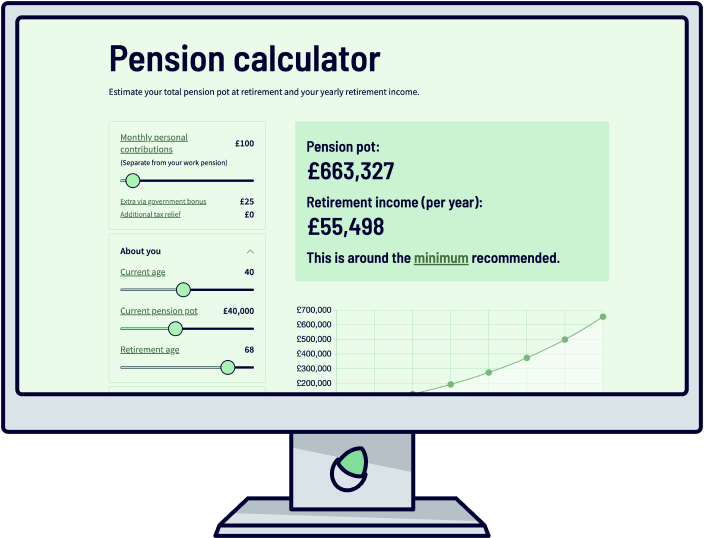

Find out how much your Stocks and Shares ISA could be worth in the future.

Yearly contributions

£2,400

(the average is roughly 5%)

Our Nuts About Money Stocks and Shares ISA calculator is here to help you plan your investment savings for the future – it shows how much your total savings could be worth, depending on how much you want to save (per month), and your estimated investment return (average percentage increase over the years).

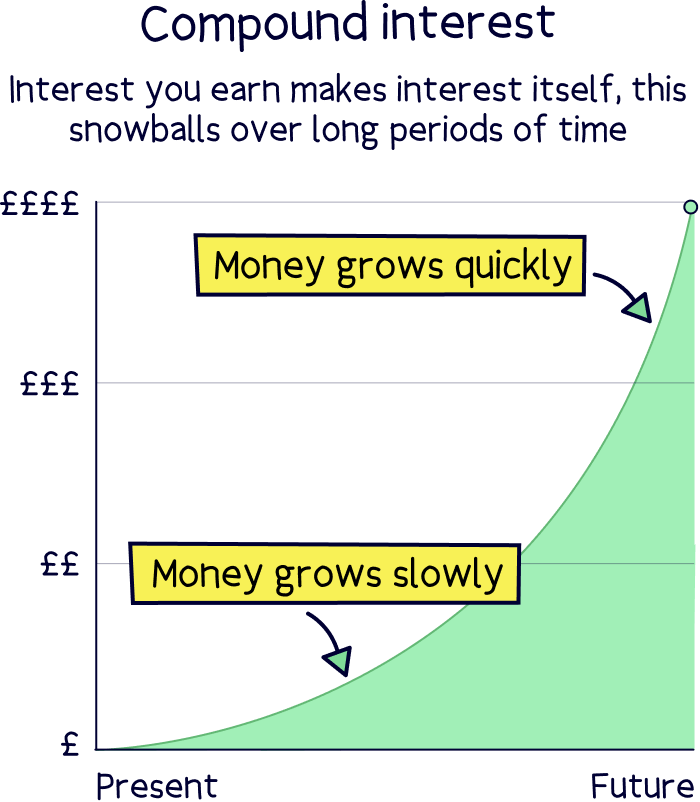

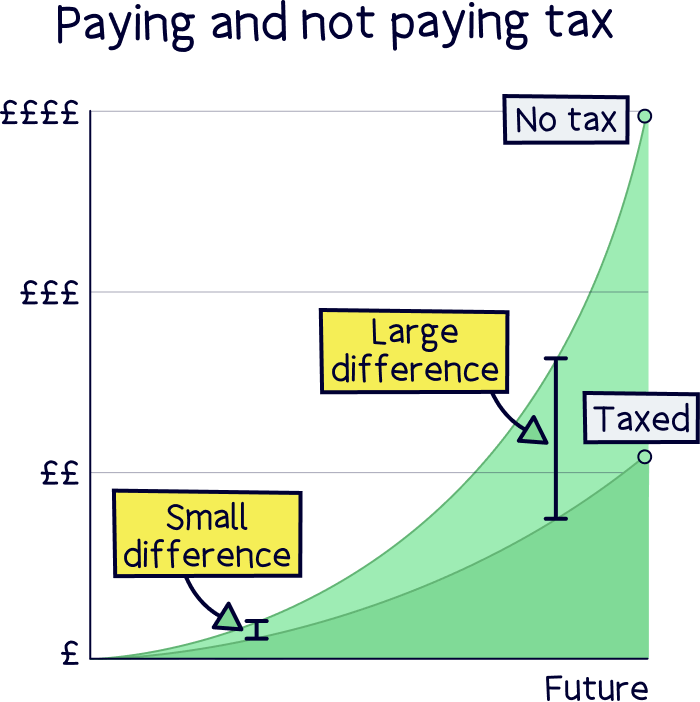

As part of our calculations we’ve included compounding (compound interest). This works annually, and means the money you make from your investments, essentially begins to make money itself too – and this snowballs over and over, and over the years turns very small amounts into huge amounts. Einstein actually called this the 8th wonder of the world.

