Article contents

Getting a buy-to-let mortgage and becoming a landlord is easier than you might think. All you need is a good deposit, a nice lender and the right property.

Thinking of becoming a landlord? Want to generate some extra cash by renting out a property? A buy-to-let mortgage could be right up your street. Here, we’ll take a look at everything to do with buy-to-let mortgages, from what they are to how they work and who can get one. Enjoy!

A buy-to-let mortgage is a long-term loan that lets you buy a property and make money from it by renting it out. Kerching!

It’s pretty similar to a standard residential mortgage, but it’s designed for people who want to become landlords. Basically, if you’re buying a property to rent out, most lenders (the people who give you your mortgage) won’t want you to do this on a residential mortgage. That’s because these are designed for people who want to live in the property they’re buying, and they normally have rules that say you’re not allowed to rent your property out.

Instead, you’ll normally need a buy-to-let mortgage. This way, you can rent your property out – and make money from it – for as long as you want. Happy days!

Tembo will find your best deal, fast, all with award-winning service.

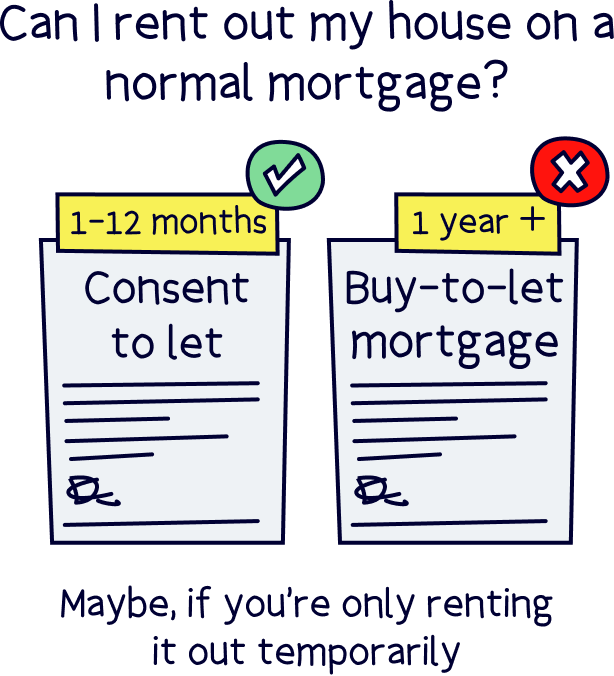

Okay, we know what you’re thinking: do you have to get a buy-to-let mortgage to rent out a property? Well, yes and no.

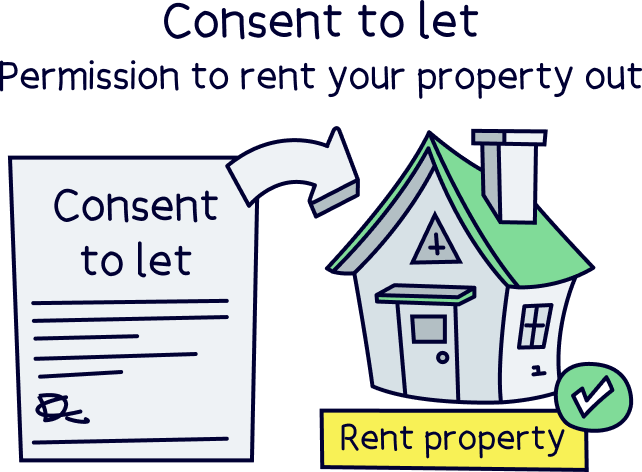

If you own a property on a residential mortgage and you suddenly find that you need to rent it out for a few months, your lender might give you something called ‘consent to let.’ That’s permission to rent out your property short-term on your standard residential mortgage (although they might change your rates).

However, if you want to become a landlord and rent out a property long-term (normally for over a year) then yes. You’ll need a buy-to-let mortgage.

