Article contents

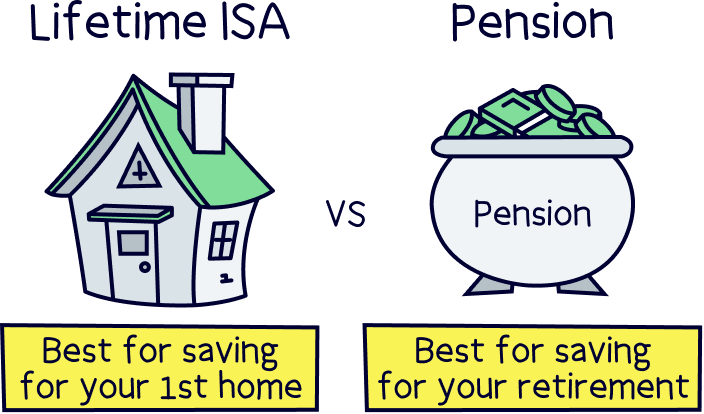

Lifetime ISAs and pensions are both great for long-term saving. You can have both, but a Lifetime ISA isn’t designed as a replacement for a pension – it’s a useful addition, but more suited to those saving for their first home. If you’re not saving for a home, a pension wins hands-down.

Lifetime ISAs and pensions are both designed to help you save for later in life. However, a Lifetime ISA (a.k.a. LISA) is also there to help you save for deposit on your first home. We’ll explain everything you need to know about Lifetime ISAs, and compare the benefits of a Lifetime ISA vs paying into a pension (and how best to do it).

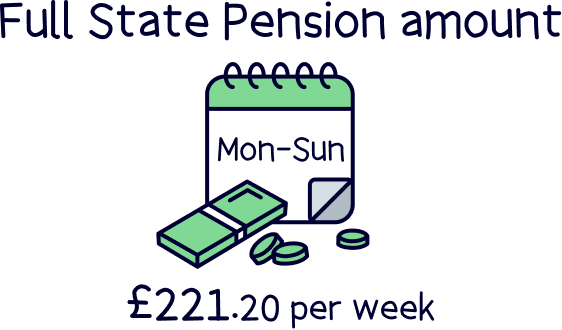

You might be thinking, I've got the State Pension when I retire so what's the point in saving for retirement myself? (That's the pension from the government when you reach 66, or 67 in 2028, and maybe extended a lot further in future).

Well, unfortunately the State Pension probably won't be able to cover much of your bills and lifestyle when you retire. At the moment it's £221.20 per week, which is of course great to have, and is a lifeline for many people. But do you think you could live on that now with the lifestyle you want?

Most people, just like us, want a slightly bigger retirement income to live comfortably, and that comes from their own pension and retirement savings. Which brings us to the question: what's the best option to save for retirement, a LISA or a private pension?

We've done the hard work for you – here’s the best personal pensions to save for your retirement.

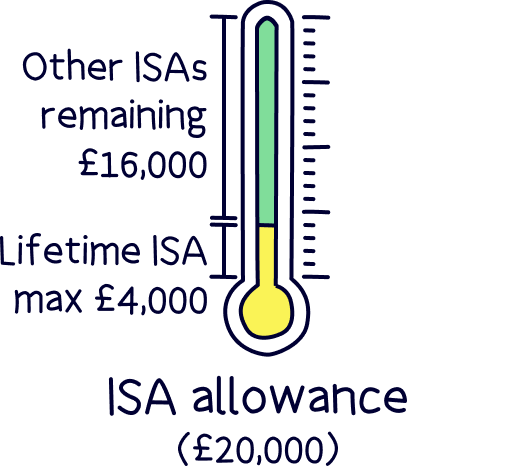

Everyone who is a resident in the UK can open an ISA – an Individual Savings Account. You can invest £20,000 in ISAs every year (this is called your ‘ISA allowance’) and you don’t have to pay any tax when your money grows in those accounts. Result!

(Your money can grow from interest when you have a Cash ISA, or from investment returns when you have a Stocks and Shares ISA. Read about the difference between these types of ISA here: Cash vs Stocks and Shares ISA).

If you're interested in investing yourself, learn more with our best investment platforms UK and best trading platforms UK.

Now, what about your Lifetime ISA?

