Article contents

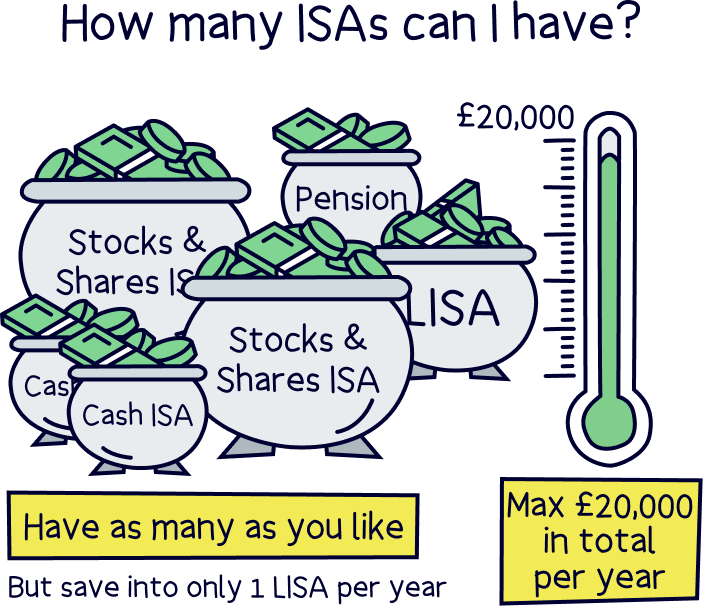

You can have more than one ISA – in fact you can have loads of ISAs! There’s no limit, and you can have lots of all the different types (Cash ISA, Stocks and Shares ISA, Innovative Finance ISA and a Lifetime ISA). Although you can only save into one Lifetime ISA each tax year, you can go crazy with the rest.

Worried about having too many ISAs? Fear not. You can have as many as you like, and as many of all the different types of ISAs too (except Lifetime ISAs – more on those later).

And open lots of the same type of ISA within the same tax year too (thanks to some government changes in 2024).

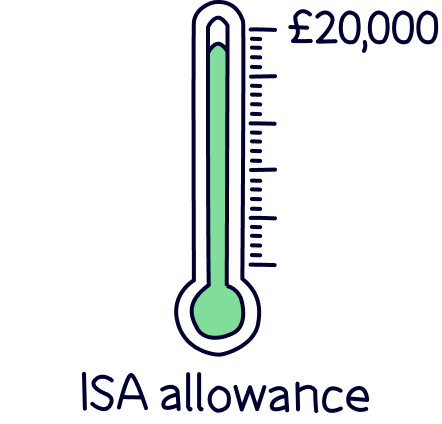

So, you could have 2 Cash ISAs and 5 Stocks and Shares ISAs, whatever you decide. The only limit you have is saving £20,000 per tax year (April 6th to April 5th the following year), across all of your ISAs (your annual ISA allowance).

By the way, an ISA is an Individual Savings Account. It allows you to save and grow your money, tax-free. Yep, that’s right. No tax at all.

If you are just here to check if you can save into a new ISA, well yes you can, go wild! But before you go, make sure you’re using one of the best ISAs out there…

We’ve reviewed all the top ISAs for each type of ISA, Cash ISAs, Stocks and Shares ISAs, and Lifetime ISAs (we’ll cover what they all are below). And here’s the best:

A great and easy to use investing app. Add money from your bank or transfer an ISA, investments handled by experts. There’s a pension pot too.

Get up to £100 free share

Lightyear is a great, low cost investing and stock trading platform. There’s a good range of investment options (over 3,000 stocks and ETFs), you can store multiple currencies, and the app itself is modern and super slick.

There's no account fees and no trading fees. There's also very low currency conversion fees of 0.35%, or you can hold the currency itself, and avoid this fee.

Company accounts: you can also invest as a business (e.g. limited company), and benefit from all the same low fees and great experience. Just select 'business' in the top of their website after you click through.

Moneyfarm is a great option for saving and investing (both ISAs and pensions). It's easy to use and their experts can help you with any questions or guidance you need.

