Article contents

Moneyfarm wins overall, although they’re both great! Moneyfarm is much cheaper when it comes to socially responsible investing, and they have experts on hand to guide you if you’re not sure what to do. However, if you're starting with less than £500 Wealthify is for you.

Keen to invest your money? Good idea. Investing can have a huge impact on your life in the future if done wisely, and Moneyfarm and Wealthify are 2 of the best options out there. But which one is better? Let’s find out.

Although they’re often classed as ‘robo advisors’, there’s not actually any robots. This just means technology is used, don't worry, there's expert humans behind the scenes! Actually, an investment app or investment platform is probably a better description, or a digital wealth manager – they have an app and/or a website for you to use to get started and manage your money.

As a quick spoiler, they’re both great investing options, the main difference is that with Moneyfarm, you’ll need £500 to get started, and with Wealthify you can start from just £1. So if you’re just starting out saving, start with Wealthify¹, and if you’re saving more than £500, you can start with either, but we recommend Moneyfarm¹.

It's simple to use, and there's experts to help you along the way.

Moneyfarm and Wealthify have both been built for modern day investing, and are super simple to get started and use. In fact, they both feature in our best investment platforms. A lot of traditional investment companies such as Hargreaves Lansdown have many hoops to jump through to even get started and the investment decisions are all on you.

With Moneyfarm and Wealthify, all you need to do is sign up online, add money, and they’ll take care of the investments for you. Pretty great right?

They’re both available on their websites, and mobile phone apps – on both Android and Apple.

Moneyfarm has an unbelievable rating of 4.7 out of 5 on Apple and 4.4 on Android.

Wealthify is rated a very high 4.5 out of 5 on Apple. There's no Android rating.

Both apps and websites are super easy to use, you can check your total balance (how much you have invested), your performance so far (how much your money has hopefully grown), and where your money is invested.

It's also easy to add and remove money, plus you can set up regular payments (your money has a lot better chance of growing large over time if you do this).

However, there’s one key difference between the two. With Moneyfarm, there’s also experts on hand to guide you through the investment process and which options are best for you. They can also help with anything you might want to chat about along the way too. They’re fully qualified, and you can get an appointment to suit your schedule. It’s a good service that not many investment apps offer.

And for that reason, we’re giving this round to Moneyfarm. They've made the whole process very simple, but on top of that you’ve also got experts on hand to help you.

Winner: Moneyfarm

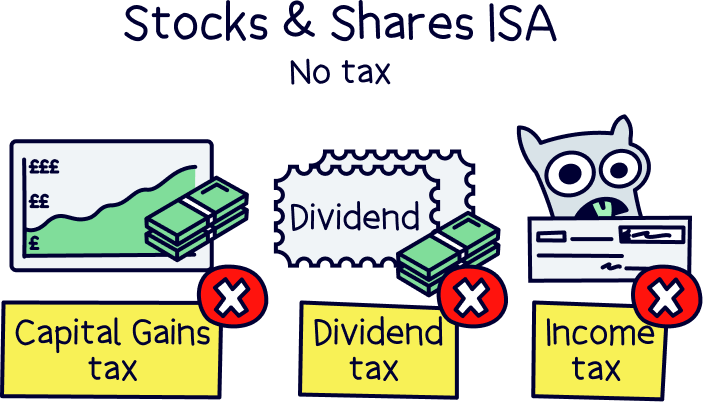

In the UK, saving for the long-term has some amazing tax-free benefits if you use a pension and a Stocks & Shares ISA. You can grow your money much faster with both, as you won’t pay any tax as the money grows. (Without these tax-free accounts, you might have to pay tax when you sell your investments, and it can be a lot in the future!)

With a Stocks & Shares ISA (Individual Savings Account), you can save up to £20,000 every year tax (April 6th to April 5th the following year), and everything you make is tax-free, forever!

Note: you can only pay into one Stocks & Shares ISA per tax year.

