Find out how much you could borrow, and your monthly repayments, for a buy-to-let mortgage.

Property value

Deposit / equity

Mortgage needed

Rental income

Interest rate

More options

Setup fees

Length

Interest-only?

(If you're only paying interest, not repaying the mortgage)

Buying in Scotland?

(For Land and Buildings Transaction Tax (Stamp Duty))

Buying in Wales?

(For Land Transaction Tax (Stamp Duty))

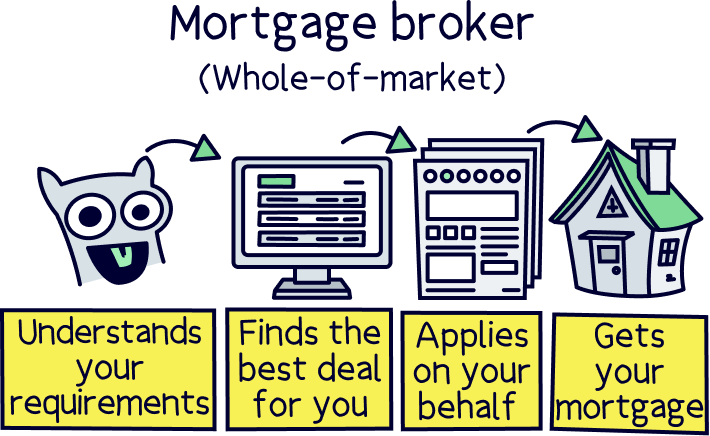

It’s a simple one – use a mortgage broker!

There’s a lot of mortgages out there, and it’s pretty difficult to search them all, in fact, you likely won’t be able to find most of them yourself, and some deals are only given to mortgage brokers.

And, all the different lenders have different criteria for giving out mortgages – things you probably won’t know until you after you apply for a mortgage.

A mortgage broker (also called mortgage advisor) can search every mortgage deal out there, to find the very best mortgage deal for your specific situation and the property itself – they know all the different lenders and which ones will be perfect for you (and the highest chance of getting the mortgage so you can avoid getting your application rejected, and potentially affecting your credit score).

They’ll also be able to get the very best mortgage (typically the lowest interest rate), which can mean the difference of £100s per month – saving you a small fortune. They’ll also help you remortgage (switch deals) in future, so you’ll always be on the best mortgage for your property.

We think they’re worth their weight in gold…

Our top pick for a mortgage broker is Tembo¹, thanks to their pretty epic customer service, and expertise in buy-to-let mortgages (you’ll get 50% off with Nuts About Money too).

And we also think Habito¹ are pretty great too (they’re online, and fee-free). For all the top options, here’s our top mortgage brokers.

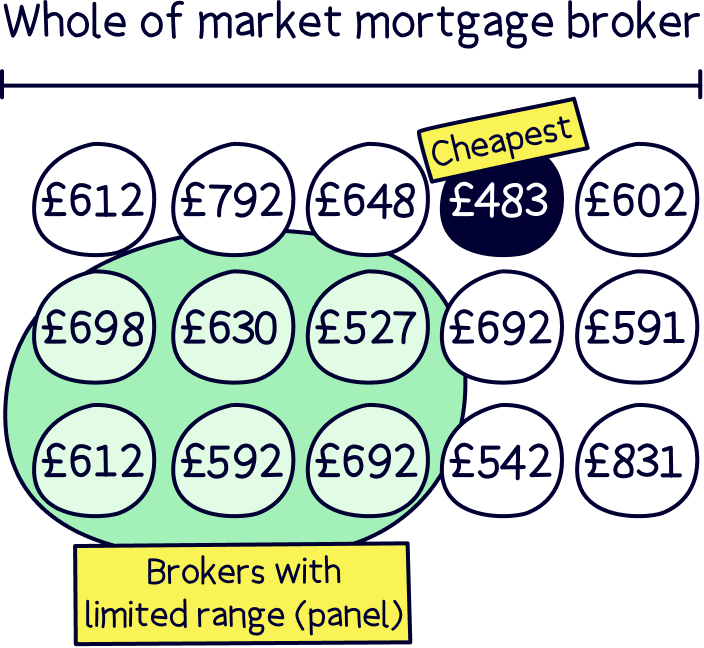

Nuts About Money tip: make sure you use a ‘whole-of-market’ mortgage broker – that means they can search all the mortgages out there. Some brokers can’t, and so can’t guarantee the best deal.