They have one of the top performing investment records, and great socially responsible investing options too. Plus, you can save cash and get a high interest rate.

The fees are low, and reduce as you save more. Plus, the customer service is outstanding.

Pros

Cons

A great and easy to use investing app. Add money from your bank or transfer an ISA, investments handled by experts. There’s a pension pot too.

A great and easy to use investing app. Add money from your bank or transfer an ISA, investments handled by experts. There’s a pension pot too.

Easy to use

A great and easy to use investing app. Add money from your bank or transfer your existing ISA, with the investments handled by experts. There’s a pension pot too.

The customer service is excellent, and has email and phone support based in the UK.

Beach is an easy to use investing app (and easy to set up), just add money and the experts handle everything. It’s all managed on your phone with a great app, and you can see your total savings whenever you like.

You’ll get an easy access pot (access money in around a week), which can be an ISA where all the money you make is tax-free (save up to £20,000 per tax year), and a standard account for those saving in addition to this (or who don’t want an ISA), where there’s no contribution limits (but also no tax-free benefits).

The investments are managed by experts from the largest investment company in the world (BlackRock). And they consider things like reducing climate change, meaning your savings could make the world a little better in future too.

There’s also an optional pension pot to save for retirement, so you can keep all your savings in one place, and if you’ve got lost or old pensions, Beach can also find them and move them over too.

Fees: a simple annual fee of up to 0.98% (minimum £4.99 per month).

Minimum deposit: £25

Customer service: excellent

Pros:

Cons:

Get up to £100 free share

Lightyear is a great, low cost investing and stock trading platform. There’s a good range of investment options (over 3,000 stocks and ETFs), you can store multiple currencies, and the app itself is modern and super slick.

There's no account fees and no trading fees. There's also very low currency conversion fees of 0.35%, or you can hold the currency itself, and avoid this fee.

Company accounts: you can also invest as a business (e.g. limited company), and benefit from all the same low fees and great experience. Just select 'business' in the top of their website after you click through.

A great and easy to use investing app. Add money from your bank or transfer an ISA, investments handled by experts. There’s a pension pot too.

Top rate

Saving for your first home? Moneybox could be for you.

Moneybox is the go-to place for Lifetime ISAs – it’s easy to use, and you’ll be able to manage everything on a great mobile app.

You can either pick from saving cash (Cash Lifetime ISA), and benefit from a great savings rate. And there’s no fee for saving cash.

Or, you can make your own investments (Stocks and Shares Lifetime ISA), and pick from a range of investment options (including individual US shares such as Apple and Amazon). Fees will apply.

Moneybox will handle everything behind the scenes, and collect your 25% government bonus and automatically add it to your account.

Overall, it’s low cost overall, and the customer service is excellent.

Note: don’t wait to get started, as you’ll need to wait 12 months before you can use your LISA to buy a home – all you need to do is add £1.

Top rate

Tembo is one of the best Lifetime ISAs out there – it’s got one of the best interest rates out there, and it’s easy to use, with a great app on your phone, packed with tools to help you save more.

They’ll also transfer your existing Lifetime ISA over if you have one too (they’ll handle everything).

There’s two options, a Cash LISA (with the top interest rate), or a Stocks and Shares LISA, where you can simply let the experts handle things, and aim to grow your money more over time).

They'll also be able to help you with the mortgage when the time comes to buy your first home – and help you borrow more if you need to.

The customer service is top notch too.

You can open and save money into as many ‘normal’ ISAs as you like. However, there’s one exception, you can only save into one Lifetime ISA each tax year.

Lifetime ISAs are really great at saving for your first home, and come with a whopping 25% government bonus – we’ll cover Lifetime ISAs in more detail just below, if you’re not sure what they are.

But, you can transfer Lifetime ISAs across providers (companies) if you decide you want to start saving with a different provider – perhaps one that’s got a higher interest rate, or easier to use. By the way, we’ve reviewed all the best Lifetime ISAs, and some have got pretty great interest rates these days, as a reminder scroll up or click top Lifetime ISAs.

