit cards with fees). Over the next few years you will hear the words 'open banking' used a lot more by banks and other financial services.

If you want to geek out you can learn more on the open banking website.

Yep! Perfectly safe. You’ll need to set up and approve everything when you first start, and have complete control to stop using an app at any time and it's easy to disconnect them from your bank accounts and credit cards.

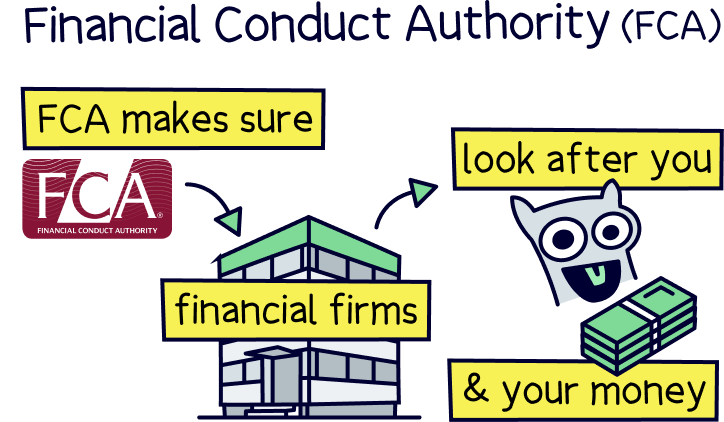

Budgeting apps are also approved and regulated by the Financial Conduct Authority (FCA). This means they’ve been reviewed and approved to look after your hard earned money and savings.

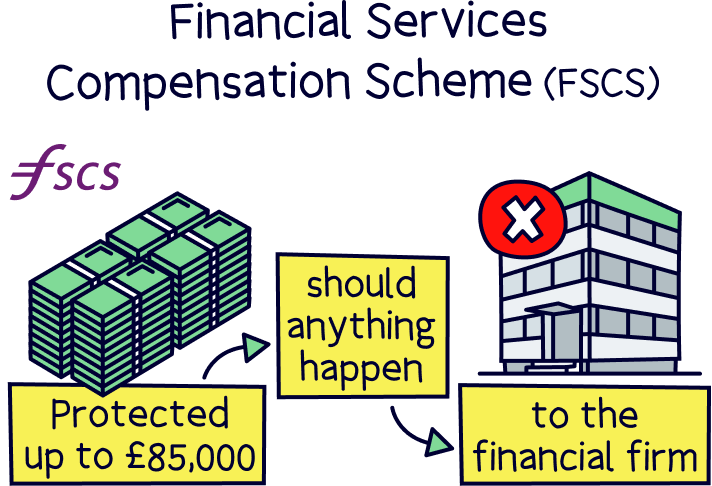

Also, when you save and invest with a money management app (budgeting app), you’ll be protected by the Financial Services Compensation Scheme (FSCS). This means you’ll get up to £85,000 back if anything goes wrong with the app company itself (such as going out of business).

However, you’ve also got more protection as your money will often be in the investments themselves (if you are investing), and these are all in your name, and can only be returned to you, not the budgeting app.

Are budgeting apps even better than you thought?

Budgeting and money management apps are great at helping you save lots more money than you probably could yourself – they’ll work out how much you can save from reviewing your spending and save this money all automatically. Pretty cool right?

And as an added bonus, you can invest your savings to grow them even more over time too. All handled by experts. And you can save tax free in a Stocks & Shares ISA.

To remind yourself of our top ticks scroll up or click best budgeting apps in the UK.

That's it! It's all over to you now! Good luck with saving! Your net worth might be looking a lot bigger soon.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Emma is a great app to help manage your everyday finances, save more and improve your credit score.