Article contents

Investing for your kid’s future is one of the best financial decisions you can make for them. With that in mind, here’s the best Stocks and Shares Junior ISAs. The best managed by experts is Moneyfarm and the best self-managed Junior ISA is AJ Bell.

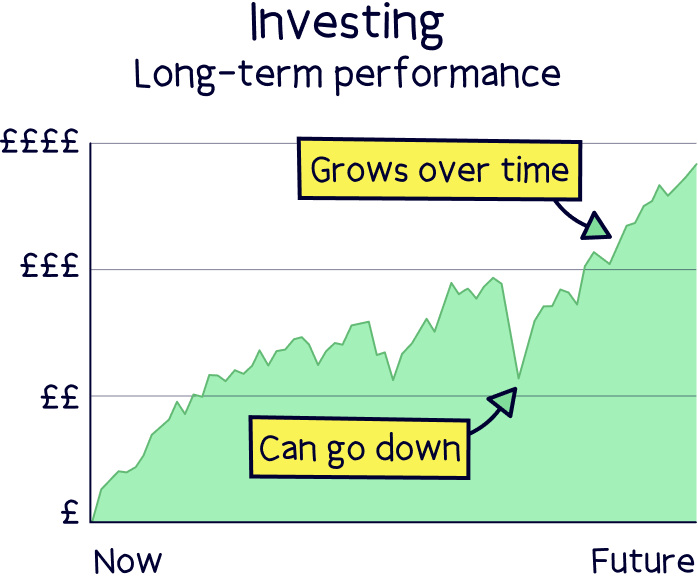

Keen to save and invest for your kids' future? Great decision. Early savings and investments can really pay off later down the line as they grow and grow over time.

When it comes to investing, you’ve got 2 options – either let the experts handle things (highly recommended), or make your own investment decisions (only recommended for experienced investors). We’ll cover the best Junior ISAs for both.

Here’s the best Stocks and Shares Junior ISAs:

Moneyfarm tops the list – they’ve got a great investment record, low fees and experts on hand to help.

Get up to £1,000 cashback

Moneyfarm is a great option for saving and investing (both ISAs and pensions). It's easy to use and their experts can help you with any questions or guidance you need.

They have one of the top performing investment records, and great socially responsible investing options too. Plus, you can save cash and get a high interest rate.

The fees are low, and reduce as you save more. Plus, the customer service is outstanding.

Beanstalk is a great Junior ISA – it's easy to use, and all works on an app on your phone.

There's simple and easy to understand options, with a choice of two funds and clever tools – perfect to build up your child's savings over time.

It's low cost too, with fees of just 0.50% per year.

Friends and family can contribute too – perfect for birthday and Christmas presents.

Get £50-500 cashback

Wealthify makes investing simple. You can open a Stocks & Shares ISA, a personal pension, a Junior ISA, or a standard account. Next, pick from a few simple investment options and the experts take care of the rest.

It's perfect for beginners and you can get started from just £1 (£50 for a pension).

The fees are reasonable, however the socially responsible option is on the higher side.

The customer service is great and you can actually speak to someone on the phone, email or live-chat if you like.

Moneyfarm tops the list – they’ve got a great investment record, low fees and experts on hand to help.

Moneyfarm tops the list – they’ve got a great investment record, low fees and experts on hand to help.

AJ Bell is well established, with a good reputation.

It's one of the cheapest traditional stock brokers out there (charging a low annual fee).

There's a huge range of investment options – pretty much every investment out there (including both funds and shares).

The customer service is great too.

Overall, it's one of the best options.

If you want a more traditional approach, with a long established history then Hargreaves Lansdown could be for you. It’s a great broker with a huge range of investment options, including expert-managed choices. However, it’s more expensive than other options.

Get £100 free trades

Interactive Investor is a popular investment platform with a flat fee, making it a cheap option if you have a larger portfolio of investments. There’s a huge range to choose from, their website and apps are great and their customer service is excellent.

Note: there's an additional fee of £30 per month for company accounts.

