Article contents

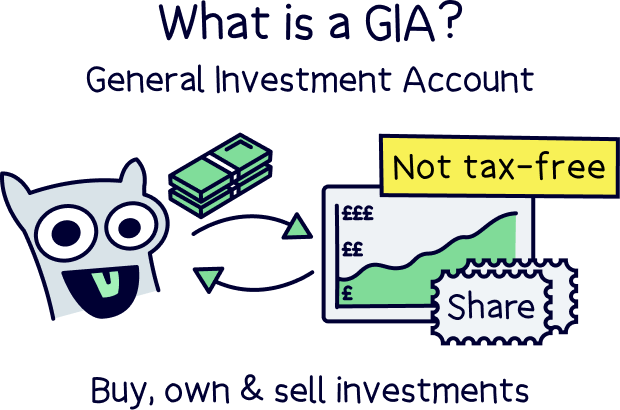

A General Investment Account (GIA) lets you buy, own, and sell investments without tax-free advantages like those of ISAs or pensions. While ISAs and pensions have contribution limits, a GIA allows unlimited contributions. Various GIA options are available to suit different investment goals.

Keen to get investing but not sure which investing account to use? Or maybe an investing pro, but not familiar with a General Investment Account?

You’re in the right place.

Let’s go through your options and everything you need to know about a General Investment Account, also known as a GIA.

A General Investment Account, often also called a ‘share dealing account’, is your bog-standard account for investing, such as buying stocks and shares.

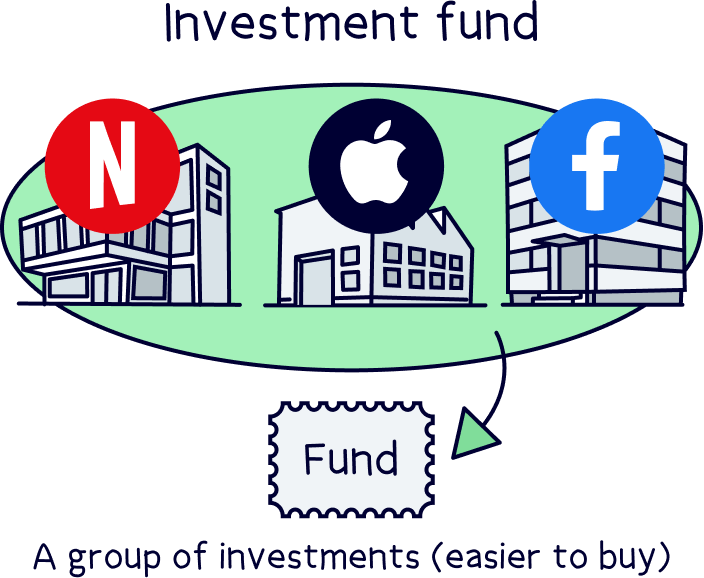

You can buy much more than just shares however, such as investment funds, or index funds – which are groups of shares and sometimes other investments like property, all grouped together into one single investment.

The types of investments can vary significantly, it just depends on which investment platform you choose, as most only have a certain amount of investments to choose from. (An investment platform is a place to buy and sell investments, often a website or mobile app).

When we say your bog-standard account, we mean there’s no fancy benefits such as tax-free saving, or juicy government bonuses added to your savings (yep, you can get cash from the government with a personal pension and Lifetime ISA!).

You might have to pay tax on what you make within a GIA, depending on how much you make (see below).

By the way, if you haven’t contributed to a Stocks & Shares ISA this tax year yet (April 6th to April 5th the following year), it’s worth considering using this first (as you wont pay any tax on your profits). Check out our guide to Stocks and Shares ISAs to learn more.

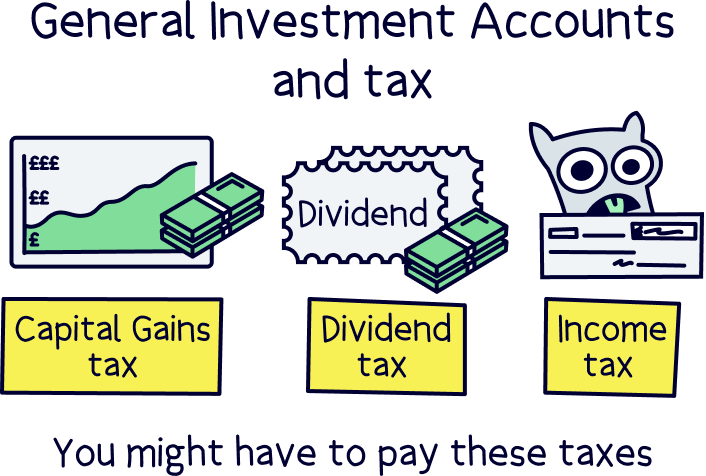

Unfortunately, there’s a few different types of tax you could pay when you invest within a General Investment Account.