Either way, you’ll need to let your lender know you want to rent your property out – if you rent it out on a standard residential mortgage without permission, you could be permitting ‘mortgage fraud,’ which is a pretty serious offence. If your lender finds out, they could make you pay your mortgage back instantly (and how many of us could really afford to do that?!). It could also damage your credit score, which could make it harder for you to get another mortgage in the future.

If you’re not sure whether you need a buy-to-let mortgage, check out our guide to whether you can rent your house out on a normal mortgage.

Buy-to-let mortgages work similarly to residential ones, but there are a few key differences.

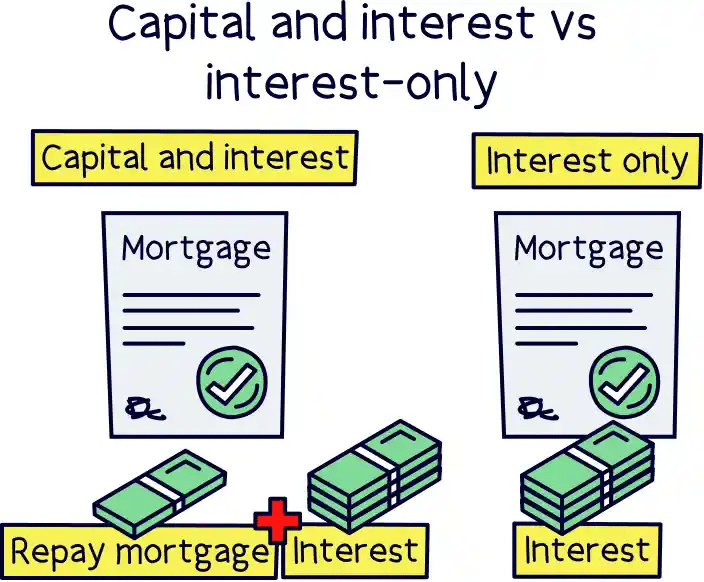

First, most residential mortgages are ‘capital and interest’. This means that in your monthly repayments, you’ll be paying off the interest you’re charged and a portion of the actual loan. However, most buy-to-let mortgages are interest-only. That means in your monthly repayments, you’ll only pay off the interest and not the loan itself. Instead, you’ll need to pay the whole loan back as one big lump sum at the end of your mortgage term.

Buy-to-let mortgages also come with higher rates and fees than residential ones. This is all to do with the fact that they’re riskier for lenders.

Basically, your lender might be worried about whether you’re going to be able to afford your monthly repayments if, for some reason, you end up without any tenants for a while. Or if your tenants don’t pay their rent on time.

Just remember though: the whole point of a buy-to-let mortgage is that it will allow you to make money from your property. So, yes, your mortgage might be more expensive than a residential one. But fingers crossed, your rental income should more than cover all that. Get in!

Got your eye on the perfect buy-to-let property? Wondering how big a mortgage you can get your hands on for it? Well, the amount you can borrow on a buy-to-let mortgage depends on two main things…

Nuts About Money tip: find out how much you could borrow with our buy-to-let mortgage calculator.

When you’re buying a buy-to-let property, you’ll normally need to put down a deposit that’s at least 15% of the property’s value. However, many lenders will want a deposit of 25% or more, while you’re likely to be able to access the best rates if you can put down a deposit of 40% or more.

