Article contents

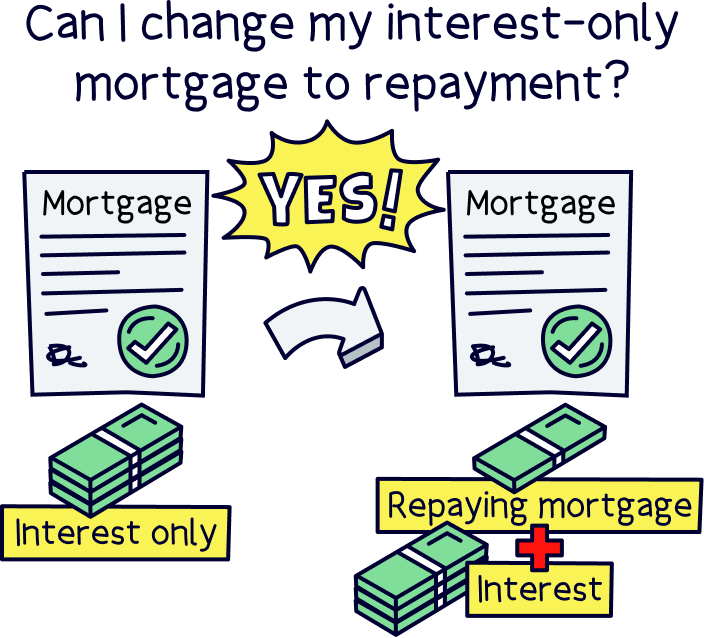

Yes! Most mortgage lenders will let you change your interest-only mortgage to repayment mortgage, as long as you’re able to prove that you can afford the new monthly repayments.

On an interest-only mortgage? Thinking of switching over to a repayment mortgage? You’re in luck! We’ve broken down the pros and cons, as well as how it all works. Enjoy!

Tembo will find your best deal, fast, all with award-winning service.

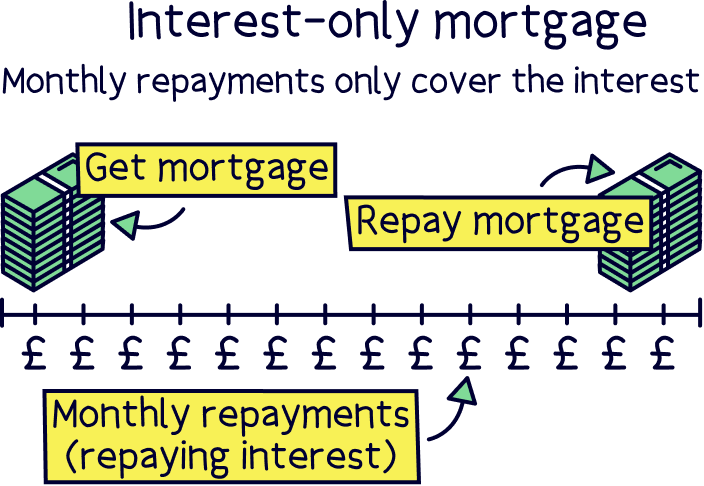

An interest-only mortgage is when your monthly repayments only cover the interest that’s building up on your loan. This means that when your mortgage comes to an end, you’ll have to pay your mortgage back, every penny you borrowed!

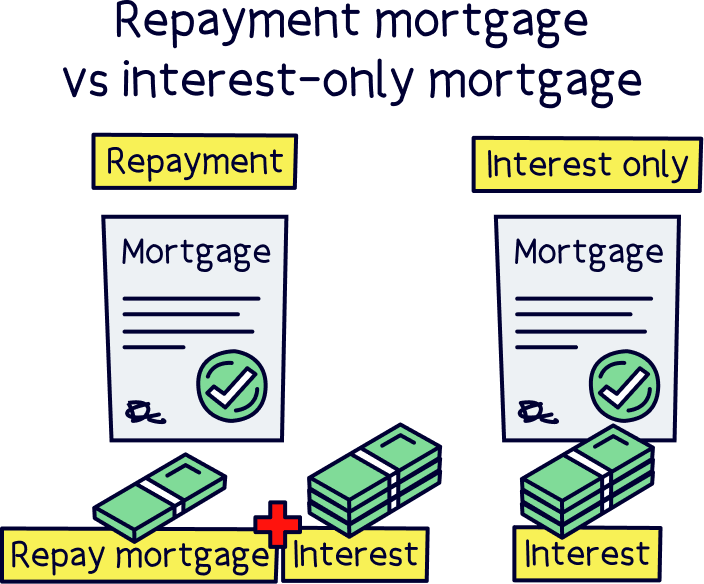

On the other hand, around 65% of homeowners are on what’s called a repayment mortgage (according to Experian). This is when your monthly repayments cover both the interest and a contribution towards paying off the loan itself. By the end of a repayment mortgage, the idea is that you’ll have paid off the loan completely and you’ll finally own your house outright. Get in!

Well, there are a few reasons. But first and foremost, a repayment mortgage could give you some peace of mind...