There’s quite a range of Stocks & Shares Junior ISAs out there, and we’ve reviewed and compared almost all of them to find the best ones for you (and more importantly, for your kids!). Here’s the criteria we used:

The Junior ISAs we recommend are all with investment platforms (places to save and invest) that we use ourselves here at Nuts About Money, and recommend to our friends and family (and readers).

So, you can feel confident you’re using one of the best out there, whichever option you choose. And for most people we recommend simply letting the experts handle things.

Nuts About Money tip: we’ve also compared the best Stocks and Shares ISAs – if you wanted to double check your own money is with the best ISA provider.

If you’re new to saving and investing in general, we recommend using an expert-managed Stocks and Shares Junior ISA – the experts will simply handle everything, all you need to do is add your money and away you go.

They’ll grow your money over time in a safe and sensible way, all suited for long-term growth. So, over the next 18 years or so, your kid’s savings could be worth a small fortune.

With that in mind, check out Moneyfarm¹, they’re a great expert-managed option overall, with low fees and a great track record of growing money over time. Plus, there’s experts on hand if you need them. However, you will need to start with a £500 minimum investment.

We also recommend Beanstalk¹ – it's easy to use, low cost, has simple investment options, and some clever tools to help you save. Plus, there's no minimum investment to get started.

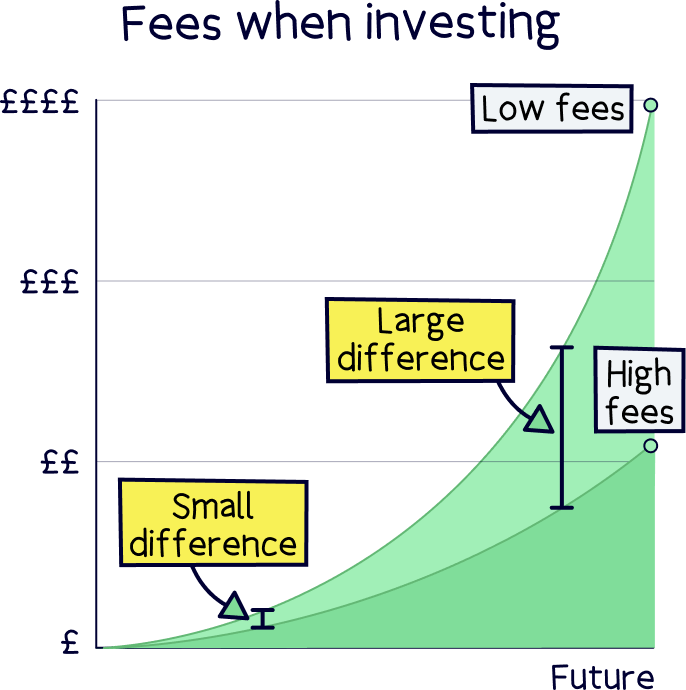

Although we don’t recommend choosing a Junior ISA, or any investment account (e.g. a regular Stocks and Shares ISA, or personal pension), based solely on fees – fees can have a big impact on how much your money grows over time.

Nuts About Money tip: we recommend choosing an investment platform based on a mix of ease of use, expert advice, and investment performance – all tailored to your own preferences.)

So, with that in mind, the cheapest Junior ISA is Beanstalk¹, it's just 0.50% (of your savings) per year. That's very low cost.

One of the best, and second cheapest is Moneyfarm¹ and their ‘fixed-allocation’ investment option, which has total fees of just 0.68% (of your total portfolio per year).

Note: fixed allocation means there’s less involvement from the experts. More involvement is called actively managed (and so slightly higher fees).

The lowest cost self-managed Junior ISA is AJ Bell¹ – they’re a traditional stock broker (a place to buy and sell investments), and will charge an annual account management fee of 0.25% on investment funds (more on that below), and a share dealing fee of between £1.50 and £9.95 depending on which investments you’d like to buy.

Although you can find online stock brokers and investment platforms cheaper than this, they don’t offer Junior ISAs.

If you’re not 100% sure what a Junior ISA is, let’s run through it.