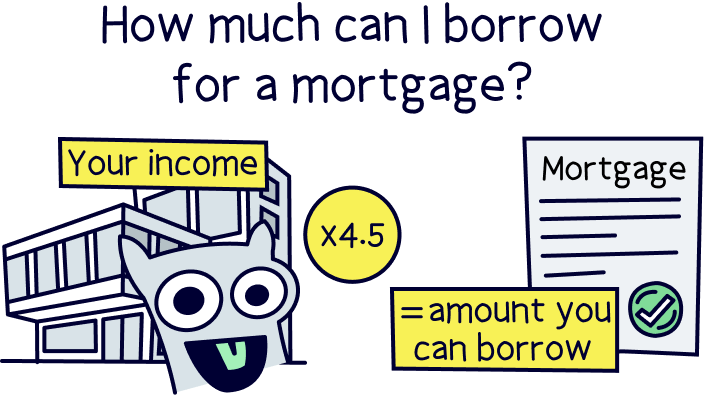

You might be familiar with residential mortgages, which is a mortgage to buy a property you live in, and the amount you can borrow is typically based on how much you earn (and normally around 4.5x your income).

However, with buy-to-let mortgages, it’s completely different. The lender will use the expected monthly rent and the property value to determine how much you can borrow.

It can be a bit complicated, which is why our buy-to-let mortgage calculator is so useful (if we do say so ourselves) – here’s how it works:

We said it was simple right? Oh wait, no, we said complicated. Here’s a quick example to explain it better…

Let’s say your estimated rental income is £12,000 per year, that would mean your maximum amount of interest allowed (your mortgage repayments) would be £9,600 (£12,000 / 125%).

We take that £9,600 and divide it by the stress interest rate of 5.5%, which gives a total of £174,546 that you are allowed to borrow for that property.

You then need to remove the deposit to get the actual mortgage amount, so for a 25% deposit (often the minimum allowed) on a £200,000 property, that would be £50,000, and so we arrive at £150,000.

Note: if you are doing the calculations yourself (to check our maths), you need to use decimals, so 125% becomes 1.25, and 5.5% becomes 0.055.

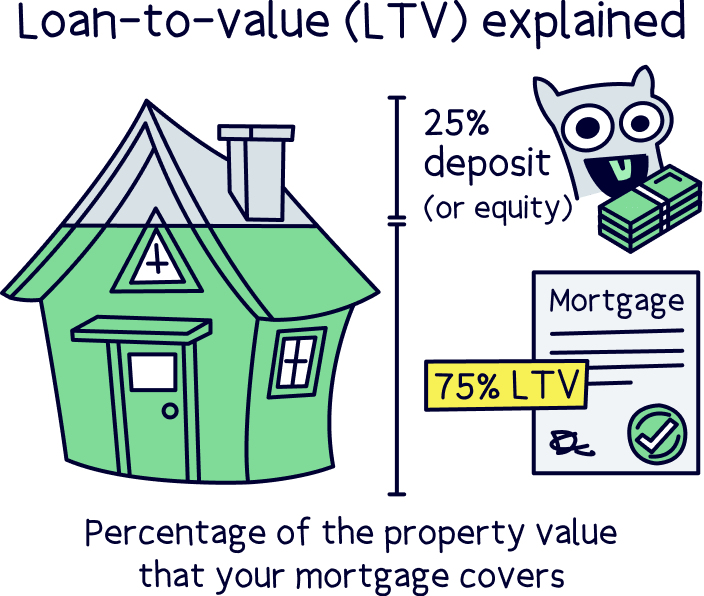

Loan-to-value, or commonly called LTV, is the amount of mortgage on the property compared to your deposit, or equity (if you already own the property).

So if the property value is £200,000 and your deposit or equity is £50,000, which is 25% of £200,000, the mortgage covers the remaining 75% of the property, and so the LTV is 75%.

For most buy-to-let mortgages, mortgage lenders will ask for at least a 25% deposit, which means 25% of the property value is your own cash, rather than the mortgage lender's money.

This is to reduce the risk for the mortgage lender as you’ll typically be repaying the mortgage from the rental income, which isn’t guaranteed.

However, depending on the mortgage lender and the property, you may be able to get a mortgage with as little as 15%, although they are hard to find. It’s best to speak to a mortgage broker to discuss your options, and help you find the right mortgage for you.

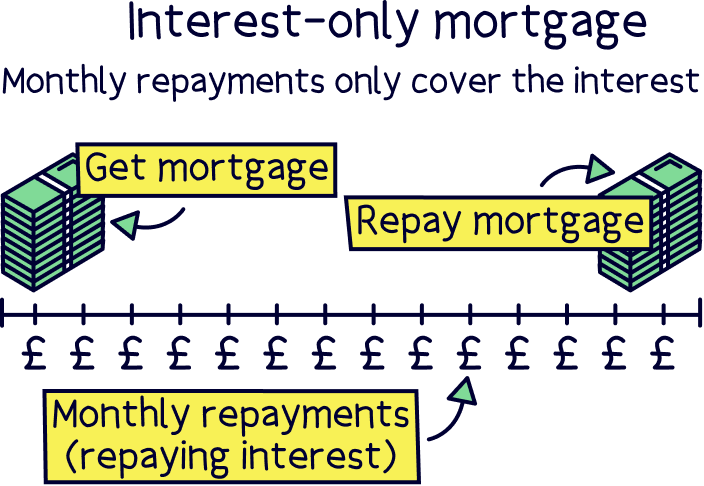

In our calculator we’ve set the default setting to interest-only. This is because most buy-to-let mortgages are interest-only, which simply means you pay off the interest each month, rather than any of the actual mortgage.