There’s Capital Gains Tax, Dividend Tax and potentially Income Tax if you earn any interest from your investments.

Let’s run through them all.

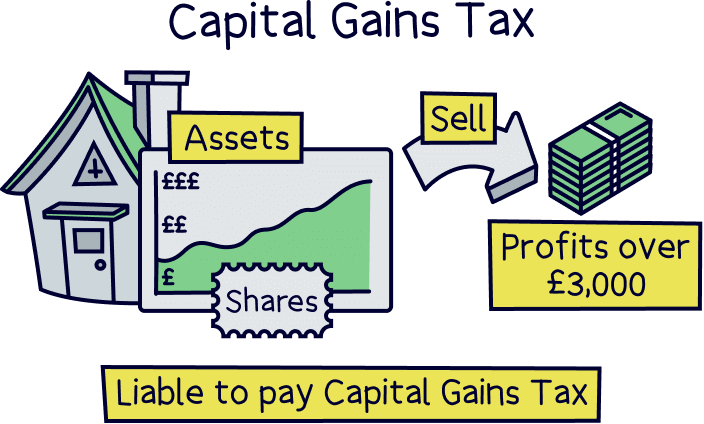

Capital Gains Tax is what you’ll pay when your money makes more money, or in most cases, when you buy an asset (like a share) and it increases in value – which means you have gained more capital (a fancy word for money).

You’ll pay Capital Gains Tax whenever your profits within a tax year (April 6th to April 5th the following year) are over £3,000. And you’ll pay 20% or 24% depending on how much you earn, and that’s on anything above £3,000 (to clarify, you won't pay any tax on the first £3,000 you make each tax year).

Bear in mind, this is only when you sell your investments, so if you’re investing for the long-term you may not have to worry about this for many years.

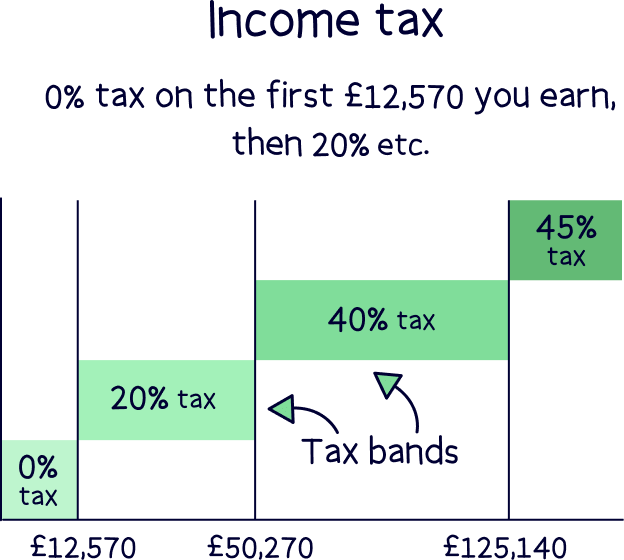

You’re probably more familiar with Income Tax – this is what you pay on your earnings, such as your salary (you will be able to see it in your payslip if you get one). It works by using ‘tax bands’ which are different categories of how much tax you pay vs how much you earn in a tax year.

Here’s what you’ll pay:

This means that the first £12,570 you earn is completely tax-free, get in! After that you’ll pay 20% tax from £12,571 up to £50,270, and then 40% on anything above that up to £125,140, and then 45% on everything above £125,140.