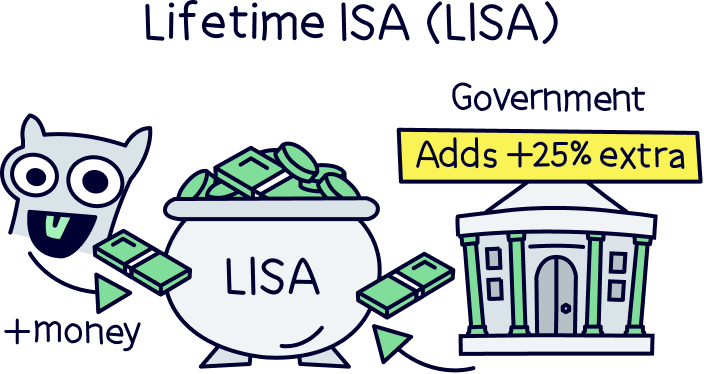

Your Lifetime ISA comes with a 25% bonus on everything you put in. In other words, the government will top-up your savings every time you pay in. If you deposit £1,000 into your Lifetime ISA for example, the government will add £250 – no questions asked.

These savings – plus bonuses – also gain interest in your Lifetime ISA (if it’s aMoneybox Cash Lifetime ISA). So that’s a double-win. And if you choose a Stocks and Shares Lifetime ISA, the money will be invested (by professionals) in the stock market, and it’ll grow over time as those investments become more valuable.

Note: Stocks and Shares Lifetime ISAs are your best bet, because the returns you get over time vastly exceed what you can get from a Cash Lifetime ISA. More on that later.

If you're interested in getting a Lifetime ISA, speak to Tembo¹, they specialise in them, plus their app is easy to use and their service is excellent.

If you’re a UK resident and you’re between the ages of 18 and 40, you can open a Lifetime ISA. If you’re a British citizen abroad, you need to be a crown servant (e.g. in the armed forces).

After you open your Lifetime ISA, you can save up to £4,000 every tax year – between 6th April and 5th April every year. The government will add your 25% bonus at the end of every tax year.

This means that if you put away £4,000 in a year, you’ll get an extra £1,000 as a bonus. Nice!

There are two different types of LISA, a Stocks & Shares LIfetime ISA and a Cash Lifetime ISA.

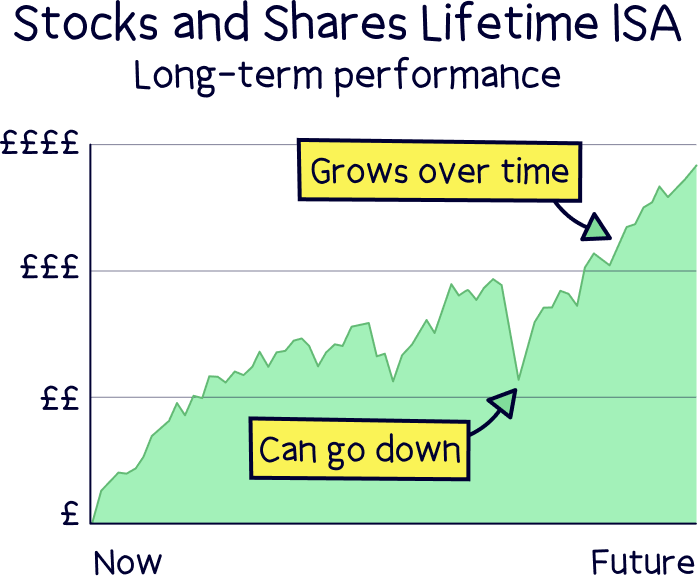

This is where your money is invested in the stock market. Your ISA provider (the company that manages your ISA) will invest in things like stocks and shares, bonds, and ETFs:

Your money is in expert hands, and in the long term the returns on a Stocks and Shares LISA should vastly outperform the interest you’d get if you were putting the money away in a savings account or Cash ISA (explained below). Stocks and Shares ISAs are always a long-term play, meaning you ride out all the temporary ups-and-downs of the stock market.