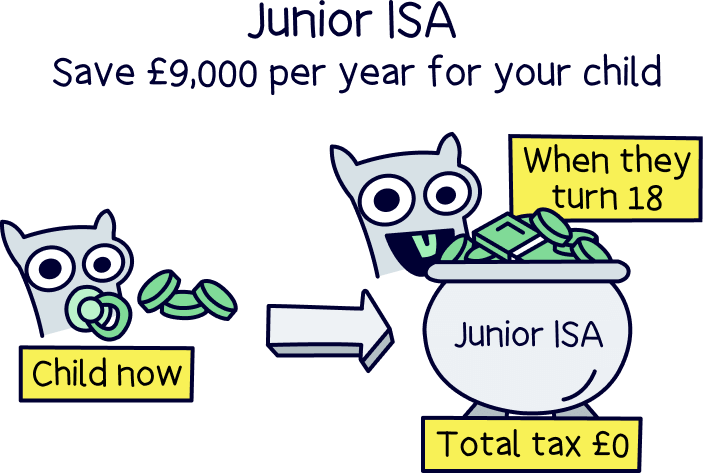

A Junior ISA, or JISA, is an awesome savings account for your children’s future. You’re able to save completely tax-free, and all in their name. You can open it when they’re any age, and they’ll get the money when they turn 18.

If you’ve got your own Stocks and Shares ISA, you’ll be familiar as they’re very similar, just in your child’s name instead of yours.

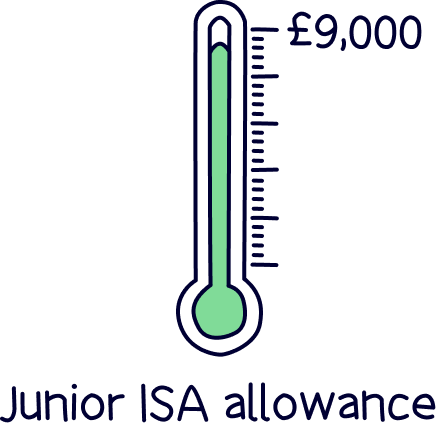

There are limits however, you can only pay into one Junior ISA and save up to £9,000 per tax year, per child, called a Junior ISA allowance, which is completely separate from your own annual ISA allowance (£20,000).

You may have heard the phrase child trust fund before, and child trust funds were a previous government scheme, almost exactly the same, and now replaced with a Junior ISA.

Note: a tax year runs from April 6th to April 5th the following year. And an ISA stands for ‘Individual Savings Account’.

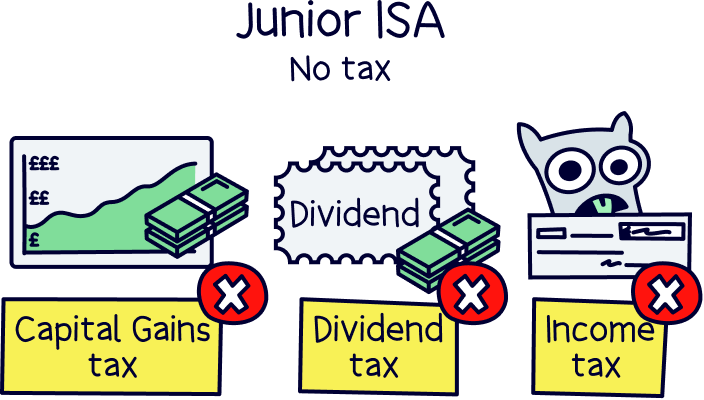

By saving and investing tax-free, you won’t have to worry about paying Capital Gain Tax, Income Tax, or Dividend Tax – which means your money can grow a lot more over the years (and there’s less admin too!).

And if you weren't aware, there’s actually 2 types of Junior ISAs, a Stocks and Shares Junior ISA, and a Cash Junior ISA. (We’ve got a guide to Junior ISAs if you want to learn more.)

This is where you can choose to invest your money in things like stocks and shares, investment funds, bonds and property (we’ll cover all of these below), with the intention your money will grow over time (and with the experts help, it typically grows a lot!).