And if you’re in Scotland, this is what you’d pay:

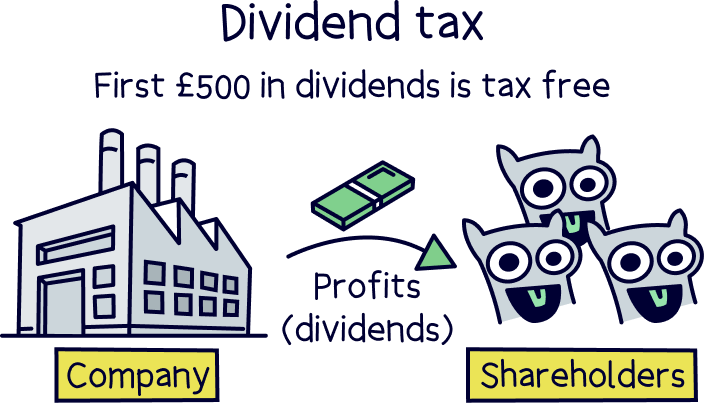

If a company pays out their profits to the owners of the company (people who own shares, called shareholders), this is called a dividend. The first £500 you receive in dividends is tax free, called your dividend allowance, but after that, you’ll have to pay tax on them.

It gets a bit complicated now, as how much tax you pay on dividends depends on how much you pay in income tax (which is a tax on your earnings).

So, depending on which tax band you’re in (we’ve gone over these just above), then below is the tax you’ll pay on all of your dividends after the first £500.

If you’re close to the next band of income tax, and your dividends push you over, then you’ll pay the higher rate of dividends tax on the amount above the band.

You’ll pay Dividend Tax on your Self-Assessment Tax Return.

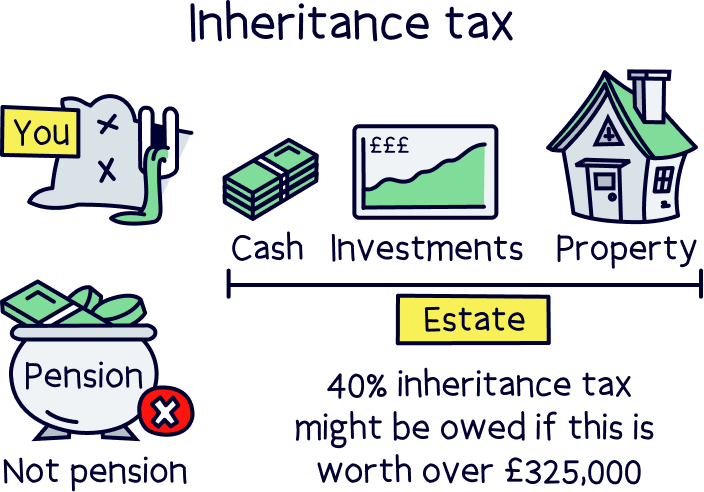

There’s also Inheritance Tax to consider too. All of your assets within your GIA will contribute towards your total estate when you pass away. Your estate is the total of all your assets, so, all of your investments and money, even in ISAs, and any property you own too.

However, no tax is paid unless your total estate is worth more than £325,000.

The only thing not included is your pension(s) – and these are quite special, they won’t be included within the total of your estate, so excluded for Inheritance Tax purposes, and they can be passed on to whoever you like. Plus, it will be tax free if you unfortunately die before you reach 75 years old (so whoever you pass them on to, won’t pay income tax).

All of this is super important if you want to leave your loved ones with as much money as possible. Learn more about Inheritance Tax and ISAs and what happens to your pension when you die.

The first thing to mention here is that you don’t need to pick between a GIA or ISA. They cater for different investing and savings goals. And typically, you’d pick an ISA first. But let’s run through what an ISA actually is and the different types available to you.

By the way, sometimes you might hear the word ‘ISA wrapper’, this just means you are using an ISA account for your savings.

A Stocks and Shares ISA is the main ISA for investing. You can pay in up to £20,000 per tax year (this is called your annual ISA allowance), and everything you make within the account is completely tax-free, forever! Not bad right?!