You can also transfer Cash ISAs, and Stocks and Shares ISAs too – more on that later.

There are four main types of ISAs:

There are also Junior ISAs (savings accounts for your kids), but being young and free, they dance to their own tune. We dive deeper into those in our guide to Junior ISAs. You can’t have more than one of each type of Junior ISA, but you can have one of each (a Cash Junior ISA and a Stocks and Shares Junior ISA).

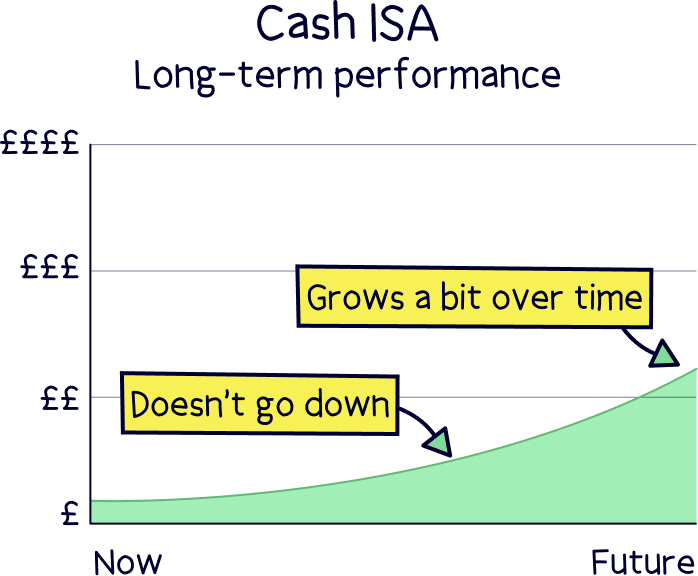

You put cash in. It earns you interest. The interest you earn is tax-free (you might pay tax on interest you earn outside of an ISA, within a regular savings account).

There are two main types of Cash ISA:

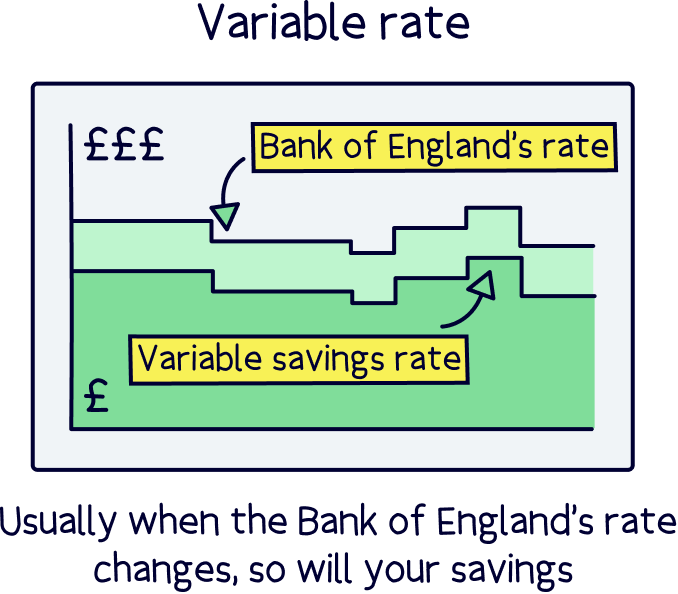

Where your interest rate can change over time. Normally in-line with the Bank of England base rate, which is the interest rate banks themselves borrow money for, but also get paid the same amount for storing money with the Bank of England.

So if this increases, they sometimes pass this onto customers, and the customer gets a higher interest rate too. And if the Bank of England lowers the base rate, the customer's interest rate will often go down too.

Where your interest rate stays the same over a set amount of years. These often have the highest interest rates as you are agreeing to keep your money with a bank for a long period of time, normally 1-5 years.

Scroll up to see our top picks or click top Cash ISAs.

