Article contents

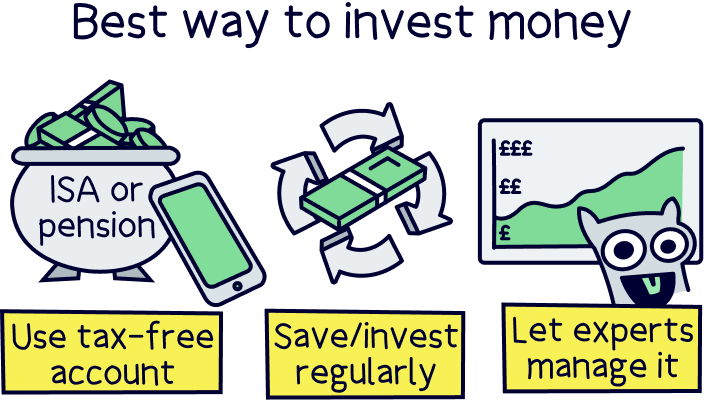

The best way to invest money is simply using the right tax-free investing account, saving regularly, and letting the experts handle your money. As simple as that. It's also cheaper than you might think, and your money could grow (very) large over time.

Looking to get started, or already investing and want to check you're using the right strategy? You’re in the right place. Here’s the best way to invest money in 3 easy steps.

1. Make use of tax-free accounts in the UK

2. Save and invest regularly

3. Let the experts manage your money

Sounds simple right? And it can be. Let’s run through each step in more detail.

Moneyfarm's app is easy to use and their experts can handle the investments.

In the UK, there’s two main tax-free accounts to help you save and invest – a Stocks and Shares ISA and a self-invested personal pension (SIPP). And, if you’re saving for your first home, you could also invest within a Stocks and Shares Lifetime ISA (LISA). (We’ll cover each below.)

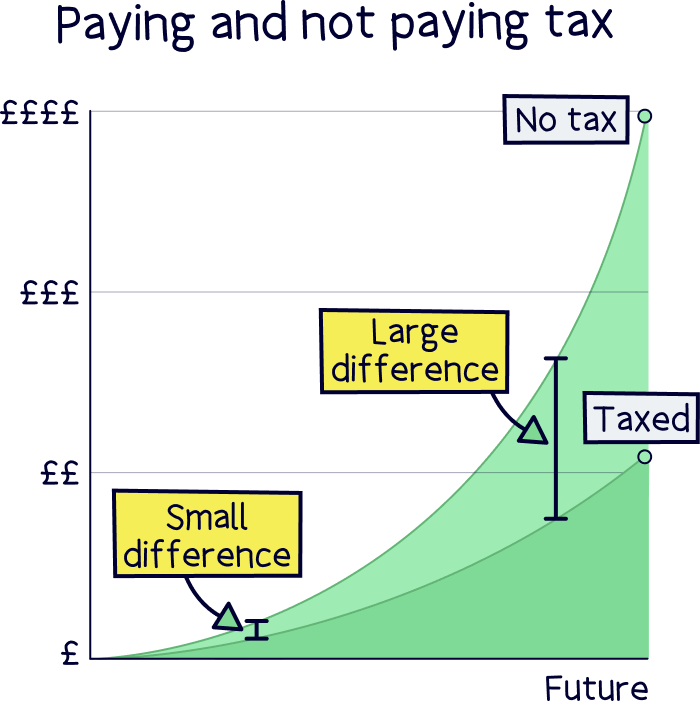

Saving and investing tax-free means your money can grow much quicker – not only will you not pay tax (which can be a lot), but the money you save from not paying tax will have a big impact on your savings thanks to compound interest.