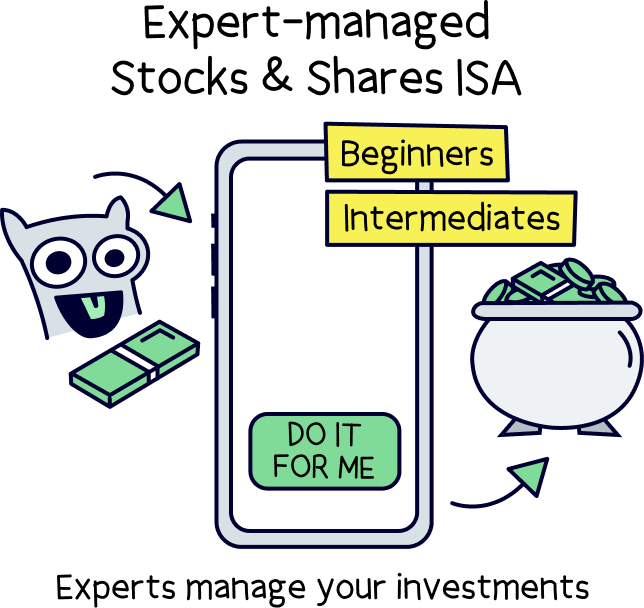

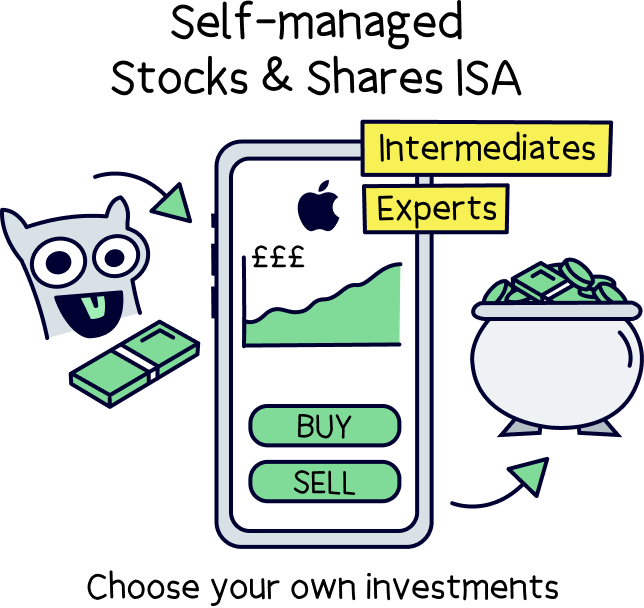

They come in 2 main forms, an expert-managed ISA or a self-managed ISA.

With an expert-managed ISA, you simply add your money, and their investing experts will take care of everything and aim to grow your money safely over time.

With a self-managed ISA, it’s all up to you, you decide which investments you want, and you’ll buy and sell investments yourself.

We’ve rated the best of both types with our best investment platforms guide and the best Stocks and Shares ISAs.

Learn more about a General Investment Account vs ISA.

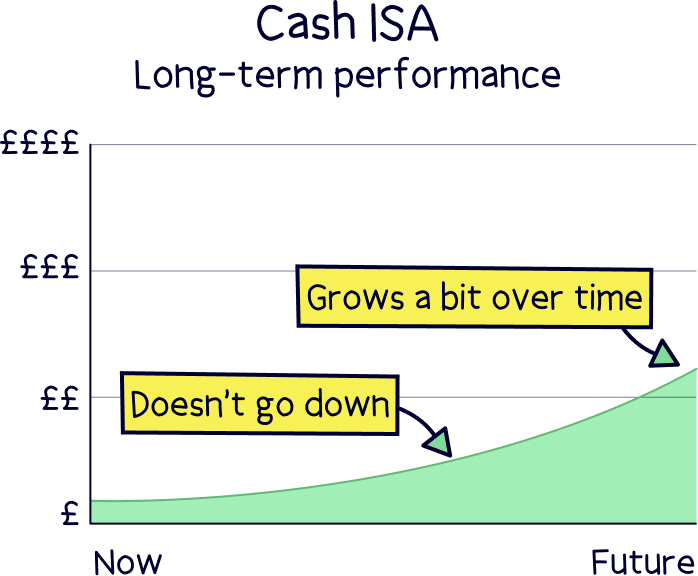

With a Cash ISA, you can save up to £20,000 too (your ISA allowance allows you to save up to £20,000 in total across all of your ISAs, not each). A Cash ISA is similar to a savings account with a bank, you’ll earn a fixed interest on your money (for example 3%), and all the interest you earn is tax-free.

If your savings were not within an ISA, you may have to start paying Income Tax.

As a basic rate taxpayer, you’ll pay Income Tax on interest earned above £1,000 per year. For higher rate taxpayers, you’ll pay it on interest earned above £500, and additional rate taxpayers will pay Income Tax on all interest earned.