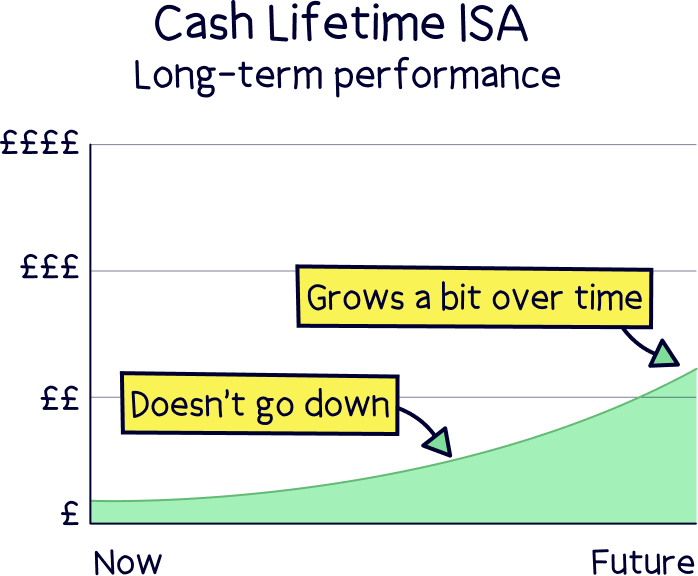

This is where your money sits in theaccount and builds interest. The problem with interest is that interest rates are crazy low, and are way behind the rate of inflation.

Inflation? Huh? Inflation basically means the rising costs of goods and services. When the interest you earn on savings is less than inflation (it is right now, and will be for the foreseeable future) the ‘buying power’ of your cash actually reduces. If you earn 1% interest but the inflation rate is 6%, your money will buy you less in the future, not good!

But there’s an important difference between a ‘normal’ Cash ISA and a Cash Lifetime ISA: the 25% bonuses you get from the government certainly does outpace inflation. It’s just that you can expect to earn even more when you choose a Stocks and Shares LISA – but only in the long term.

If you’re buying your first home in a year or two, it’s probably better to open a Cash Lifetime ISA and just pocket the free cash from the government.

Visit Tembo¹ if you’re interested in getting a Lifetime ISA.

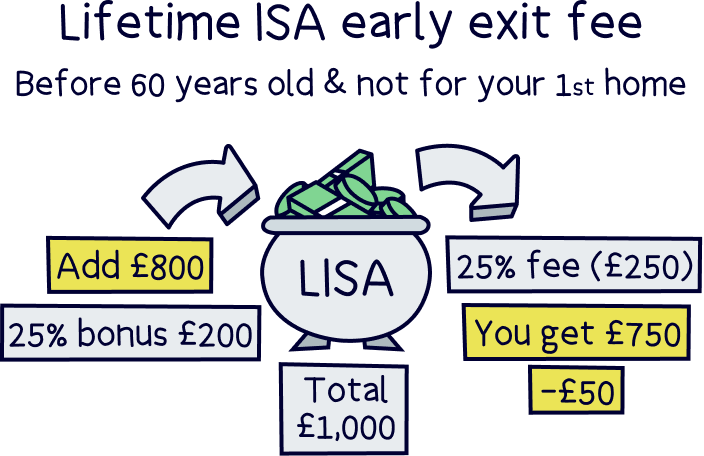

You can only withdraw money from your Lifetime ISA for two reasons:

You can technically take money out whenever you want, but you’ll incur a 25% penalty if you do it for another reason. This means you’d lose all the bonuses the government gave you alongside 5% of your own cash, and if your account has gone up in value you'd lose a lot more too – so it’s not recommended!

You can pay into your Lifetime ISA until your 50th birthday, and you must make your first payment into your Lifetime ISA before your 40th birthday.

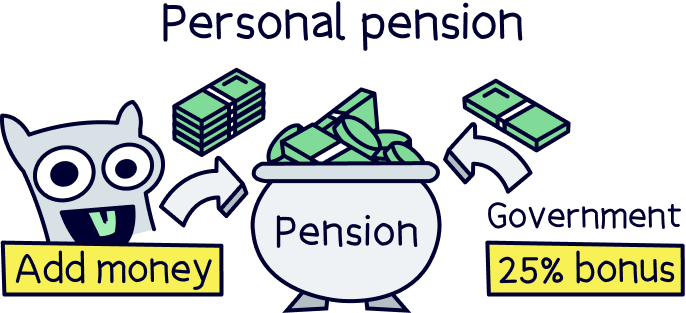

A pension is similar to a LISA in many ways: it's a pot of money that you pay into throughout your working life, which financially supports you after you retire. Pension providers will invest your money (in stocks and shares etc, just like a Stocks & Shares ISA), with the aim of growing your pension savings (significantly!) ready for your retirement.