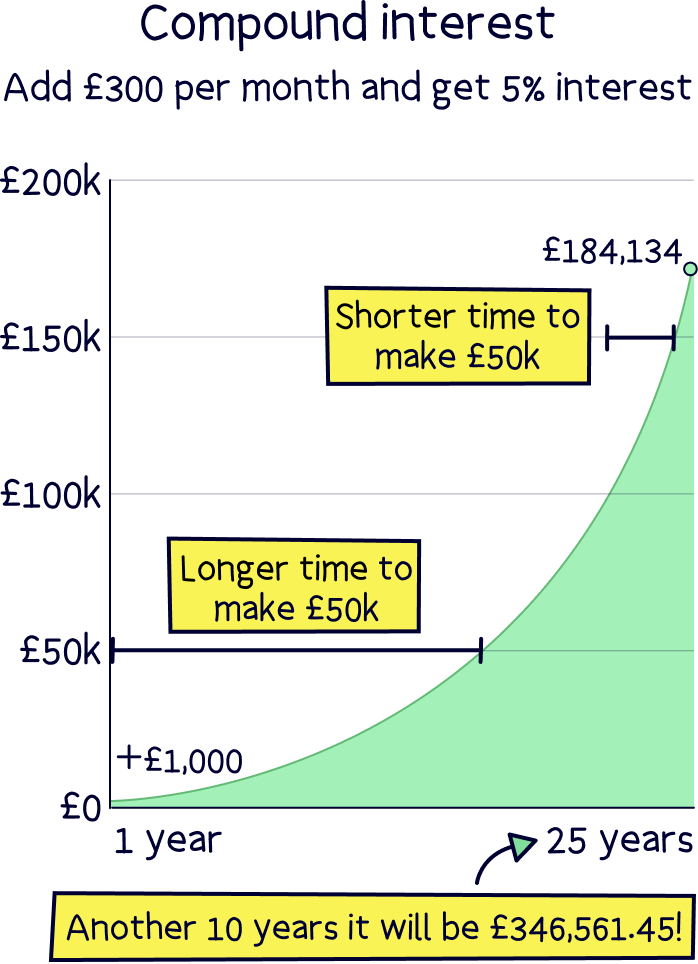

Compound interest is where the money you make starts to make money too, and this snowballs over and over, and over time this has a massive impact. Small savings now, can result in some serious money in the long term.

Imagine you add £300 per month to your account, and it increases by 5% per year – over the first few years, it would grow slowly, and take quite a long time to reach £50,000...

However, as time goes on, all the money you make in interest, is making interest too, and this has a huge impact in the future – where your money would grow much faster, and the time to reach the next £50,000 would be much shorter. Long term investing really pays off over time.

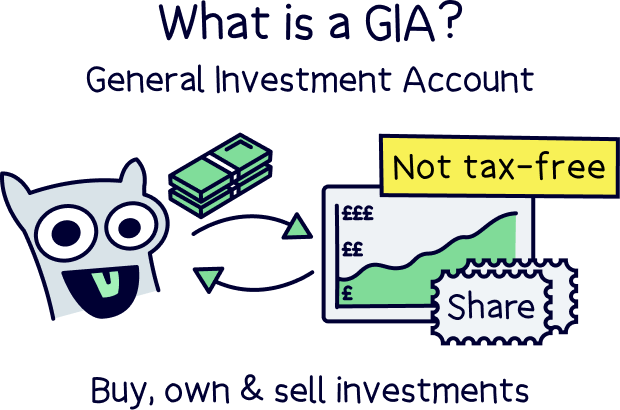

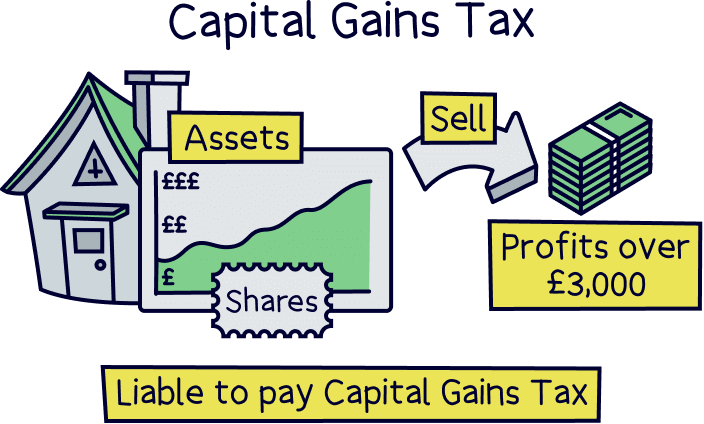

Note: investing outside of an ISA or pension would be within a General Investment Account (GIA), and some of the profit you make could be taxed (if you make over £3,000 per year, and sell investments). These can also be called share dealing accounts.

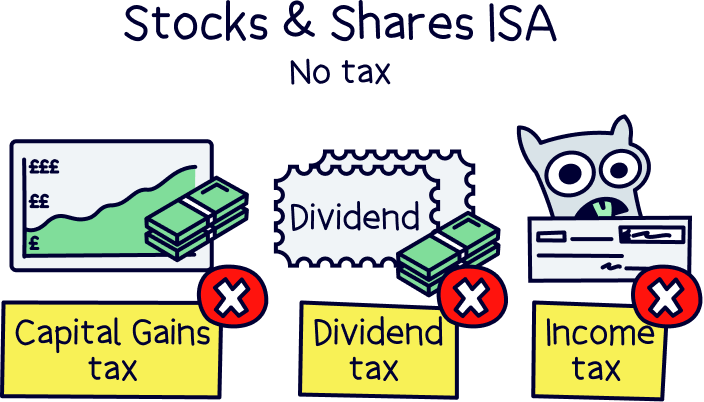

A Stocks and Shares ISA (also often called an Investment ISA), is a type of investment account that allows you to save up to £20,000 per tax year (April 6th to April 5th the following year) completely tax-free. That means that any money you make from your investments, would be tax-free, forever!

Note: your £20,000 ISA allowance is split across all types of ISAs, for instance a Cash ISA, and Lifetime ISA (maximum £4,000).