This is called your Personal Savings Allowance. Let’s make that a bit clearer:

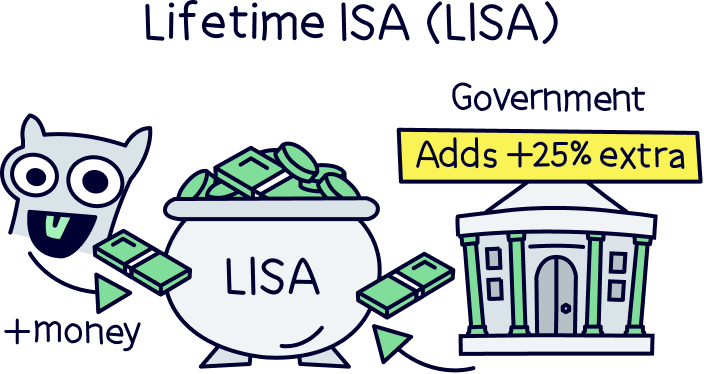

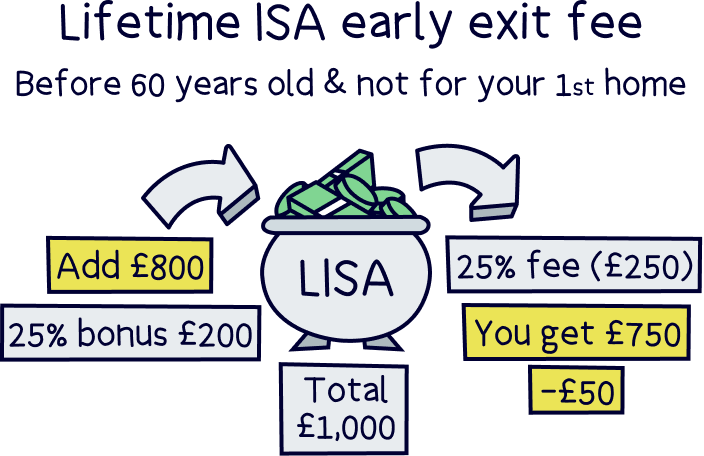

A Lifetime ISA is great if you’re saving to buy your first home. You’ll be able to save up to £4,000 per year (which is part of your £20,000 ISA allowance), and the government will add 25% of whatever you contribute yourself. So if you put the full amount in every tax year, you could make an extra £1,000 per year!

However, if you don’t use it to buy your first home, you’ll have to wait until you’re 60 before you can access the cash. If you want it before then, you’ll have to pay a very hefty 25% fee, which actually works out to more than the 25% free cash you get from the government.

So where does a General Investment Account fit in? Well, the best strategy is to use it in addition to your ISAs – because it makes sense to get as much tax-free benefits as possible first!

For example, you might hold most of your savings in an expertly managed Stocks & Shares ISA. However, if you’re planning to contribute the full £20,000 ISA limit during the tax year and want to invest in some individual stocks on the side, you’d need to use a General Investment Account (GIA). You’ll need to open a GIA on an investment platform, or maybe a stock trading platform.

And the same goes for a Cash ISA, maybe you want to use your ISA limit to save cash, but want to have investments too. So, you can open a General Investment Account for your investments.

There’s lots of options really. It’s all down to your personal circumstances and how you like to save and invest.

As we mentioned, pensions are great for long-term saving, but how do they compare to a GIA?

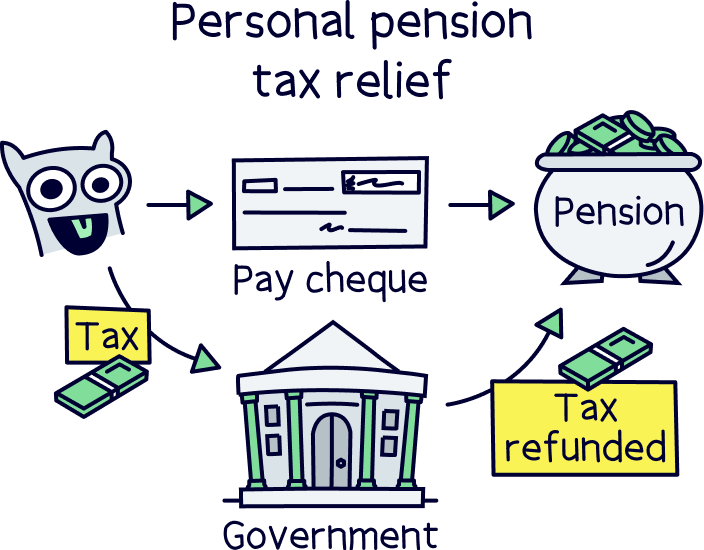

Why are pensions great for saving and investing? Well, everything you make within a pension is tax-free (however, you may end up having to pay Income Tax when you take the money out).