You can save up to £20,000 per year into a Stocks and Shares ISA (well, a total across all your ISAs), so we’ve set the annual limit to £20,000, which is £1,667 per month.

Our Stocks and Shares ISA calculator allows you to save for up to 40 years – eventually you’d probably want to spend the money, but if you want to save for longer, maybe for retirement, check out our pension calculator.

And as Stocks and Shares ISAs are tax-free, we haven’t included any tax payments in the calculations (all of the above is explained below).

This is how much you’ve got in your Stocks and Shares ISA account already.

This is how much you are intending to save per month into your Stocks and Shares ISA.

The most you can save into an ISA is £20,000 per year, so you’re able to save £1,667 per month.

Nuts About Money tip: if you’re planning to save more, and thinking about retirement, a pension can be a great idea, use our pension calculator to learn more and plan ahead. You can also invest more into a regular investing account, where you’ll pay tax on your profit.

This is how long you intend to keep your savings for – and you can save up to 40 years with our Stocks and Shares ISA calculator. If you’re intending to save for longer, such as for retirement, you might want to consider a personal pension (they’ve got great tax-free savings benefits too).

This is how much you’ll expect your money to grow each year (as an average).

As a guide, 5% per year is seen as a middle of the range forecast, 8% on the higher end and 3% on the low end (these are guidelines set by the Financial Conduct Authority (FCA), who are the people who look after financial companies).

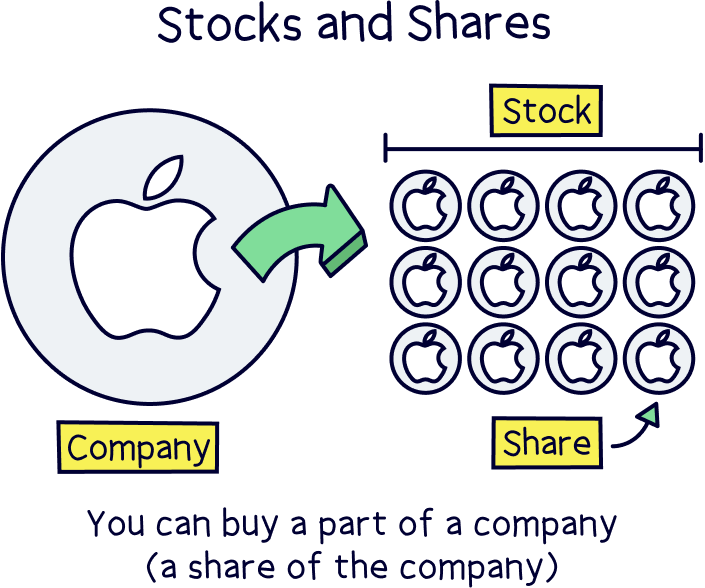

A Stocks and Shares ISA is where your money is invested in, you guessed it, stocks and shares, with the aim of growing your money over time. And it’s all tax-free.

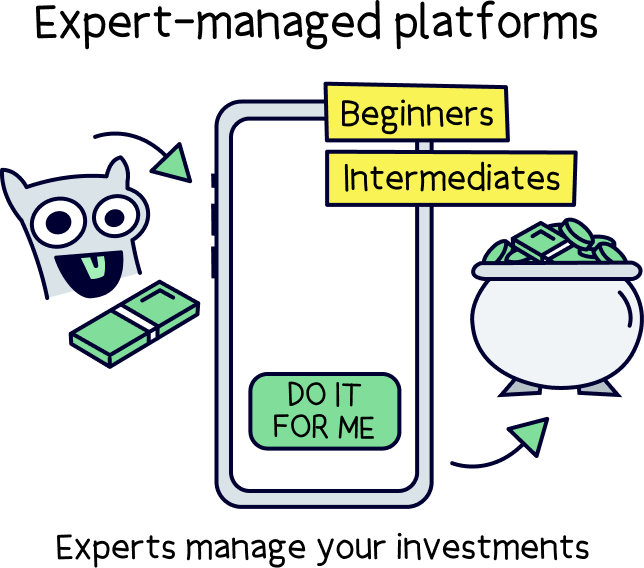

If done right, they’re not as complicated or risky as they might seem, and can significantly increase your savings over time, potentially much more than interest from a cash savings account – and you can simply let the experts handle the investments (meaning you don't need to know much about investing).