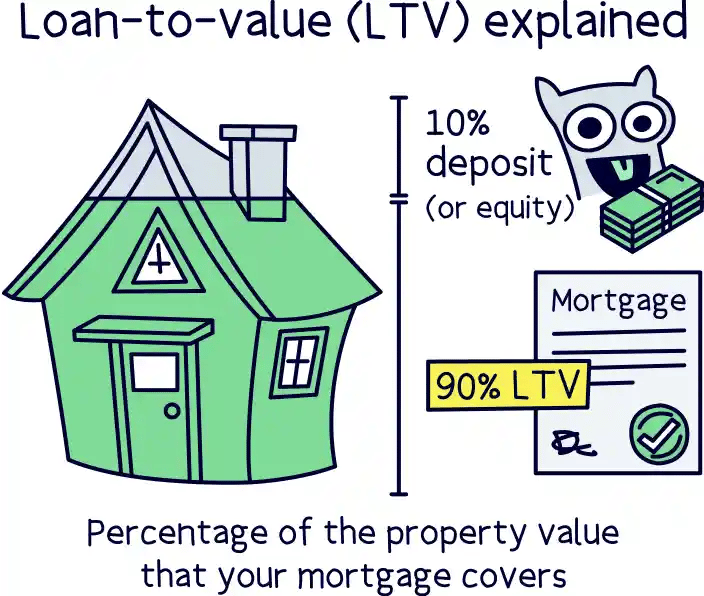

This is all to do with the loan-to-value ratio (LTV). LTV basically refers to what percentage of the value of the property you’re taking out as a loan.

Confused? Let’s say you’re buying a property that’s worth £200,000. If you put down a £50,000 deposit (25%), you’ll be borrowing the remaining £150,000 (75%) from your lender. This means you have an LTV of 75%.

Many lenders won’t want to give you an LTV of more than 75% for a buy-to-let property. This is because, if you don’t keep up with your monthly mortgage repayments, your lender will need to sell your property to make their money back. Normally, they’ll do this for a discount at auction to make things happen quicker. The higher the LTV, the more likely it is that they won’t be able to sell the property for enough money to get their loan paid back in full.

That said, although you can usually get the best rates if you go for a lower LTV, do the maths first. If you’re starting a property empire or you’re going to refurbish your property, you might want to keep some cash and go with a higher LTV. Everyone’s different!

With a buy-to-let mortgage, the chances are you’ll be relying on the rental income you receive to be able to afford your monthly mortgage repayments. So, your lender will do some careful checks to work out how much income they think you can generate from your property, before deciding how much they’re happy to lend you.

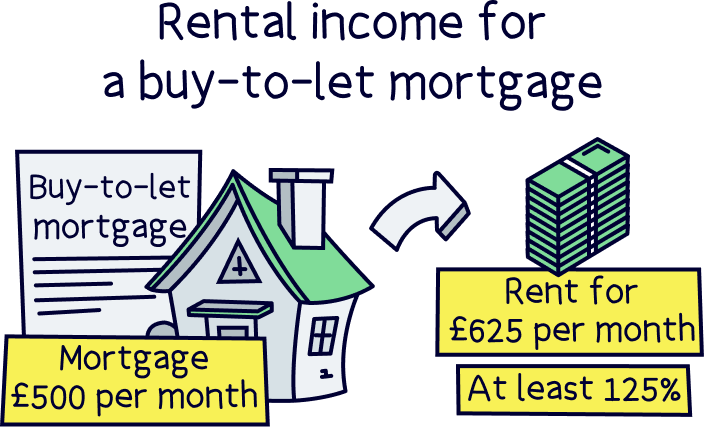

As part of this, they’ll carry out something called a ‘stress test.’ This is where they take the interest rate of the mortgage you’ve applied for and add 2% (to a minimum of 5.5%). Then, they’ll check to make sure that your yearly rental income will be at least 125% of that figure (although 145% is becoming more and more common). This percentage is known as the interest coverage rate, or ICR.

Don’t worry, it’s not as complicated as it sounds!

Let’s say you’re hoping to borrow £100,000 and your interest rate is 3%. For the purposes of the stress test, your lender will add 2% to your interest rate, bringing it to 5%. Because that’s below the minimum interest rate, they’ll then round this up to 5.5%. This would bring the yearly interest to £5,500 (because that’s 5.5% of the amount you want to borrow). Your lender will then times this by 145% (or 125%, depending on the lender’s ICR), to get to a final figure: £7,975.

This means that, over the course of a year, you’ll need to be able to earn at least £7,975 in rent from your property.