Also called ‘Investment ISAs’, these allow you to invest your money in:

You might have heard that Stocks and Shares ISAs are risky and complicated. But this is actually not true! They’re great for long-term investing (if you let the experts manage them), and everyone, whatever your knowledge or experience, can open one easily and start growing their savings, tax-free.

With most Stocks & Shares ISA, the investments are managed by experts, with the aim of growing your money sensibly over time (they do go up and down in value). These are typically called managed Stocks and Share ISAs.

But, you can also make your own investments, sometimes called a self-select ISA, where you’ll buy and sell investments you decide, whenever you like. This can be great for more experienced investors.

To see our top picks scroll up or click top picks for Stocks and Shares ISAs.

Innovative Finance ISAs allow you to lend out your savings to individuals or companies through what is called a ‘peer-to-peer lending platform’. This cuts out the middle-man – i.e. the bank. Borrowers then have to pay the money back over time – with interest. And most of that interest is for you.

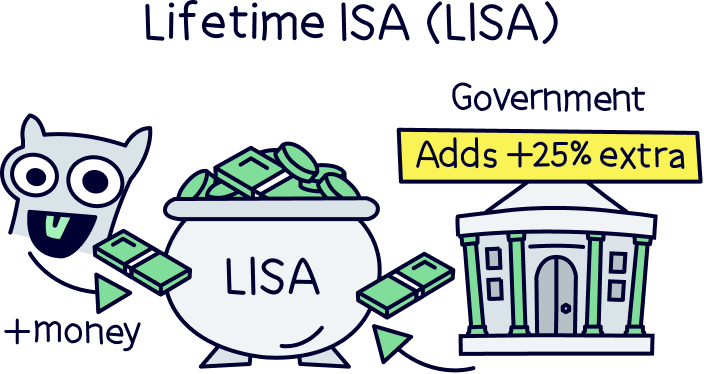

If you’re saving to buy your first property or you’d like to save for later in life (over 60) in addition to a pension, a Lifetime ISA offers some serious perks. You can save up to £4,000 and the government will give you a 25% on the amount you save.

That’s potentially an extra £1,000 per year. Completely free!

Note: this £4,000 allowance counts towards your £20,000 total annual allowance.

Learn more with our guide to Lifetime ISAs.

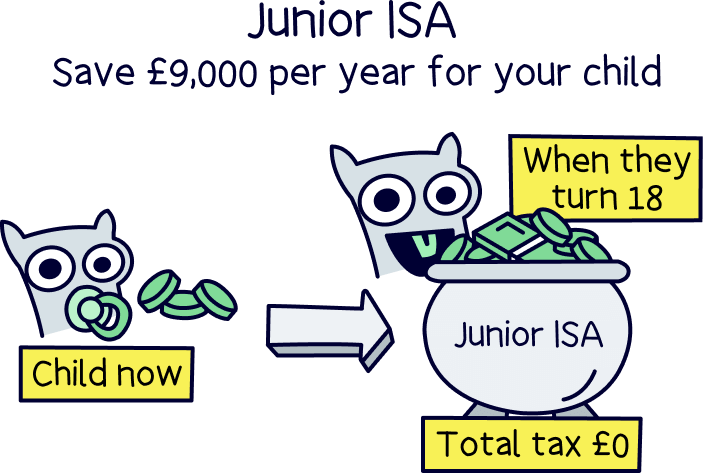

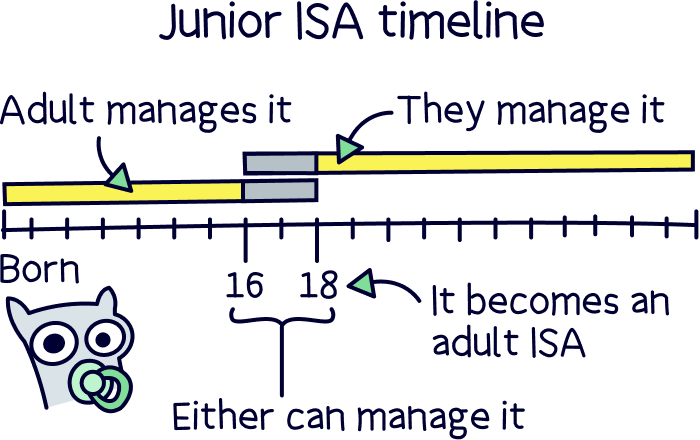

Looking to open a long-term savings account for your kid’s future? A Junior ISA (or JISA) is a great option. You can opt for a Junior Cash ISA or a Junior Stocks and Shares ISA. (a Junior Stocks & Shares ISA is far better for long-term saving).