Shares represent part ownership of a company (you own a share of a company), and they have a value (e.g. £100), and when a company does well and grows, this value can increase (e.g. to £150), and therefore your investment increases.

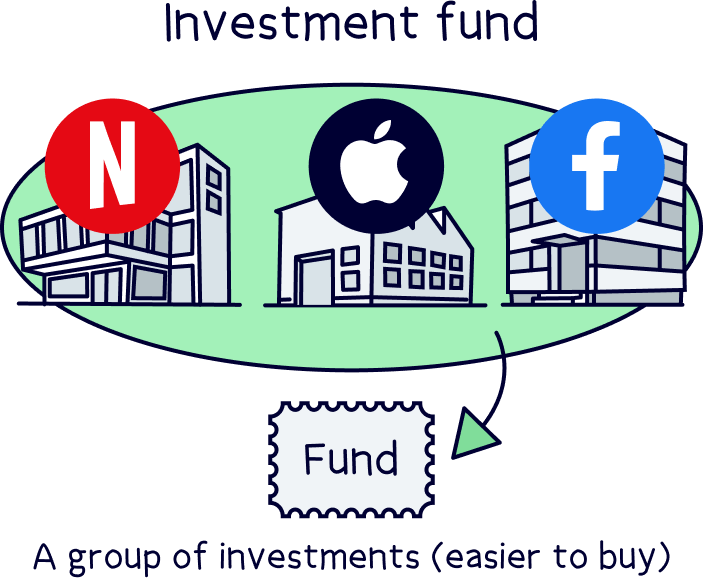

Most investment strategies would include owning thousands of different shares (companies), often by being invested in what’s called a fund, which is a large group of shares or similar kind of investments to shares (like loans to governments called bonds).

This reduces a lot of the risk of your money falling in value significantly, and helps your money grow over time. Depending on how much it grows will usually depend on the level of risk you’re happy with, and the type of investment you’d like.

Your money will always go up and down day-to-day, but over time (e.g. over 5 years or more), and with the right investment strategy, it would typically grow fairly significantly (although there’s never any guarantees).

You can simply leave the experts to manage the investment side of things with a managed Stocks and Shares ISA (recommended), and leave your money to grow over time.

Or, if you’re more confident with investing, you can manage your own investments within a self-managed ISA.

Nuts About Money tip: for all the top options for Stocks and Shares ISA, head over to our best investment platforms table.

If you’re saving for your first home, you could consider a Lifetime ISA instead of, or alongside a Stocks and Shares ISA.

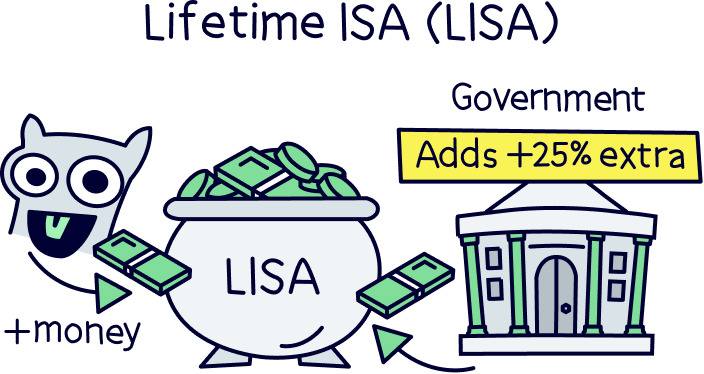

A Lifetime ISA, or LISA, is a government scheme to help you save your first home, although they can also be used for later in life if you don’t want to use it for your first home (after 60 years old).

With a LISA, you can save up to £4,000 per tax year (April 6th to April 5th the following year), and you'll benefit from a massive 25% bonus from the government on everything you save into it, so up to £1,000 free each year.

Your money will grow tax-free, so there’s no tax to worry about either, so it can grow much more over time.

You can use the money towards your first home, as long as you’re a first time buyer (so haven’t bought a home before), and the property has to be under £450,000. You also have to live in it (so not a buy to let).

However, there are some rules to open one, you need to be at least 18 years old, and be under 40. You can also only save into one until you’re 50.

And if you don’t end up using your LISA for your home, if you want to withdraw your money from your account, you’ll face a hefty 25% fee, which works out as more than the 25% bonus (it sounds odd, but the maths works out). Or, you can wait until you’re 60 years old, when there’s no penalty fee.

Nuts About Money tip: check out our Lifetime ISA calculator to plan your LISA savings.