The idea is that this way, you’ll have enough income to easily cover your mortgage repayments along with all your other landlord costs (like insurance and maintenance) – even if you end up with gaps between tenancies. If your lender doesn’t think that’s possible, they won’t let you have the mortgage.

Right, so here’s the big question – will you qualify for a buy-to-let mortgage? Well, it’s impossible to say for sure, since every borrower and every lender is different. That said, here are a few things that most lenders will look at.

Do you own the house you’re currently living in? If so, that’s great news! Most mortgage lenders will want to see that you have at least one residential mortgage before approving you for a buy-to-let one.

Huh? Why does it matter?!

Well, most lenders would rather buy-to-let borrowers weren’t living in rented accommodation. This is all to do with rental prices – lenders will worry that your rent will be more expensive than the rent you’re earning from your buy-to-let property, which could stretch you financially.

They might also worry about whether you’d still be able to afford your rent if you had a gap between tenancies. The last thing they want is for you to end up in financial trouble, as this will make it harder for them to get their money back.

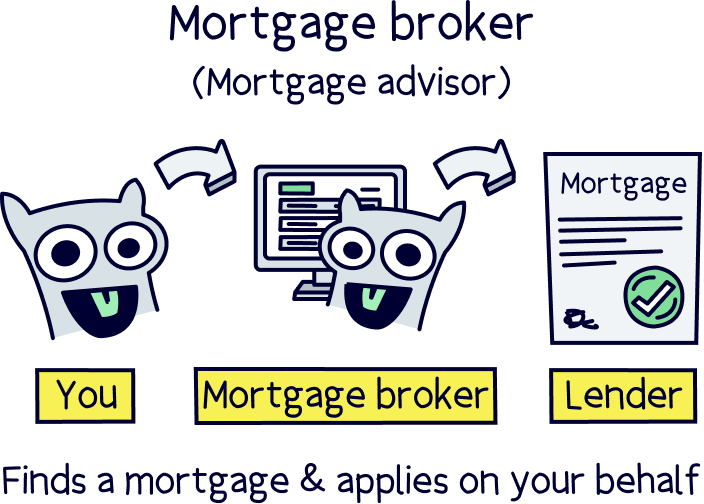

That isn’t to say that you can’t get a buy-to-let mortgage if you’re living in rented accommodation. Just that there’ll be fewer lenders to choose from. A ‘whole-of-market’ mortgage broker (also known as a mortgage advisor) will be able to compare mortgages from lots of different lenders to help you find one that works for you.

Not sure where to find a good broker? Check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

Do you have a stack of unpaid bills and credit cards piling up on your doormat?

Let’s hope not, because one of the most important things a lender will check before offering you a mortgage is your credit score. That’s a score that shows lenders how good you’ve been with money in the past.

To put it bluntly, if your credit score is looking a bit peaky, you’re going to find it hard to get a buy-to-let mortgage. After all, how will a lender be able to trust that you’re going to pay them back if you haven’t paid back other loans in the past?

Your lender will also want to check how many other loans you’ve got. This is so they can make sure you’re not going to be stretching yourself too far financially.

All this to say that, before you apply for a buy-to-let mortgage, get up-to-date with your bills, pay back any unpaid credit cards and reduce your borrowing. Yep, that means no more ‘pay monthly’ holidays until after you’ve been approved (sorry!).

You know how we said that lenders will want to calculate how much rental income you’ll be earning from your buy-to-let property? Well, that’s enough info for some lenders.

However, other lenders will also want to know what other kinds of income you have. Basically, they just want to be extra sure that you’re going to be able to afford your monthly mortgage repayments, even if nobody ends up renting your property for a few months.

For this reason, you might struggle to get approved for a mortgage if you’re earning less than £25,000. Don’t get us wrong, it won’t be impossible. After all, some people make all their income from renting out properties! It’ll just reduce your options.

Okay, okay, so we know it’s not polite to ask your age. To be honest, we don’t care how old you are, but sadly, lenders do (don’t shoot the messenger!).