The tax you could pay is Capital Gains Tax, Income Tax, and Dividend Tax.

Capital Gains Tax is a tax you would pay on any profit you make from selling investments within a tax year – although you only pay this if your profits exceed £3,000 per year (your Capital Gains Tax allowance).

Income Tax is paid on things like your salary, but investments can also pay an income, so you might have to pay Income Tax on any income you might make from your investments too.

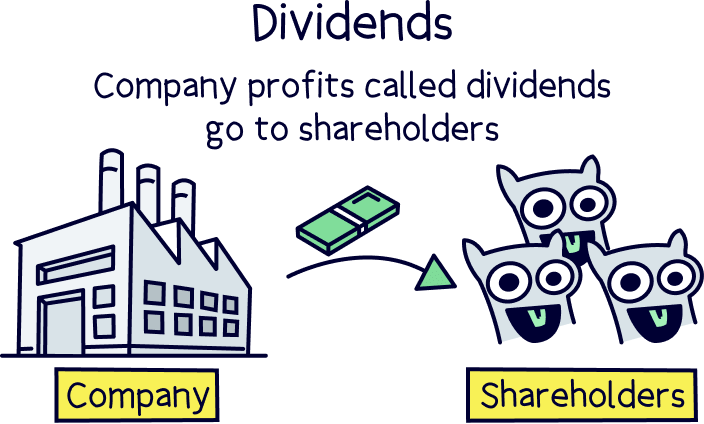

Dividend Tax is paid if a company pays out some of its profits to its shareholders (the owners of the company). This can happen regularly with large, profitable companies such as Apple. There’s currently an allowance of £500 in dividends before any tax is paid.

If you’re keen to avoid paying these taxes and want to invest within an ISA, check out the best Stocks and Shares ISA and see your potential savings with our Stocks and Shares ISA calculator.

And, if you want to make your own investments, check out the best investment platforms in the UK.

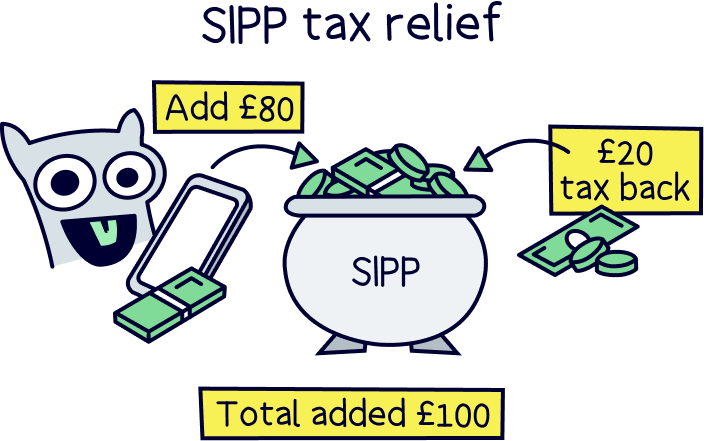

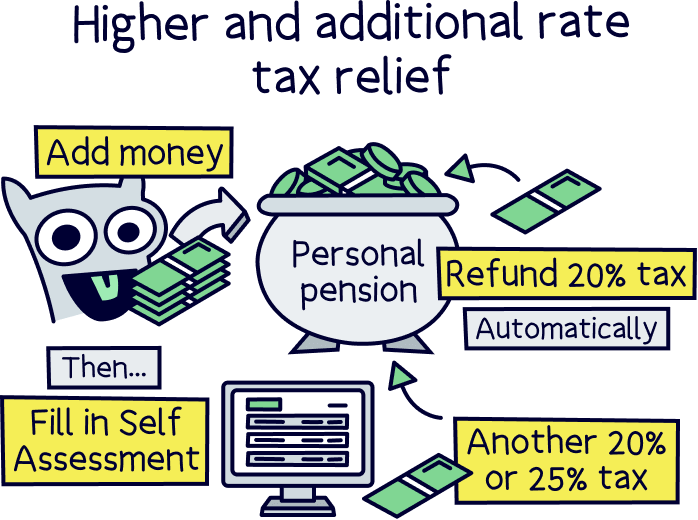

A self-invested personal pension, also called a SIPP, is a pension where you can invest and your money will grow tax-free, but you’ll also get a free 25% bonus from the government on everything you pay in. We’re not joking!

And if you’re a higher rate taxpayer (earning over £50,270, and paying tax at 40%), or additional rate taxpayer (earning over £150,000, and paying tax at 45%), you can claim some of that tax back too (by simply filling out a Self-Assessment tax return).

This ‘free money’ is to refund the tax you’ve paid on your income already, as saving for a pension is intended to be tax free.