If you can’t afford to pay back your interest-only mortgage in one lump sum, you’ll have to take out a new mortgage – or, if worst comes to worst, sell your house. Yep, you heard us right. It can be pretty nerve-wracking!

Switching to a repayment mortgage where you pay off the interest and loan in monthly instalments can make your mortgage easier to manage.

That said, lenders (the people that give out mortgages) won’t give you an interest-only mortgage unless you have a solid plan for how you’re going to pay it back. This is known as a ‘repayment vehicle’ and can include plans like selling a buy-to-let property (where you rent the property out), or paying into a savings account or investment account each month.

In other words, even though paying back the full loan as a lump sum might sound scary, you won’t usually be in this position unless you’ve proven you can handle it.

That depends. Interest-only is probably a bigger risk than a repayment mortgage, but some of us are more willing to take risks than others.

Ultimately, only you can make the decision. But to help, here are some of the pros and cons of switching to a repayment mortgage.

Nuts About Money tip: See the latest interest rates with our mortgage comparison tool. Or get expert help with a mortgage broker.

Yes! Changing from an interest-only mortgage to repayment is normally fairly straightforward (and a lot easier than changing your mortgage to interest-only!).

Put yourself in your lender’s shoes – while you’re on an interest-only mortgage, they’ll have to wait for potentially decades to get a single penny of the money they lent you back (assuming the interest doesn’t count). But if you switch to a repayment mortgage, they’ll get some money back in their pockets every month.

This makes it a lot less risky for them. So, they’ll probably be pretty happy that you want to make the switch. That said, there are a couple of things that you’ll need to bear in mind:

‘Affordability’ is all about how easily you can afford to pay back your lender. Basically, switching to a repayment mortgage will mean you have to pay a lot more each month. And the last thing your lender wants is for you to struggle to pay them back. After all, you wouldn’t want to lend someone money if you didn’t think they’d be able to pay it back on time.

Before making a decision, your lender will do some checks to see whether they think you can afford it. If they’re not convinced then they won’t let you switch. It’s as simple as that!

Not sure you’ll be able to handle the repayments? Don’t worry. There’s also something called a part-and-part mortgage.

A part-and-part mortgage is where you pay back some of your loan on an interest-only basis and some on a repayment basis. Your monthly repayments will be lower than they would be on a full repayment mortgage. But you’ll also have less to pay as a lump sum than you would on an interest-only mortgage. So, it just takes the pressure off a little. We guess you could call it the best of both worlds!

Some mortgage lenders will let you stay on your current mortgage and just switch the way you pay. Happy days!

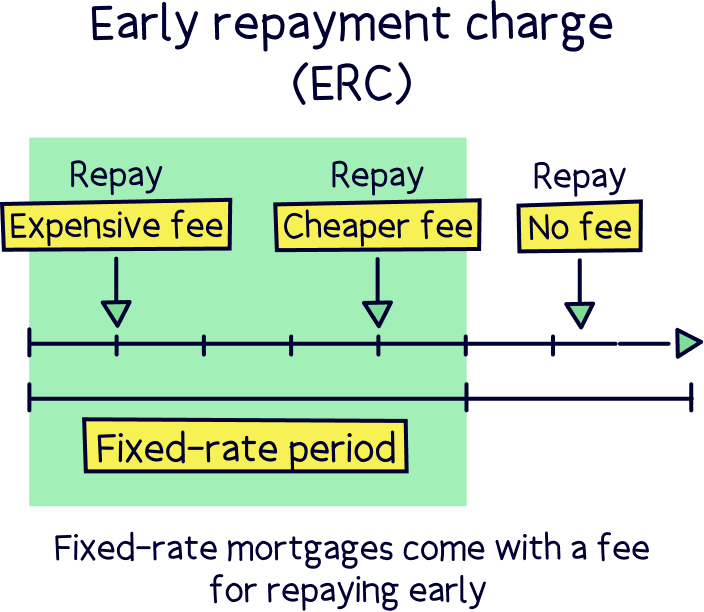

But others will want you to take out a new mortgage altogether. Let’s face it, this is essentially just remortgaging (swapping one mortgage for another). Although this isn’t a problem in itself, it could mean leaving your current mortgage in a fixed-rate period (a contract if you will), which could mean you have to pay an early repayment charge. This could come to thousands of pounds (don’t shoot the messenger!).

Similarly, switching to a whole new mortgage deal normally means you’ll end up on a different interest rate. Don’t get us wrong, this isn’t always a bad thing – you might actually find yourself on a lower interest rate than what you were on before! But there’s always a chance it’s the other way around.

If your lender’s making you switch to a new mortgage, you’ll want to weigh up all these factors before coming to a decision. It’s also a great idea to get a mortgage broker involved so that you can compare all the deals available to you – not just the mortgages your current lender can offer you. At the end of the day, we all love a good deal. And why stick with the same lender if you can get a better deal elsewhere?!

If you're not sure where to find one, check out our top mortgage brokers. Or visit Tembo¹, they've got award-winning service, and will guarantee to get you the best mortgage deal. You'll also get 50% off their fee with Nuts About Money. How great is that?