Your mortgage lender will have an upper age limit (normally between 70 and 75) and you’ll need to make sure you’re below that age limit when your mortgage ends.

Let’s imagine you’re 35. You’ll probably be fine to take out a 35-year mortgage (but only just!) as it’ll end when you’re 70. However, if you’re 45, you’ll probably need to look at a shorter mortgage term, for example, 25 years. That way, you can still avoid going past the upper age limit.

This is all to do with your lender worrying about ‘affordability’ (whether or not you’re going to be able to afford to keep up with your mortgage repayments). In other words, you might be able to afford your mortgage repayments now, but will that still be the case once you hit retirement age? Most lenders won’t want to take the risk.

Do you already own other buy-to-let properties? If you own 4 or more that have mortgages on them, you’ll count as a ‘portfolio landlord.’ Fancy!

However, this means you’ll have some extra hoops to jump through.

Remember how we said lenders will carry out a ‘stress test’ where they check that the rent you earn is going to be at least 145% of your mortgage repayments? Well, if you’re a ‘portfolio landlord,’ the lender won’t just carry out a stress test on the property you’re hoping to buy. Instead, they’ll carry out a stress test on every property in your portfolio individually.

In other words, you’ll need every property in your portfolio to pass the stress test before your lender will let you have another buy-to-let mortgage. Urgh.

If you’re worried that your portfolio won’t pass, you could look for a lender that does something called ‘top slicing.’ This is where they take your personal income into account and use it to subsidise any shortfalls in your properties’ earnings during the assessments. Not many lenders do it, but there are a few.

On top of this, depending on the lender, you might have to pass some other tests. For instance, some lenders will want to see that, across your whole portfolio, your LTV is less than a certain figure (for example, under 65%). Others will limit the number of properties that they’ll let you have in your portfolio (often to 10).

Every lender is different, so we’d recommend getting in touch with a ‘whole-of-market’ mortgage broker. They’ll be able to look through all the mortgages being offered by all the lenders to find the one that’s best for you.

Because a buy-to-let property is designed to make you money, you’ll have to pay more taxes on it than you would with a residential property that’s designed for you to live in. Here are some of the tax considerations you’ll need to bear in mind before you take the plunge.

The money you make from rent on your buy-to-let property is classed as income. So, you’ll need to declare it on your Self Assessment tax return and pay income tax on it!

In the UK, everyone gets a tax-free allowance of £12,570 (unless you’re earning over £125,140). But anything you earn above this will be taxed at 20%, 40% or 45%, depending on how much money you’re making.

Just remember that you can subtract allowable expenses like property maintenance, Council Tax and letting agent fees from your rental income, so you don’t have to pay tax on them. You can find a list of these expenses on the Gov.uk website, although it might also be worth getting an accountant to help you out to make sure you’re as tax efficient as possible.

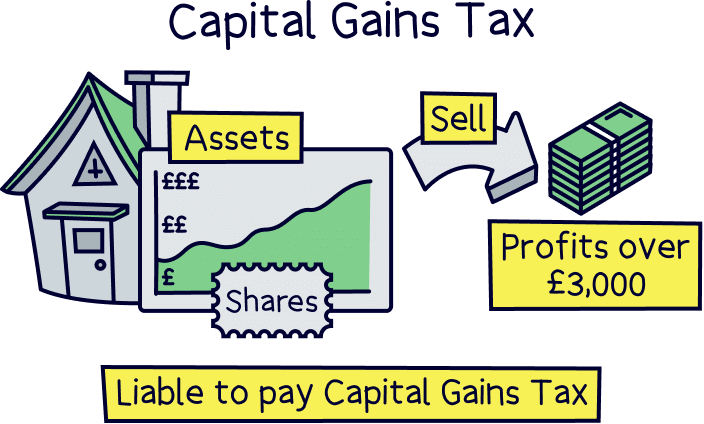

Capital Gains Tax is a tax you have to pay when you sell something that’s increased in value. You don’t have to pay it if you sell the home that you live in (assuming you only have one!). But you do have to pay it if you sell a buy-to-let property.