Note: these are also often phrased as a Junior Stocks and Shares ISA, a Junior investment ISA, or children's Stocks and Shares ISA.

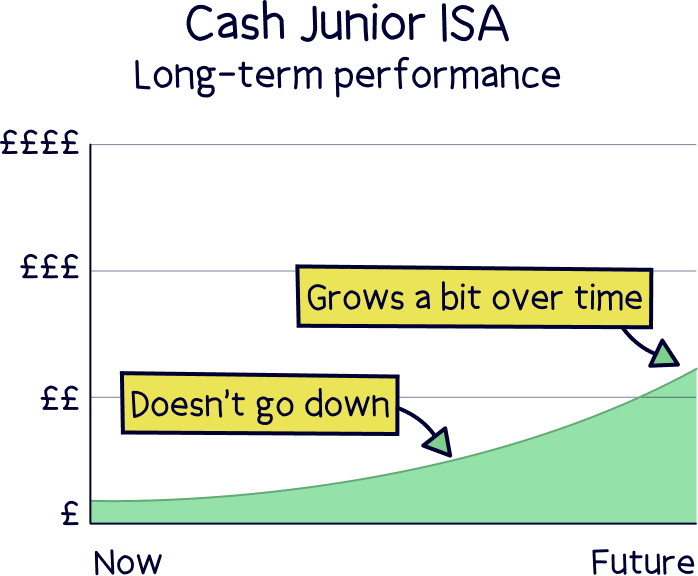

A Cash Junior ISA is where you simply save cash in exchange for interest. And the interest you receive is tax-free. There's no ups and downs over the years but your money (sorry, your kids money) probably won't grow as much over time.

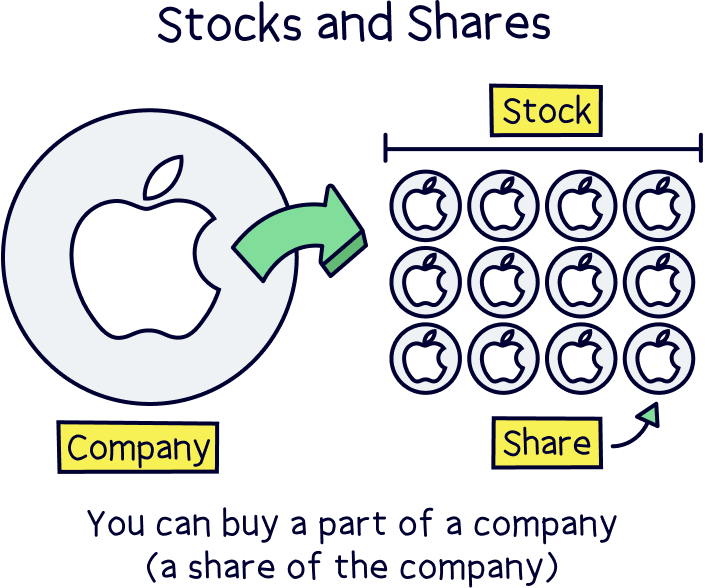

These are where you own part of a company, you own a ‘share’ of a company. Shares are bought and sold on stock exchanges across the world, for instance the London Stock Exchange (LSE) in the UK.

The total of all the shares amount to the total value of the company, and this value and the value of the individual shares can change over time, often due to the performance of the business (e.g. profit), and the stock market in general.

Shares can also pay its profits out to shareholders, which are called dividends.