Buy-to-let investors typically opt for this option because it increases the cash they receive each month (their cash flow), which they can use to invest elsewhere or support themselves.

They would then pay off the mortgage when they sell the property.

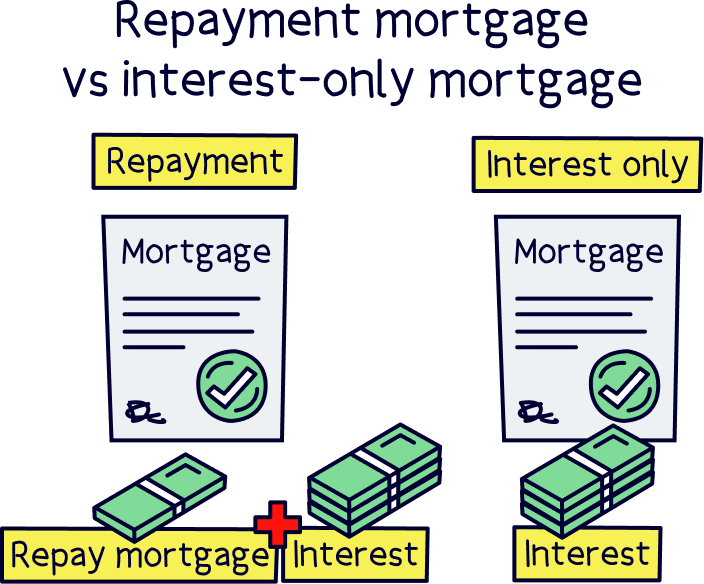

Note: you can opt for a ‘repayment’ mortgage, where you pay off some of the mortgage each month too, although the monthly repayments will be much higher.

In order to get a buy-to-let mortgage, most lenders will ask for a 25% deposit, and that you’re not a first time buyer (although not always), and that you have an annual income of at least £25,000.

This is to reduce the risk for the lender that you’re not going to live in the property yourself (which is not allowed with buy-to-let mortgages), and that you’re able to cover the repayments should you not have any tenants in the property.

When purchasing property in the United Kingdom (England, Scotland, Wales and Northern Ireland), unfortunately, you’ll need to pay tax – and beware, it’s a lot, and even more for most buy-to-let investors, where higher rates are charged for buying properties in addition to your main residence (3% more in England and Northern Ireland, 6% more in Scotland and 3-4% more in Wales).

Note: in our calculations, we’ve used the higher rates for additional properties (all the rates below).

In England and Northern Ireland this tax is called Stamp Duty Land Tax (SDLT, or Stamp Duty for short), and here’s what you’ll pay:

Note: you’ll pay the tax rates that apply to the property price range, it’s not the rate for the whole property price. So, if it’s £300,000, you’ll only pay 5% on £50,000 if it’s your main home.

If you’re a first time buyer, your tax free limit rises to £425,000, unless the property is over £625,000, in which case your limit falls back to £250,000. However, if you’re buying your first property to rent out, you won’t get the discount at all.

And if you’re buying an additional property, the higher rate only applies if the property is worth more than £40,000.

In Scotland, the tax is called Land and Buildings Transaction Tax (LBTT). Here’s what you’ll pay:

If you’re buying an additional property, the higher rate only applies if the property is worth more than £40,000.

In Wales, this is called Land Transaction Tax (LTT), and here’s what you’ll pay:

Buy-to-let mortgages can be pretty complicated when it comes to determining how much you can borrow, so we hope this buy-to-let mortgage calculator makes things a bit easier.

How much you can borrow all comes down to your expected rental income, the property value and your deposit size. Ideally you want at least a 25% deposit, a high monthly rent, and low property value – but finding that is easier said than done!

Once you've found a great property, we recommend using a mortgage broker to find the best mortgage for you. They really are worth their weight in gold and could save you £100s per month, which you could invest elsewhere, or pocket yourself – better you have it than a bank.

Oh by the way, for your mortgage on your own home, check out our mortgage repayment calculator to get an idea of how much you could borrow and your monthly repayments.

All the best with your buy-to-let property!

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Get the best deal and award-winning service with Tembo. Plus 50% off.