Everyone has a tax-free Capital Gains Tax allowance of £3,000. In fact, if you own your buy-to-let property jointly with a partner, you could combine your tax-free allowances.

However, after that, any income you make from selling your buy-to-let property will incur a charge of 18% (if you’re a basic taxpayer) or 28% (if you’re a higher-rate taxpayer). Ouch!

Up until 2017, landlords benefited from this great thing called ‘mortgage interest tax relief.’ What it meant was that landlords didn’t have to pay tax on the income they were using to pay off the interest on their mortgage. However, mortgage interest tax relief has now been replaced with a 20% tax credit.

The 20% tax credit means that landlords get taxed on all their earnings, including the income they use to pay their interest. However, they get 20% of it back pound for pound.

This is great for landlords who fall into the lower tax bracket. They’ll only be paying 20% in tax anyway, so with the 20% tax credit, they get all that tax back.

However, landlords who fall into the higher and additional rate tax brackets (40% and 45%), will still only get a 20% tax credit. So will lose out by the difference, 20% and 25%. Basically it’s double the tax for higher rate taxpayers.

When you buy any property, you have to pay a tax called Stamp Duty Land Tax (more commonly known as just Stamp Duty). Exactly how much you have to pay depends on how much your property costs and whether you’re a first-time buyer.

Note: First time buyers don't pay any Stamp Duty up to £300,000, and then it's the usual amount.

Nuts About Money tip: To find out how much Stamp Duty you might have to pay check out our Stamp Duty tool if you are buying in England or Northern Ireland. We also have a Land and Buildings Transaction Tax tool if you are buying in Scotland and a Land Transaction Tax tool for Wales.

Annoyingly for would-be landlords, if you’re buying a buy-to-let property that costs more than £40,000 (and let’s be honest, most do!), you have to pay an extra 5% on top of the standard stamp duty tax.

Here’s how much you’ll have to pay:

You'll pay the rate on the portion that falls into the price range. So 5% on the price between £250,001 to £925,000, and then 10% on the portion above that up to £1.5 million, and so on.

Most people who get a buy-to-let mortgage do it as a private landlord. This is where you buy the property and take out the mortgage in your own name.

However, you can also get a buy-to-let mortgage as a limited company. This is where you set up a company, and then buy the property and take out the mortgage in the company’s name, rather than as an individual.

So, which is better?

Well, everyone’s different and there’s no one right answer. However, here are some pros and cons of getting a buy-to-let mortgage as a limited company.

Basically, before you close your laptop and start thinking of cool business names, take some time to do the maths. Switching to a limited company could be a great shout for some, but there’s just no point unless you’re going to be making a decent saving!

Most of the big banks offer buy-to-let mortgages and some specialist lenders do too. However, their requirements and deals will all be quite different. Not only will they all offer different interest rates, but some will charge additional fees too. So, make sure you take your time to weigh up everything carefully before taking the leap.

We’d always recommend talking to a ‘whole-of-market’ mortgage broker who can scour all the deals out there to find the best lender and the best mortgage for you. Not only will they take the time to find out more about your circumstances and requirements, but they’ll fill out the whole mortgage application for you too. They’ll even be able to give you some advice about whether you should take out your buy-to-let mortgage as a limited company or as an individual.

That’s right, you just sit there with your feet up watching telly while they do all the dirty work. You’re welcome!

Got your eye on the perfect buy-to-let property? Can’t wait to get that lovely rental income flowing into your pocket each month? As you can see, becoming a landlord is totally doable and a lot easier than you might think.

All you have to do is get in touch with a mortgage broker and they’ll be able to point you in the right direction. Before you know it, you’ll be signing tenancy agreements and getting your first cheque through the post (okay, okay, your first bank transfer…).

It really is that easy! We recommend you check out Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money.

Good luck!

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.