If you’re saving for retirement, you also might not want to use a Stocks and Shares ISA…

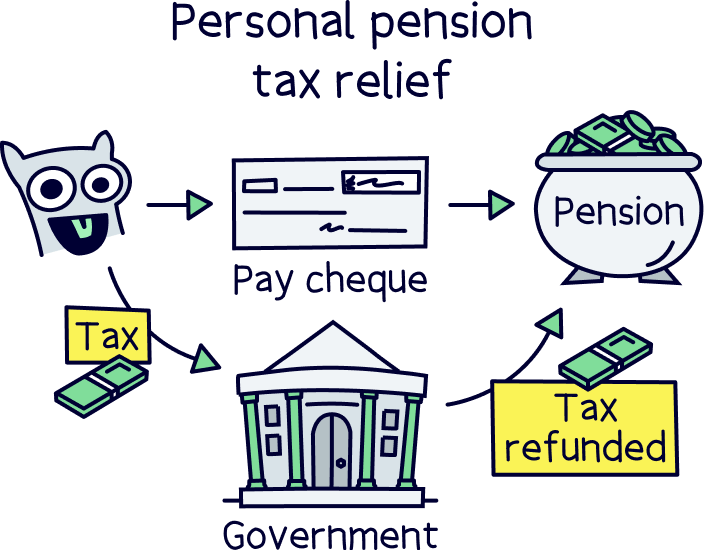

You also have the option of a pension, which you’ll likely be familiar with if you have a job, but you can also save into your own pension, called a personal pension, alongside your pension from work.

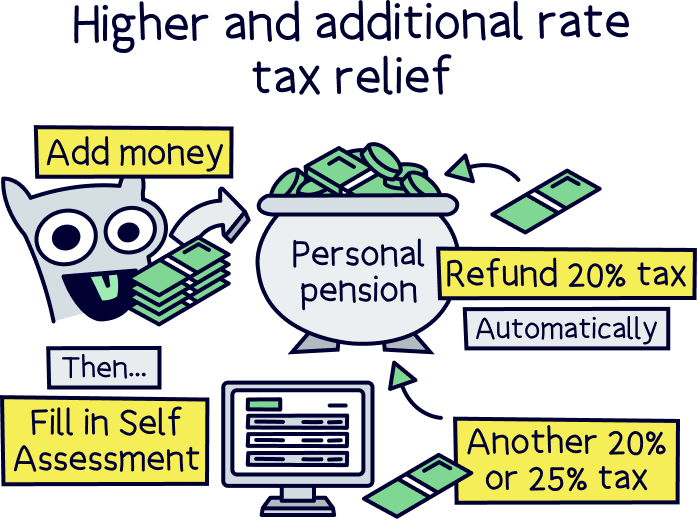

With these, you’ll automatically get a 25% government bonus on everything you save into one, which is to refund tax you’ve paid on your income (at 20% tax rate), called tax relief.

And if you earn over £50,270, meaning you pay 40% or 45% tax on some of your income, you’ll also get this tax back too (which you do by claiming on a Self Assessment tax return).

Your money grows tax-free too, and when it comes time to retire and withdrawing from it, you can withdraw 25% completely tax free (as long as the 25% is under £268,275).

You can save up to £60,000 per year, or up to your total income each year (e.g. your salary), whichever is lower, as a total across all your pensions.

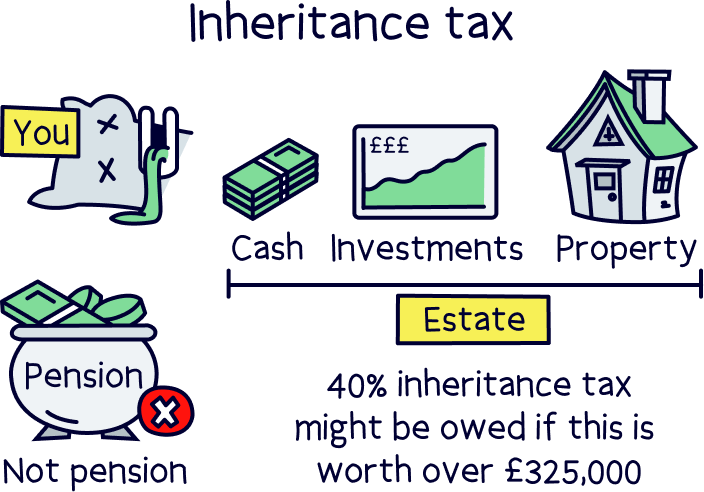

And, they don’t count towards any Inheritance Tax that might be paid when you sadly pass away.

Anyway, we won’t go into all the details right now, but you can learn more with our guide personal pensions, or if you’re keen to get started, here’s our guide to the best private pensions. Oh, and try our pension calculator too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

interactive investor is a low cost (flat monthly fee), investment platform with excellent customer service.