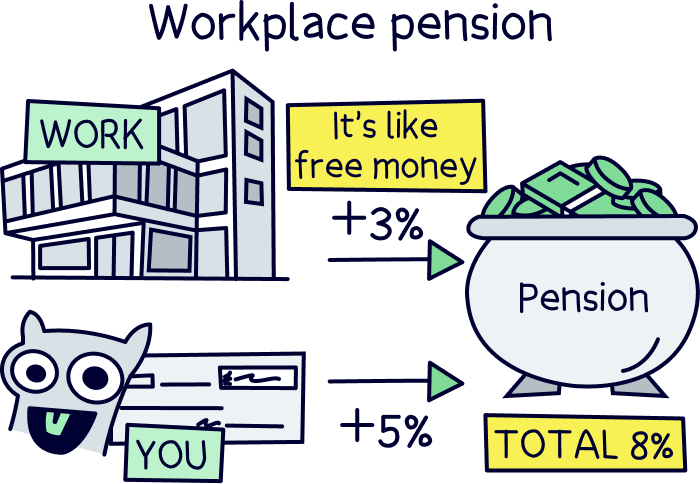

If you're employed, you'll be automatically enrolled into your workplace pension – which is a pension set up by your employer.

What you pay in (your contributions) are taken out of your monthly pay. The standard rate is 5%, and if you do that, your employer has to contribute 3% into your pension too (employer contributions). Winning.

So overall, you'll be putting away at least 8% of your salary into your workplace pension, which you get lovely tax relief on – meaning it's taken before you pay income tax on it (so you don't pay it!). Plus, you won't have to pay National Insurance Contributions on it either.

If you're self-employed, you'll need to manage your own pension. This means you need to decide how much you want to save, and set up the payments yourself. This is called a personal pension and is a type of private pension (which just means it's in your own name). It's super easy to set up and manage, don't panic! Here's our guide to self-employed pensions.

You'll still get pension benefits, such as pension tax relief, but it's slightly different where it's a bonus added to your pension after you pay in, just like a LISA.

You can also have one (or more) personal pensions (also called self-invested personal pensions, or a SIPP), if you're employed as well as your employer pension, and it's often a great idea to do so. We'll get into why later.

If you've heard enough already, here's our best private pension providers – our favourite is PensionBee¹, it's super easy to use and low cost too, here's our review of PensionBee.

Let’s look at the ways Lifetime ISAs and pensions compare. Bear with us, this gets a bit fiddly.

You get a 25% bonus on the money you put into a Lifetime ISA.

You’re allowed to put £4,000 into a LISA each year, which means you can get up to £1,000 for free each year. Tembo¹ can help you set one of these up.

Now with pensions, if you’re a basic-rate taxpayer (earn less than £50,270), you get 20% tax relief on your pension contributions – which actually works out as a 25% bonus on what you pay into your pension – so exactly the same as a Lifetime ISA.

However, if you’re a higher-rate taxpayer (earn more than £50,270), you actually get 40% tax relief from the government, on the money that you’d paid 40% tax on. So a lot more than a Lifetime ISA.

And if you’re employed, your employer has to add a minimum of 3% to your workplace pension too! And nice employers might even add a lot more than this. This is something that doesn’t happen with a Lifetime ISA – your employer doesn’t make any contributions.

So overall, a pension wins on contributions and government bonuses, and by quite a bit.

When you choose your own personal pension, you can make sure your money is going into an ethical pension fund – meaning your pension provider doesn’t invest in things like fossil fuels, weapons, tobacco, or gambling.

With a workplace pension, you’re limited to your employer’s pension provider. You don’t really have a choice, unless your employer gives you different options to choose from.

With a Stocks and Shares Lifetime ISA, you can choose an ethical ISA, or choose investment funds that suit your choices. The choice is all yours!

When we talk about ‘allowances,’ we mean the amount you’re allowed to put into a Lifetime ISA or a pension each tax year.

With a Lifetime ISA, you can put away a maximum of £4,000 each year.

With pensions, you’re allowed to contribute either £60,000, or the equivalent of your whole salary (whichever is lower), into your pension each year. So your allowance is much higher than with a LISA.