It will be in their name, and technically their money, which they’ll be able to access when they turn 18.

And because it’s your kids money, Junior ISAs are not included in your annual £20,000 ISA allowance. They have their very own allowance that is separate. (Right now, it’s £9,000.)

Learn more with our guide to Junior ISAs.

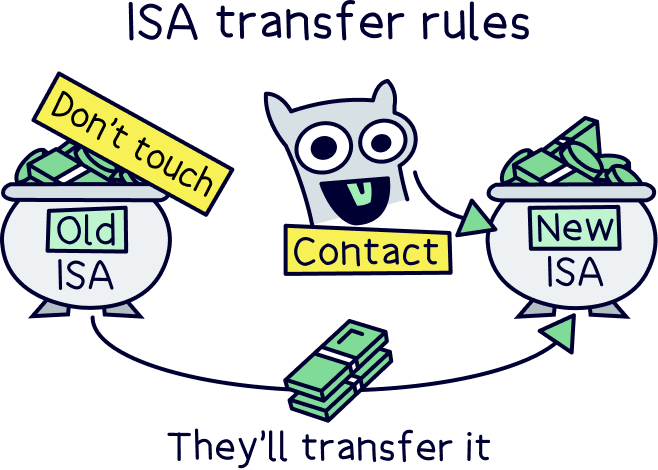

If you’ve already got an ISA, and want to switch providers, you can either set up a new account with the new provider, and keep your old one – or simply transfer your ISA to your new provider.

This means your cash (if you have a Cash ISA), or your cash and investments (if you have a Stocks and Shares ISA), will be moved to your new provider.

You can even transfer just part of your ISA, it doesn’t have to be the whole amount. This is called a ‘partial transfer’. (Except Lifetime ISAs and Junior ISAs, where you have to transfer the full ISA).

Transfers are really simple to do. Just let your new provider know you want to transfer your old ISA, and they’ll take care of everything. They’ll get in touch with your old provider, sort all the paperwork, and your money or investments will simply appear in your new ISA after a few weeks.

You can even transfer a Cash ISA to a Stocks and Shares ISA if you want to (and vice versa).

It should take no more than 30 days, but with some reluctant providers, it can take a bit longer.

Nuts About Money tip: don’t withdraw money from your old ISA and then add it into your new ISA, as it will count towards your annual ISA allowance (£20,000), so you might not be able to add more cash in later on. It’s always best to transfer it, which won’t affect your allowance.

So, there we go. You can have as many ISAs as you like, and save tax-free into all of them at the same time.

That’s except Lifetime ISAs, where you can only save into one per tax year.

Every year, you can use your £20,000 ISA allowance however you like across all of the ISAs, except from a maximum of £4,000 per year for Lifetime ISAs.

For long term saving, we recommend you open a Stocks & Shares ISA. You’ll likely earn a lot more money than a Cash ISA over time. They’re super easy to set up and it’s all managed for you by experts. To view our top picks scroll up or click top Stocks & Shares ISA, or check out all the top options with our guide to the best investment platforms.

And if you are interested in a Cash ISAs here's our Cash ISA picks and our Lifetime ISA picks.

And if you’ve got kids, you can also have a Junior ISA, which is completely separate, and in your kids name, and you can put £9,000 in per year. Find out more with our Junior ISA article.

Happy saving!

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

A great and easy to use investing app. Add money from your bank or transfer an ISA, investments handled by experts. There’s a pension pot too.