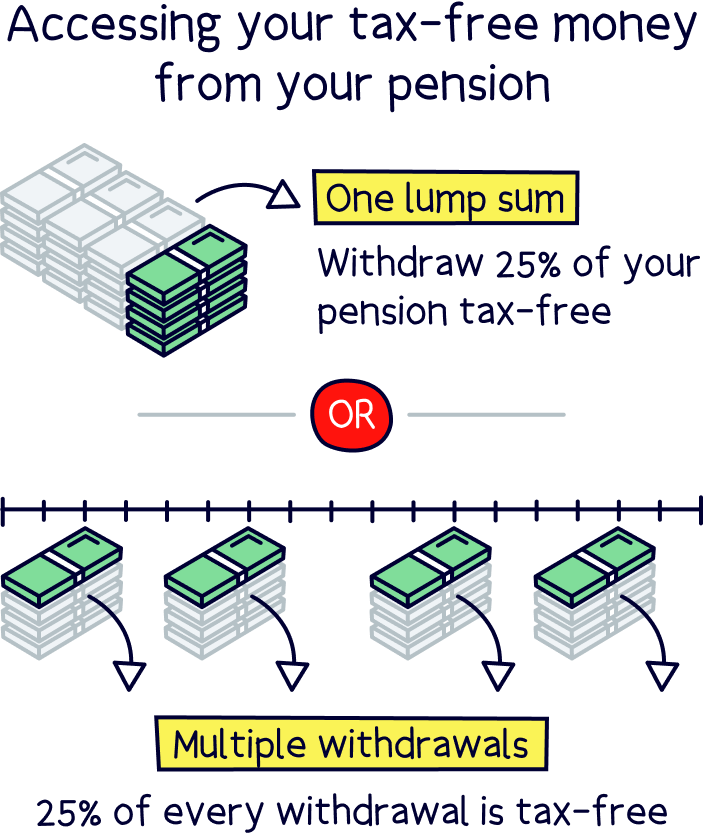

Important: your money will be locked away until you’re at least 55 (57 from 2028), but after that, when you decide to withdraw it, 25% will be tax-free, and with the remaining, you might pay Income Tax, just like your salary now.

With a SIPP, you can invest in a range of investments, such as stocks and shares, and investment funds (covered below). You can even let the experts handle everything for you, such as with PensionBee¹ (5* rated).

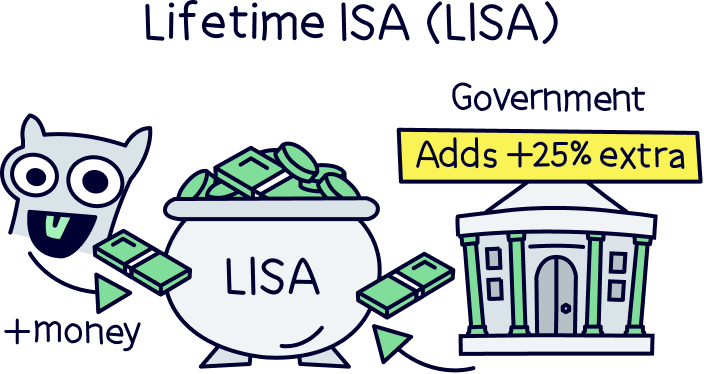

If you’re saving for your first home, you could also save within a Stocks & Shares Lifetime ISA. This is where you save up to £4,000 per tax (which counts as part of your £20,000 ISA allowance), and you get a free 25% bonus from the government on all your contributions.

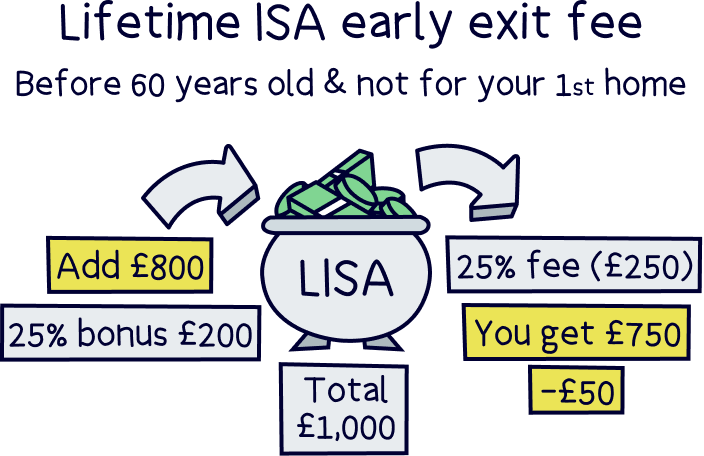

However, you can only use this to buy your first home, and only if it’s under £450,000. If you don’t use it for this, you’ll have to pay a hefty 25% fee to get your money back (which works out as more than your free bonus), or wait until you’re 60 years old.

Nuts about Money tip: if you’re keen to invest in a LISA, here’s the best Stocks and Shares Lifetime ISAs. See how much you could save with our Lifetime ISA calculator.

Unless you’re a professional investor, you probably don’t want to spend all your time and effort looking for new investments, and tweaking and managing your investments daily (your portfolio). Plus, there’s no guarantees that you might be making good investments.