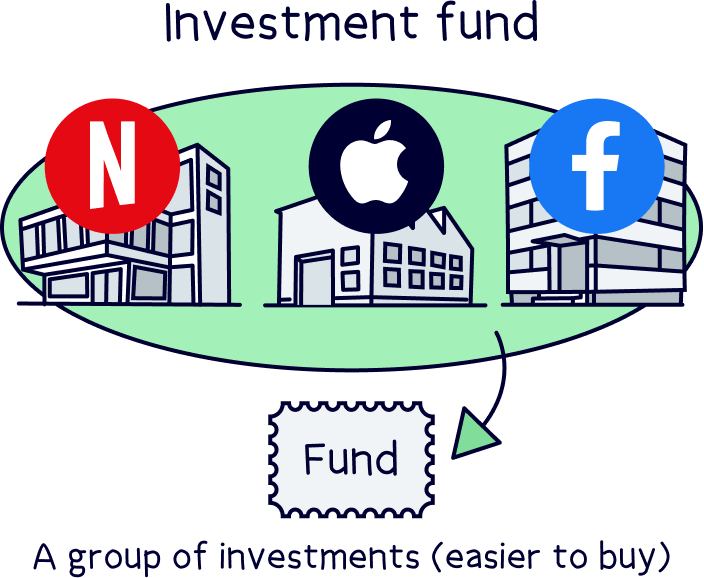

An investment fund, also called a mutual fund, is a collection of lots of different investments all pooled into one single investment. These make investing much easier and cheaper, as you only need to buy a share of an investment fund rather than all the individual investments – so you can build a well diversified investment portfolio very easily (a wide range of investments for long-term growth).

You can have lots of different types of investments, for instance, the top 100 companies in the UK (called the FTSE 100), or a group of similar companies all in the same industry, such as green energy or electric vehicles.

Investment funds can also be traded on stock exchanges, and if so, they are called exchange-traded funds (ETFs) – and are super popular!

Bonds are essentially loans to large businesses (corporate loans) and governments, in return for interest payments. Typically, these are seen as lower risk than stocks and shares (equities).

You can also invest in property, normally as part of an investment fund, and this is typically commercial property such as shops and offices which pay a rental income.

Yep! It’s perfectly safe to save and invest within a Stocks and Shares Junior ISA.

Every ISA provider has to be authorised by the Financial Conduct Authority (FCA), who are the people responsible for making sure your money is well looked after and financial firms are treating you fairly.

You can check if a company is authorised by the FCA by checking the FCA register.

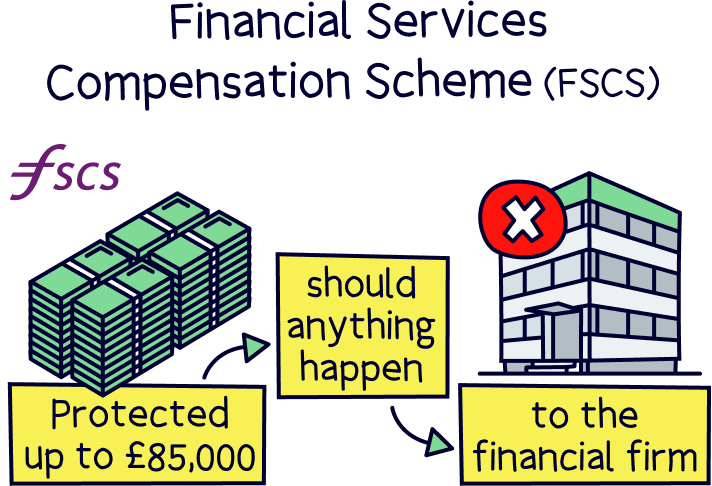

This also means your money is protected by the Financial Services Compensation Scheme (FSCS). This means you could be compensated up to £85,000 should your ISA provider go out of business – although unlikely.

In fact, your money will actually be held with investments with large banks, separate to your ISA provider. All in your name, and can only be returned to you.

However, this doesn’t mean you can’t lose money, and your investments can go down in value. It’s a sensible idea to grow your money with responsible investment strategies over time, such as letting the experts handle things.

There we have it for Stocks and Shares Junior ISAs. We hope that made things clear, and made Junior ISAs understandable. They really are a great opportunity to build a large amount of money for your children over time, all completely tax-free.

By the time they’re 18, they’ll have a head start in life – and could continue investing to build their wealth over time.

As mentioned (a few times!), we don’t recommend making your own investments unless you know what you’re doing. It’s often best to leave it to the experts, but the choice is yours!

Moneyfarm tops the list – they’ve got a great investment record, low fees and experts on hand to help.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Moneyfarm tops the list – they’ve got a great investment record, low fees and experts on hand to help.