And if you add money to your pension after you’ve been paid (for instance after your salary), you can also get a 25% bonus from the government for everything you put in.

Why does the government do this? It's effectively the tax you’ve paid on your income being refunded back into your pension to make it tax free.

And if you’re a higher rate or additional rate tax-payer, you can claim back the amount of tax you’ve paid at that rate too. So you could even get a 40% or even 45% bonus. We told you they were good!

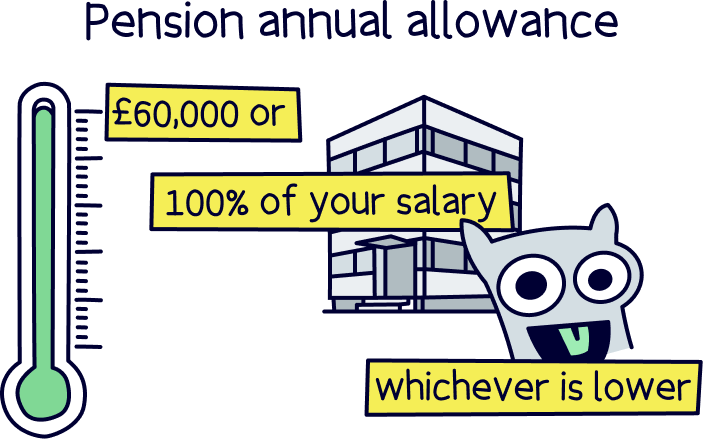

Note: you can save up to your whole earnings per year, or £60,000, whichever is lower. Across all of your pensions, which includes your workplace pension if you have one (the one your employer sets up for you).

However, you can’t access your pension until at least 55 (57 from 2028), so make sure you are saving for the long-term before putting your hard earned money in.

This is where a General Investment Account can be useful. If you are saving for the short-term, or making lots of short-term investments, a GIA makes it much easier to access your money when you need it – you’ll normally have it back within a few days!

There are lots of great options out there for personal pensions. Check out our best private pensions (UK) to learn more and find the best one for you.

Learned enough and ready to get yourself a GIA? Here’s the best General Investment Accounts that are managed by experts, and General Investment Accounts managed by yourself.

We’ve reviewed the best investment platforms so you can find the best for you.

Great app

A great and easy to use investing app. Add money from your bank or transfer your existing ISA, with the investments handled by experts. There’s a pension pot too.

The customer service is excellent, with support based in the UK.

Beach is an easy to use investing app (and easy to set up), just add money and the experts handle everything. It’s all managed on your phone with a great app, and you can see your total savings whenever you like.

You’ll get an easy access pot (access money in around a week), which can be an ISA where all the money you make is tax-free (save up to £20,000 per tax year), and a standard account for those saving in addition to this (or who don’t want an ISA), where there’s no contribution limits (but also no tax-free benefits).

The investments are managed by experts from the largest investment company in the world (BlackRock). And they consider things like reducing climate change, meaning your savings could make the world a little better in future too.

There’s also an optional pension pot to save for retirement, so you can keep all your savings in one place, and if you’ve got lost or old pensions, Beach can also find them and move them over too.

Fees: a simple annual fee of up to 0.73% (minimum £3.99 per month).

Minimum deposit: £25

Customer service: excellent

Pros:

Cons:

Moneyfarm is a great option for saving and investing (both ISAs and pensions). It's easy to use and their experts can help you with any questions or guidance you need.

They have one of the top performing investment records, and great socially responsible investing options too. Plus, you can save cash and get a high interest rate.

The fees are low, and reduce as you save more. Plus, the customer service is outstanding.

Pros

Cons

We’ve reviewed the best investment platforms so you can find the best for you.

We’ve reviewed the best investment platforms so you can find the best for you.

Get up to £100 free share

Lightyear is an awesome mobile app with very low cost investing.

There’s a decent range of investment options (over 4,000 stocks and ETFs), you can store multiple currencies, and the app itself is modern and super slick.