As a general rule, it's best to save and invest regularly (for instance each month when you get paid), and either let the experts handle things, or if you’re confident, select a range of investments that are suited to long term growth (we’ll cover this below).

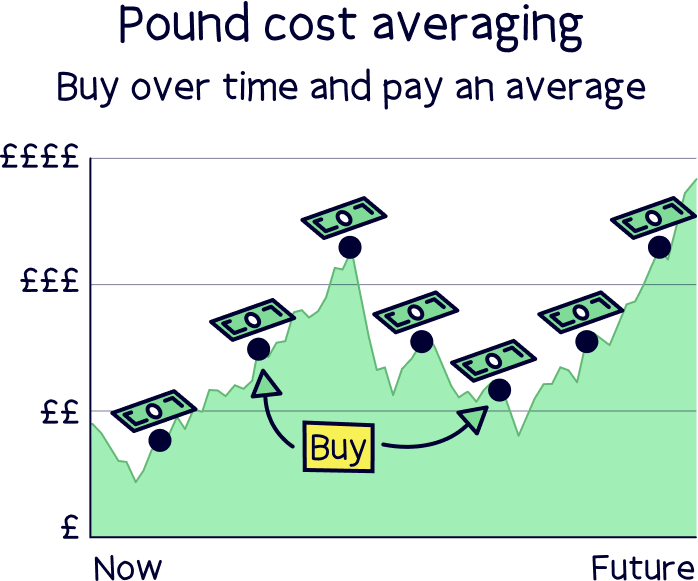

By investing regularly, you are buying investments whatever the price might be at that particular time, this means sometimes it might be high (more expensive), and sometimes it might be low (cheaper) – but over time, the average price you are getting will often work as great value when looking back in the future. This is called pound cost averaging (or more commonly dollar cost averaging).

Nuts About Money tip: this isn’t always a good strategy for individual stocks and shares – it’s typically for long term focused investments.

InvestEngine¹ makes saving regularly easy with their ‘Savings Plan’ option, where your money will be automatically invested within your set investment portfolio – so you don’t need to do a thing, it’s all handled for you.

We also recommend letting the experts handle things when it comes to investing (unless you know what you’re doing). The experts have a lot of experience in managing investments for people, and growing money over time.

Now, we’re not talking about financial advisors – although if you have large amounts of savings getting advice is a great idea. We mean using an investment platform (website or app) that has an option to simply let the experts manage your money.

You can benefit from their knowledge and skills, and great investment strategies to grow your money over time.

Or, if you do want to invest yourself (and usually pay lower fees), you could consider investing with investment funds designed for long term growth over time, or funds that historically grow in value over time, such as index funds, including the FTSE 100 (top 100 largest companies in the UK) and S&P 500 (top 500 companies the US).

You can do this easily with an investment platform. Not sure what one to use? Check out the best investment platforms and the best Stocks and Shares ISAs.

The best investment platforms where experts manage your money.

Get up to £1,000 cashback

Moneyfarm is a great option for saving and investing (both ISAs and pensions). It's easy to use and their experts can help you with any questions or guidance you need.

They have one of the top performing investment records, and great socially responsible investing options too. Plus, you can save cash and get a high interest rate.

The fees are low, and reduce as you save more. Plus, the customer service is outstanding.

Free welcome bonus from £20 to £100. Promo code NUTS.

InvestEngine offers a very low cost way to manage your savings - and their experts handle everything. It's just 0.25% per year (account fee).

The track record is great, and you can manage everything on your mobile (if you want to).

There's a low minimum investment of £100, and you'll be able to save and invest within a tax-free Stocks & Shares ISA too, so your money can grow faster.

You can also make your own investments alongside, and all for free (ETFs only).

Moneyfarm's app is easy to use and their experts can handle the investments.

The best investment platforms where YOU manage your own investments.

Moneyfarm's app is easy to use and their experts can handle the investments.

eToro is one of the best investment platforms out there - and is by far the most popular, with over 30 million customers.

Why? eToro is very low cost (commission-free stocks), easy to use, and has lots of awesome trading features. There's also a community of other traders to learn from and even copy.

It’s also got the largest range of assets to trade and invest in – including stocks, ETFs, crypto, CFDs, currencies and commodities (such as gold).

Deposit £50, get 10 free trades

Lightyear is a great, low cost investing and stock trading platform. There’s a good range of investment options (over 3,000 stocks and ETFs), you can store multiple currencies, and the app itself is modern and super slick.

ETFs are completely free, and stocks are £1/$1/€1 per order.

There's also very low currency conversion fees of 0.35%, or you can hold the currency itself, and avoid this fee.

Company accounts: you can also invest as a business (e.g. limited company), and benefit from all the same low fees and great experience. Just select 'business' in the top of their website after you click through.