Switching to a repayment mortgage is (normally) as easy as pie. To get started, there are two main things you can do:

You could (although not recommended) send your current lender an email, pick up the phone or check out their website. Either way, most lenders will normally make it pretty easy for you to switch to a repayment mortgage.

Some will let you switch on an execution-only basis, which is where the lender just does what you ask them without giving you any advice. Others will get you to switch on an advised basis, which is what it’s called when your lender puts you in touch with one of their mortgage advisers to chat things through.

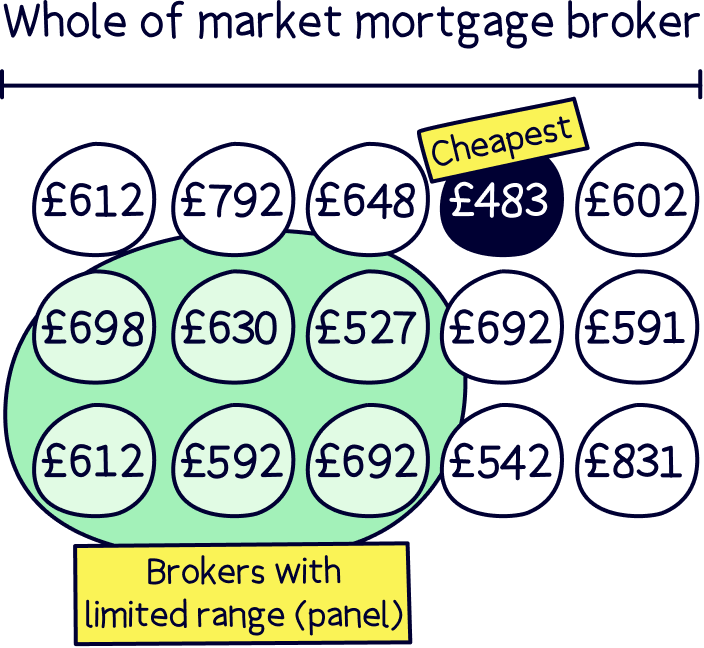

The problem with this option is that they can only show you their mortgages, and the chances are you could get a better deal elsewhere (and with mortgages, that could mean a saving of hundreds of pounds per month). If you want to get an idea of costs visit our mortgage comparison table and find out what your monthly repayments would be with our mortgage repayment calculator.

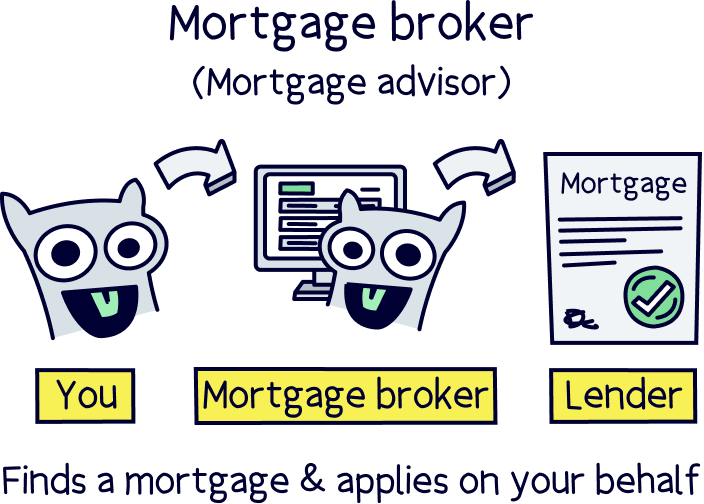

The best option is to use a mortgage broker. This is a company, or someone who can help you to get the best mortgage deal. You don’t have to use one but... well... you’ll probably want to. Especially if your lender wants you to take out a new mortgage instead of just switching the payment type on your current one.

Basically, an independent broker can search the whole market for the best mortgage deals for you. This means they’ll search every mortgage in the UK and will be able to tell you whether you could save money by switching to a different lender altogether (a little clue for you: you probably could!). On the other hand, your lender’s advisers will only be able to tell you about their own mortgages.

In other words, you’re better off talking to someone who’s looking for the best deal for you, rather than the best deal for them!

Again, here's a list of our recommended mortgage brokers.

Want to know more? Here's our guide on whether you should remortgage with the same lender.

And that's it! As you can see, an interest-only mortgage isn’t for everyone. But neither’s a repayment mortgage. And much as we’d love to sit here and tell you which is best for you, we don’t know what your circumstances are!

If you’re umming and ah-ing about making the switch, a mortgage broker can help. They’ll take the time to learn all about you and then, if you do decide to change to repayment, they can help you find the best deals. Meanwhile, you just sit back, relax and let them handle it all for you! Not sure where to find a good broker? Here’s a list of our recommended mortgage brokers.

Finally, for all things mortgages, visit our mortgage home page. Thanks for reading!

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

Tembo will find your best deal, fast, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo will find your best deal, fast, all with award-winning service.