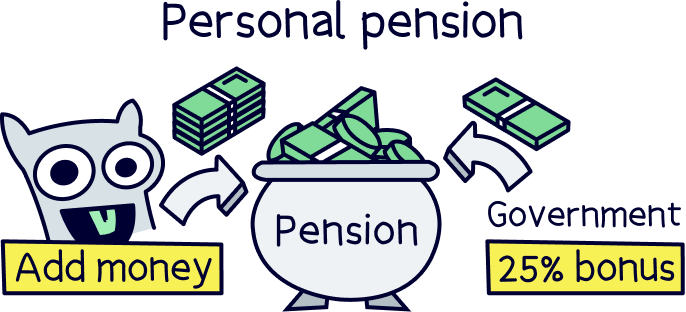

With a pension (technically called a personal pension), your money grows tax-free too. As you’ve already paid tax through your salary, this money is refunded to you. This works by giving you the tax back as a 25% bonus, which goes straight into your pension, every time you contribute. It's kind of like free money, how good is that?!

However, you might have to pay tax later down the line when you withdraw your cash, it all depends on how much you earn at the time – but 25% of it is always tax-free.

It’s a little complicated, but overall pensions are a great way to save for your future. Here’s where to learn more about tax on pensions.

By the way, if you’re only looking to save within a pension, check out PensionBee¹, they’re easy to use, low cost and have a great track record of investing. Here’s our 5 star PensionBee review to find out more.

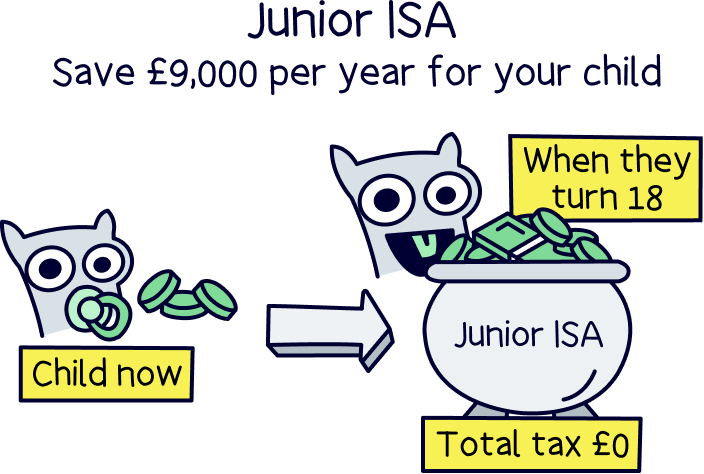

You can also save for your children's futures with a Junior ISA – where you can save up to £9,000 per year completely tax-free, all in their name.

Finally, you can also invest within a General Investment Account (GIA), however there are no tax-free benefits.

With both Moneyfarm and Wealthify, you have all of these options, which is:

As they’ve both got all of them, this one’s a draw.

Winner: it’s a draw!

Once you’ve decided which account you want to save in, you’ve then got the main event, which investment option you want. An investment option is how you’d like your money to be invested, and each platform offers a small range to suit different people. With both, again, it’s super easy.

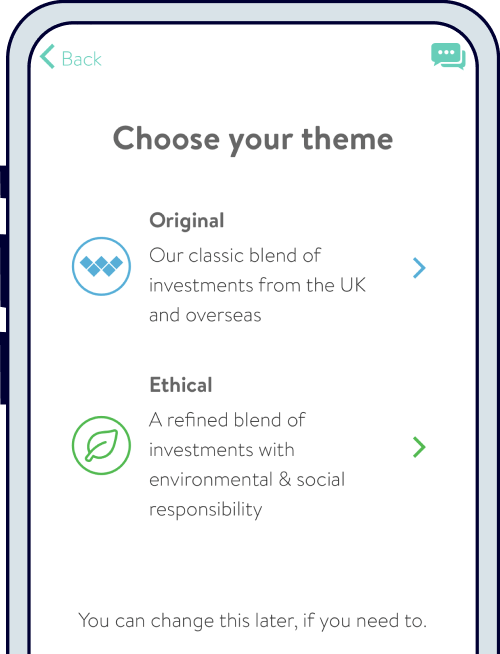

With Moneyfarm, there’s 3 simple options:

And with Wealthify, you’ve got 2 options:

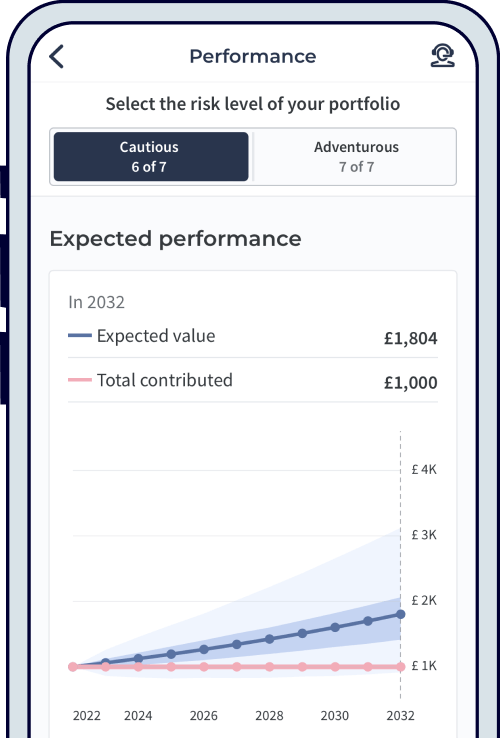

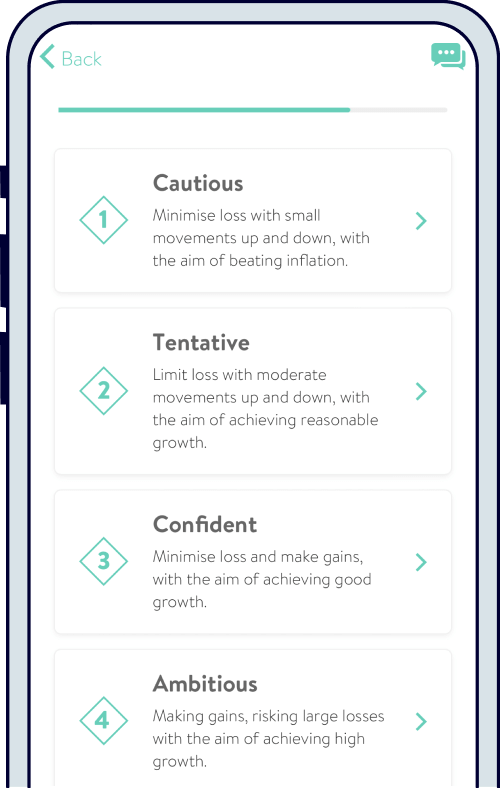

Super simple right? Next, for both Moneyfarm and Wealthify, you’ll then pick which risk level you’re happy with (don’t let the word risk put you off). You’ll pick from low to high, and a higher risk level means there’s potential for your money to grow much more, but there is likely to be bigger ups and downs along the way (called volatility). With lower risk, the aim is slow and steady growth.

Moneyfarm has 7 different risk levels.

And with Wealthify there’s 5 risk levels. So there’s a bit more flexibility with Moneyfarm.

And when it comes to the socially responsible investment option, both are great, but Moneyfarm’s is just that little bit more special…

Why? The investments are based on stricter criteria, meeting 100% of the United Nations Global Compact initiative (which covers things like climate and working conditions), and 100% compliant with labour laws across the world (such as no child labour).

Here’s where to learn more about Moneyfarm’s socially responsible portfolios¹.

Whereas Wealthify’s investments are less strict and only cover ESG practices (environmental, social and governance). Which is still great by the way!

We're big fans of socially responsible investing here at Nuts About Money, and Moneyfarm goes above and beyond, making them the clear winners here.