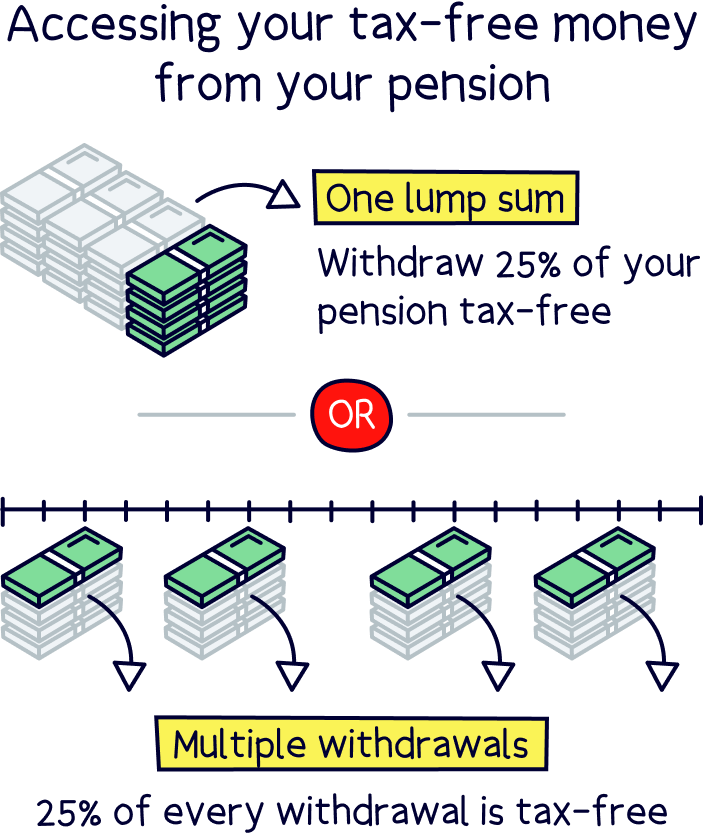

With pensions, you’ll pay tax on your money eventually, when you start taking money out. The first 25% is tax free, but you’ll normally pay tax on the remaining 75%, and it’s the same tax rate as a regular income, such as your salary – but only if your income is above your personal allowance, which is currently £12,570, so you might end up not paying any tax at all in the future, or just a little bit.

Lifetime ISAs are totally tax-free from start to finish. You don’t pay tax on your contributions, you don’t pay tax on interest or investment returns, and you don’t pay tax on withdrawals. With Lifetime ISAs, tax isn’t something you need to worry about.

However, you have already paid tax on the money you’ll pay into your Lifetime ISA, because you’ve paid tax on your income, such as the salary from your job. So although a Lifetime ISA may seem tax-free initially, you have actually already paid it! With a pension you are effectively putting off paying tax until you retire, when you might not have to pay anything anyway!

You can take money out of your Lifetime ISA if you want to buy your first home, or when you reach the age of 60. Anytime before then, or for any other reason, and you’ll face a penalty of 25% – quite a hefty whack!

You can’t access your pension before the age of 55 right now, but that’s due to go up to 57 in 2028. Withdrawing it earlier than this will mean facing charges of 55%. That’s a huge blow. But, you’ll still be able to take your money out of a pension 5 years (or 3 in the future), before taking money out of your Lifetime ISA.

There’s a lot more pension companies offering personal pensions than there are Lifetime ISAs. That means they tend to compete on offering you lower fees, and better options for growing your money. (That’s providing you shop around looking for the best personal pensions). Our private pensions comparison table can help find the best options.

So, which is better? A Lifetime ISA or a pension? Well here we go:

If you’re saving for your first home, a Lifetime ISA is your best option, as you get that lovely 25% bonus, but for saving for your future, and retirement, a pension is the far better option. Why?

In terms of how much your money grows, it’s roughly similar for both, as they’ll be invested in almost the same way.

The Lifetime ISA isn’t designed to be a replacement for a pension. You can have both a Lifetime ISA and a pension – but a Lifetime ISA’s best use is simply for saving for your first home.

The best option for saving a home deposit is a Lifetime ISA. You can save up to £4,000 every tax year and the government will add a 25% bonus at the end of every tax year (that's up to £1,000 free). Tembo¹ specialise in them, it's super easy to get started and their customer service is great.

The best option for long-term saving is to pay as much as you can into your workplace pension, that’s the one you get with your employer, but only up to the limit where they’ll match your contributions – and for most people, thats paying in 5% in order for your company to pay in 3% themselves.

After that, stop paying into your workplace pension, and open your very own personal pension. This gives you much more control over where your money goes – you get to choose which pension provider you want to use, and how your money is actually invested, which could be only in ethical companies for instance.

And by being able to choose which pension provider you go with means you can pick the one with the lowest fees and the best history of growing your money. With workplace pensions, they’re often more expensive and perform worse.

There you have it. Here’s where to learn more about what a personal pension is, and here’s where to find the best personal pension for you. If you want a head start, our recommended provider is PensionBee – here’s our PensionBee review to learn why. Happy saving!

We've done the hard work for you – here’s the best personal pensions to save for your retirement.

We've done the hard work for you – here’s the best personal pensions to save for your retirement.

We've done the hard work for you – here’s the best personal pensions to save for your retirement.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

We've done the hard work for you – here’s the best personal pensions to save for your retirement.