Get fractional shares worth up to £100

Trading 212 is a platform built for everyone in mind – there's over 2,000,000 customers! It’s great for beginners to get started, and perfect for experienced traders looking for more advanced trading options, such as CFDs, meaning you can trade with leverage (borrowed money), and trade the price going down (go short). There's all the trading tools you’ll need too, such as stop-loss and limit orders.

It’s one of the cheapest platforms out there with low fees when buying foreign stocks (currency conversion fee).

Platform experience: good

Device options: website & phone app

Support: 24/7

Stocks & Shares ISA: yes

Pension (SIPP): no

Range of investments: large

Stocks: yes

ETFs: yes

Fractional shares: yes

Crypto: no

CFDs: yes

Forex: no

Account fee: free

Cost per trade: free

Spread fees: yes (low)

Currency conversion fee: 0.15% on stocks, 0.50% on CFDs

• Low cost trading

• Huge range of investment options

• Hold and trade in multiple currencies

• Very low foreign exchange fees (0.15%)

• Offers an ISA

• Offers CFD trading (alongside regular investing)

• Great mobile app

• Lots of resources to learn

• Awesome customer service

• No minimum investment

• Fractional shares

• No personal pension (SIPP)

If you’re not quite sure about all the different types of investments you could invest in, don’t worry – not many actually do! That’s why we often recommend letting the experts handle things. Let’s run through them now.

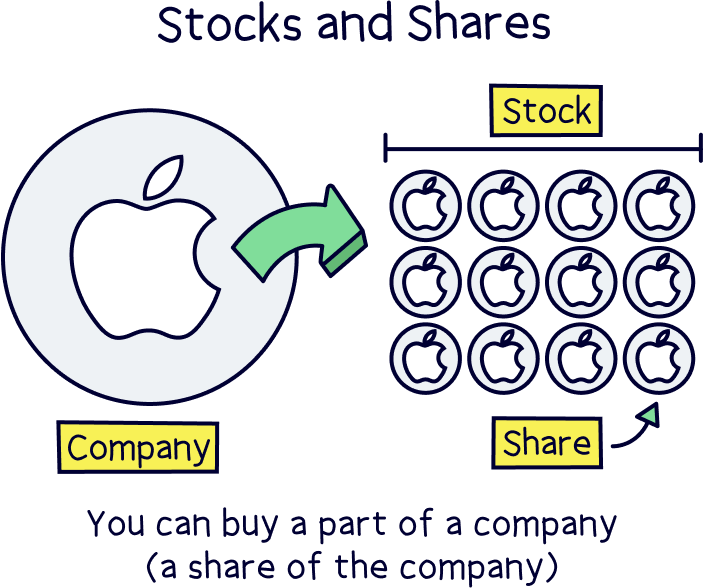

Stocks and shares are where you buy and own part of a company, you buy a ‘share’ of a company. Shares are traded on stock exchanges all over the world (stock market), such as the London Stock Exchange (LSE) in the UK, and the New York Stock Exchange (NYSE) in the US.

All the shares of a company combined equal the total value of the company, and typically, when a business grows (it makes more money), the value of the company increases, and so does the share price.

Profitable companies can also pay out their profits to shareholders, which are called dividends.

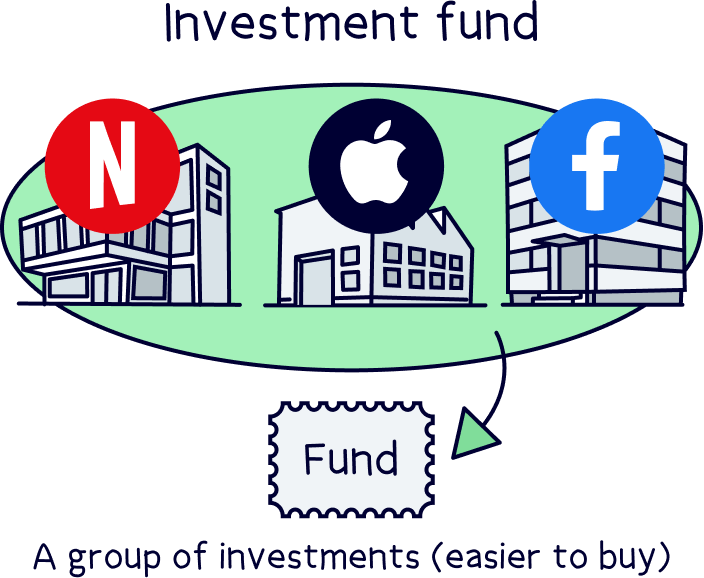

Investment funds are a group of investments (such as shares of a range of different companies), all pooled together into a single investment. This makes it much easier to buy a wide range of investments, and can be a lot cheaper than buying all the shares individually. They’re also often called mutual funds.

Investment funds are managed by an investment manager (known as a fund manager), and can be actively managed (investments chosen by the fund manager), or they could track certain groups of things (known as an index), such as the top 100 companies in the UK (FTSE 100). Or, even things like companies that pay dividends – there’s a huge range of different options.