Winner: Moneyfarm

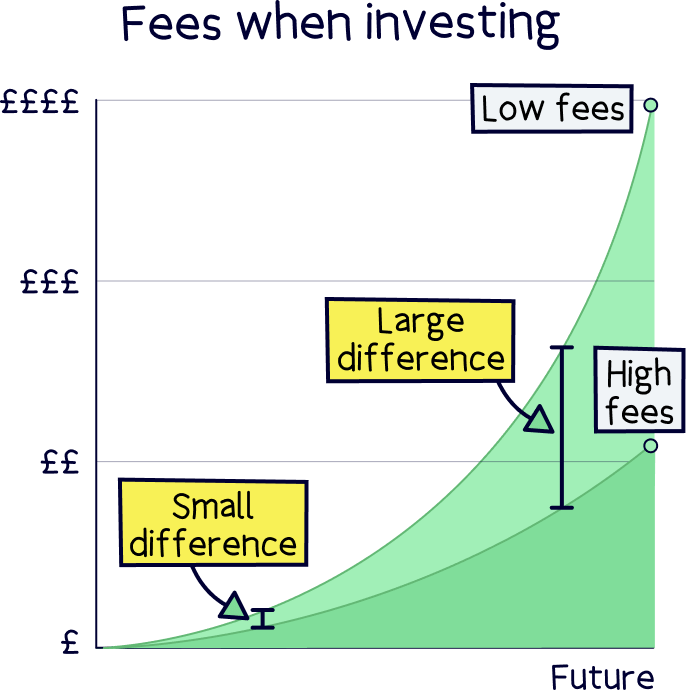

When it comes to long-term investing, fees are important, they can eat away at your profits over time and what seems small now, can have a big impact on your total balance in the future!

However, we don’t recommend making decisions based on fees alone, as long as you’re getting value for money, and your money is growing well, then it’s often worth it. Especially, if experts are handling the investing for you.

The fee structure is the same with both Moneyfarm and Wealthify (and most investment platforms). You’ll pay an annual management fee based on the total amount you have invested. Alongside that the investments themselves will have a fee and there can be fees when investments are bought and sold too.

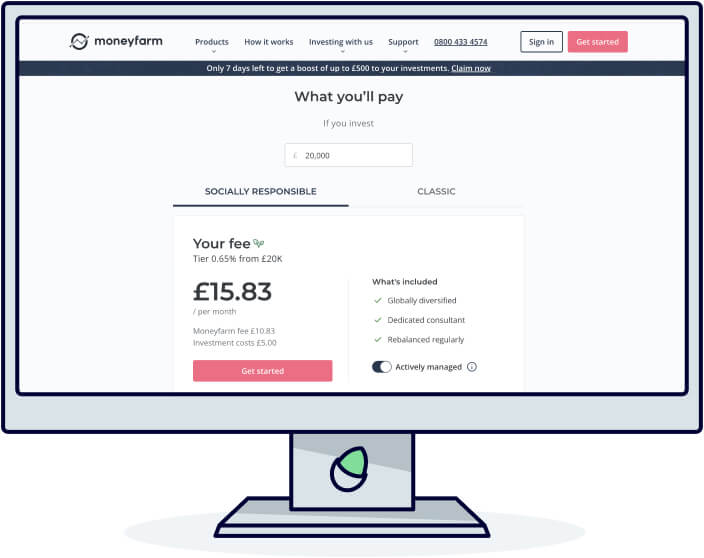

Overall, Moneyfarm is much cheaper for socially responsible investing, and both are very similar with their regular plans that don't have ethical investments. Moneyfarm’s fixed allocation option is also lower cost.

In general, compared with other investment platforms they’re great value. Another popular provider is Nutmeg, which is more expensive. You can learn more about Nutmeg with our comparison of Moneyfarm vs Nutmeg. And if investing with a financial advisor, expect to pay a lot more, around 2% per year.

Bear in mind, these are platforms with experts managing your investments. You might find cheaper platforms where you are managing the investments yourself, such as InvestEngine¹.

Let’s run through the fees for each.

Here’s what you’ll pay as a percentage of the money you have saved. The fee applies to how much you have in total.

Fully managed and ethical:

Fixed allocation (less hands-on from the experts):

You’ll then pay investment fees which average 0.20% and fees to buy and sell up to 0.09%.

This comes to a total of a maximum of 1.04% and reduces as you save (maximum of 0.74% with the fixed allocation).