There's no account fees and no trading fees. There's also very low currency conversion fees of 0.35%, or you can hold the currency itself, and avoid this fee.

You can invest with a tax-free ISA, a regular account and a business account.

And if you’ve got cash savings, you’ll also get one of the best rates possible with their Cash ISA (it matches the Bank of England base rate).

eToro is one of the best investment platforms out there - and is by far the most popular, with over 30 million customers.

Why? eToro is very low cost (commission-free stocks), easy to use, and has lots of awesome trading features. There's also a community of other traders to learn from and even copy.

It’s also got the largest range of assets to trade and invest in – including stocks, ETFs, crypto, CFDs, currencies and commodities (such as gold).

AJ Bell is well established, with a good reputation.

It's one of the cheapest traditional stock brokers out there (charging a low annual fee).

There's a huge range of investment options – pretty much every investment out there (including both funds and shares).

The customer service is great too.

Overall, it's one of the best options.

A General Investment Account doesn’t have a fixed cost, it depends on which investment platform you want to open. They all have different costs, and all offer different investment options.

For instance, a trading platform would often have very low, or no account fees (costs to just have an account), but charge trading fees when you buy and sell investments.

Whereas a typical investment platform, such as an expert-managed platform and a self-managed platform, would typically charge account fees based on the amount of money you have invested (which can range from 0% to 2% per year).

And again this varies depending on the service you’d like, such as the experts managing everything for you, which is typically more expensive than managing your own investments.

So it’s best to decide on what you’re after first, and then compare the costs if there’s two very similar options that you like. Our recommended options above take fees into account, and they’re some of the cheapest you’ll find.

Yep, all General Investment Accounts in the UK are authorised and regulated by the Financial Conduct Authority (FCA). That means they’ve been reviewed and approved to look after your money. You can also check the FCA register if you want to check if a specific investment platform is authorised.

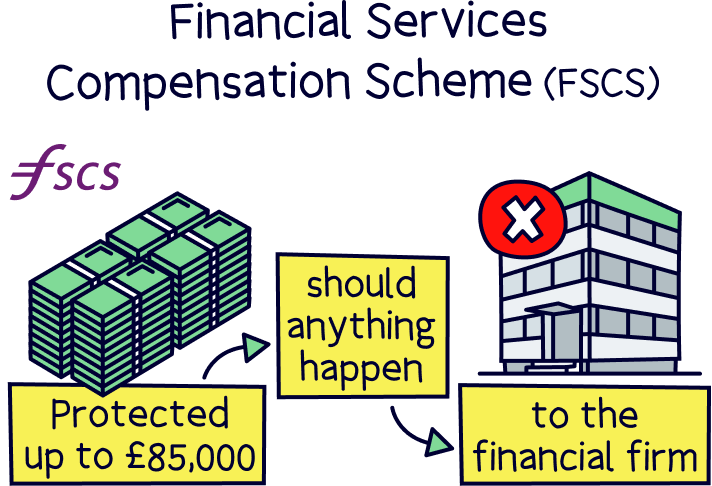

They are also all part of the Financial Services Compensation Scheme (FSCS). This means that if anything happens to the investment platform, such as going out of business, you’ll get up to £85,000 back if you have any cash within the platform itself.

However, your money would normally be in the investments themselves, and these will be stored with an investment provider, with all of your investments in your own name, completely separate to the platform's money, and can only be returned to you.

Pretty simple really right? Unfortunately General Investment Accounts have no tax-free benefits like an ISA or a pension, however they are still useful!

You can use them in addition to your ISAs once you've saved £20,000 within a tax year, such as using a GIA to buy stocks in certain companies you think are good investments, or maybe having the experts manage some of your investments for you.

There’s lots of options for a GIA – it simply depends on what your investing goals are and what you’re looking to do.

If you’re looking to add a General Investment Account to your investment strategy, check out the best investment platforms to find the best one for you.

We’ve reviewed the best investment platforms so you can find the best for you.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things investing, with many years of combined experience writing and talking about investing and trading. Some of our team were top financial advisors. We understand and love helping people learn more about both short term trading and investing for the long term – investing can be a great way to grow your money over time.

More than 20 years of combined experience researching and writing about investing

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of trading and investing companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

We’ve reviewed the best investment platforms so you can find the best for you.