Investment funds can be bought and sold on stock exchanges, just like shares, so bought and sold whenever you want to (during opening hours of the stock market), and if they can be, they’re known as exchange-traded funds (ETFs).

Note: instead of investing money in things such as shares, investment funds can also deposit their money with high interest savings accounts and earn interest instead. These are called money market funds, or cash funds. Here's the best money market accounts in the UK.

Bonds are where you effectively loan your money to a government (government bonds) or large corporations (corporate bonds), in return for interest payments. The bond (loan) will have a date it matures, at which point, you’ll get your money back, plus all the interest during that time.

Commercial property such as offices and shops can also be an investment – and can make up part or all of an investment fund. This can provide a regular income (in the form of rent).

If you’re just getting started and want to make your own investments and create your own investment portfolio (your collection of investments) – it’s typically a good idea to start with investment funds, rather than individual stocks and shares.

Investment funds have a huge range of different structures and goals – all suited to different investors, but the best way to invest money is simply for long term growth (especially if you’re a beginner).

Investment funds for long term growth are kind of like a pre-built investment portfolio, which can be well diversified (a range of well suited, different investments), with investments selected for long term growth.

Trying to pick individual stocks and shares yourself, or buying the next trending stock (such as Tesla), can work out as a great short term investment, but typically not suited for long term growth. It’s a strategy more suited to day trading (lots of short term trades).

If you want to invest in investment funds check out the best ETF platforms.

Yes, it’s very safe to invest money if you follow our recommendations.

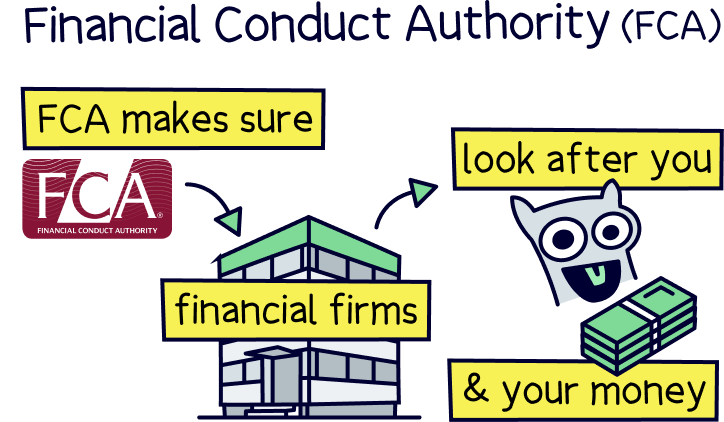

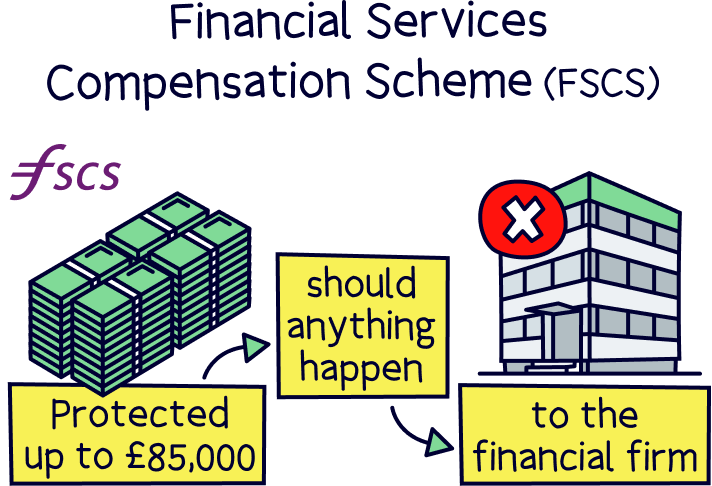

All financial services companies need to be authorised by the Financial Conduct Authority (FCA). They’re the people who make sure companies are looking after their customers and their money.

This also means that your money is protected by the Financial Services Compensation Scheme (FSCS), which means you could be compensated (up to £85,000), should the company holding your money go out of business.