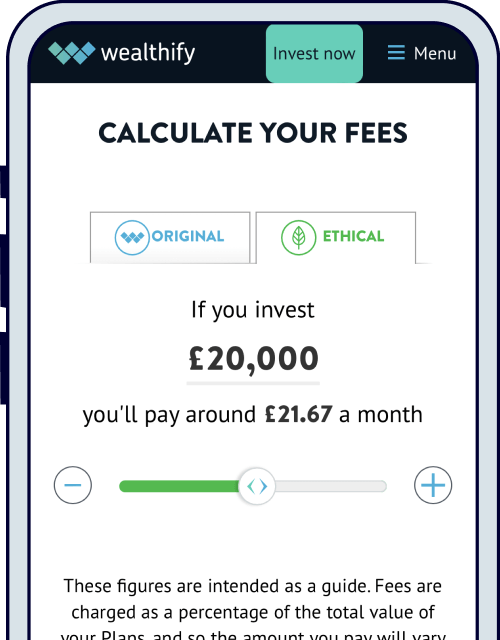

With Wealthify, you’ll pay a flat fee of 0.60% per year.

However, here’s where it gets a bit more complicated. With the original investment plan, you’ll pay investment fees in the region of 0.16%. Which gives a total of 0.76% in total.

With the ethical plan, you’ll pay fairly hefty investment fees of 0.70%, giving you a total of 1.30% per year. That’s a lot in comparison.

Overall, if you have less than £50,000, it’s a bit cheaper with Wealthify, anything above that and Moneyfarm starts becoming a lot cheaper.

That’s unless you opt for the cheaper fixed allocation option with Moneyfarm, which would be cheaper regardless of the amount saved.

With ethical investing, Moneyfarm wins hands down, it’s much cheaper.

Again, as we're big fans of ethical investing here at Nuts About Money, and as the difference between Moneyfarm fees vs the original investment plan with Wealthify isn’t that big, and Moneyfarm is cheaper with more saved, we’re giving this round to Moneyfarm.

Plus, it’s one of the cheapest expert-managed options out there.

Winner: Moneyfarm

To get a good idea of customer service and the overall customer satisfaction, let’s look at the customer reviews. And to do this, let’s use the popular reviews website, Trustpilot.

With Moneyfarm, it’s got an excellent rating of 4.4 out of 5, from over 750 reviews. That’s pretty amazing. Lot’s of the reviews mention the ease of use, good investment performance and the great customer service overall, especially from the experts.

With Wealthify, it’s also got an excellent rating of 4.3 out of 5, from over 1,700 reviews. Again, amazing. Lots of the reviews mention how easy and simple it is. However there’s a few negative reviews highlighting the poor investment performance.

Although it’s very close, Moneyfarm just pip them to the post.

Winner: Moneyfarm

Wealtify is great for many reasons, but Moneyfarm has lifted the bar to a new level and is the overall winner!

They’re both super easy to get started and use, and both have great apps and websites to track and manage your investments. The key difference is Moneyfarm has experts on hand to help you determine the right investment strategy for you, and to help you with any questions you might have.

The account options are exactly the same, with the key accounts being a Stocks & Shares ISA, and a personal pension (both great options to save for your future).

And when it comes to investment options, they're fairly similar, both with a standard option where the experts manage everything, and a socially responsible option. Moneyfarm also has a lower cost option too (with less expert involvement).

With the fees, there's one main difference, and that’s the socially responsible option is much more expensive with Wealthify unfortunately. It’s almost double the cost of the original option (1.3% vs 0.7%). That’s also a lot when compared to Moneyfarm’s socially responsible option, with management fees starting at 0.75% and reducing as you save more.

And finally, with customer reviews, Moneyfarm just nicks it. Although customers are big fans of both.

So, overall, there’s not much difference, and you can’t go wrong with either, but we’re calling Moneyfarm the winner here. It’s slightly better overall.

There’s also one big thing to mention, with Moneyfarm, you have to invest at least £500 to get started. So if you’re just starting out, and have less than this, start with Wealthify and see how you get on. You can always swap when you have enough money saved.

If you like the sound of Moneyfarm, get started on the Moneyfarm website¹, and here’s where to get started with Wealthify¹.

And if you’re just looking to start a pension, check out PensionBee¹ too – there’s no minimum deposit, and it’s super easy to use, with a great track record of investing. Plus, they have an incredible 5 out of 5 on the Google Play Store, it's the only one we've ever come across and we've reviewed 100s of apps!

It's simple to use, and there's experts to help you along the way.

It's simple to use, and there's experts to help you along the way.

It's simple to use, and there's experts to help you along the way.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

It's simple to use, and there's experts to help you along the way.