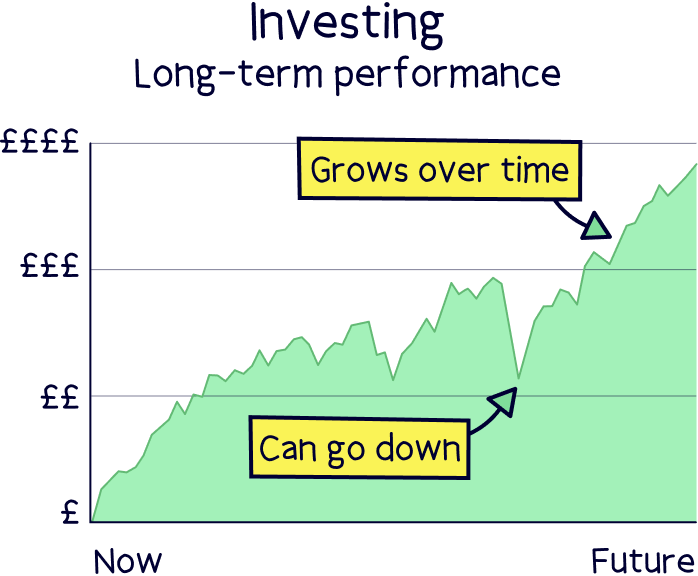

However, this doesn’t mean you can’t lose money – your investments could go down in value. But with a focus on long term growth (rather than short term investments), which experts typically have, your money should grow over time (with ups and downs along the way).

If you’re not sure investing is right for you, don’t worry, it’s not for everyone, and you do have other options – although typically, sensible investing has the best results over the long term.

You could simply save your money as cash, and earn interest on it each year. There’s two options for this, a savings account, and a Cash ISA.

A savings account is a great option to earn interest on your money, you simply sign up, add money to the savings account, and you’ll start earning interest (money).

There’s a few different types of savings accounts depending on when you might need the money back.

A popular option is an easy access savings account, where you can get your money back whenever you like, here’s our best easy access savings accounts to learn more.

Or, you could lock your money away for a set period of time, anywhere from 7 days to 5 years, in exchange for what can be a higher interest rate (but not always). These can be called notice accounts (where you give notice to get your money back), or simply fixed term savings accounts.

With a fixed term account. you won’t be able to access your money without hefty fees. Check out the best savings accounts to learn more about all your options. An easy access account can often be a better option for most people.

Note: you might have to pay tax on your interest, depending on how much you make – typically you’ll have to earn over £1,000 in interest before paying tax (your Personal Savings Allowance).

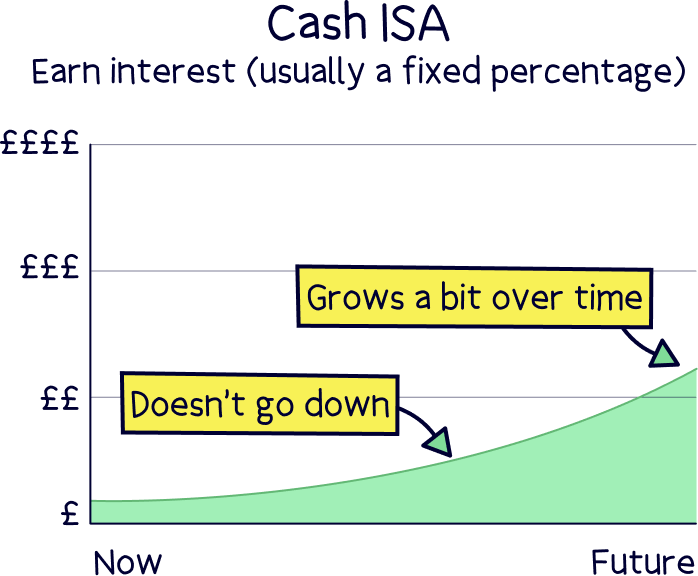

With a Cash ISA, all of the money you earn (interest) is tax-free – which means your money could grow more over time.

However, the interest rates are typically much lower than a regular savings account, and you may not end up paying tax on your interest anyway (thanks to the £1,000 tax-free, Personal Savings Allowance).

Well, there we have it – the best way to invest money. Simpler than you think? Let’s run through it again quickly.

So, there’s 3 simple steps to investing the best way (in the UK):

1. Make use of tax-free accounts

2. Save and invest regularly

3. Let the experts manage your money

Making the most of tax-free accounts such as a Stocks and Shares ISA, or a self-invested personal pension, can mean your money grows tax-free, saving you a small fortune in tax, but also means your money can grow much quicker, thanks to compound interest (money earning more money).

With a pension, you’ll also get a 25% bonus on your contributions – added to your pension automatically. How great is that? But hold your horses, you will have to pay tax when you start withdrawing your money (depending on how much you earn at the time). Although 25% will always be tax-free.

Saving and investing regularly is the key to building up your savings. You’ll benefit from compound interest again – so even small amounts every month can have a big impact in the future.

And finally, simply let the experts handle your investments, unless you know what you’re doing.

Experts know what they’re doing (it’s their job!), and know the right investment strategies to grow your money sensibly over time. It can also save you a lot of time and effort.

We recommend simply using an investment platform that offers expert-managed investing, and offers a tax-free investment ISA. Here's the best investment platform managed by experts. And if you do want to manage your own investments, here's the best investment platform for beginners.

Finally, if you’re only looking to save for a pension, here's the best private pensions.

And that’s it. All that’s left to do is wish you all the best with your investing!

Moneyfarm's app is easy to use and their experts can handle the investments.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Moneyfarm's app is easy to use and their experts can handle the investments.