Article contents

Current mortgage rates are changing constantly, check below for the latest mortgage rates (updated daily). We search 20,000 mortgages from over 100 lenders to work out the current rates, this represents the ‘whole of the market’ and can be used for journalism and reporting.

Nuts About Money tip: if you would like more data than shown here, get in touch with us and we'll see what we can do!

Mortgages rates have been falling slowly after the highs of 2023, where they topped over 6% – some say because of the budget that spooked the financial markets and impacted interest rates, but they were ultimately due to rise anyway, so it’s not worth dwelling on the past.

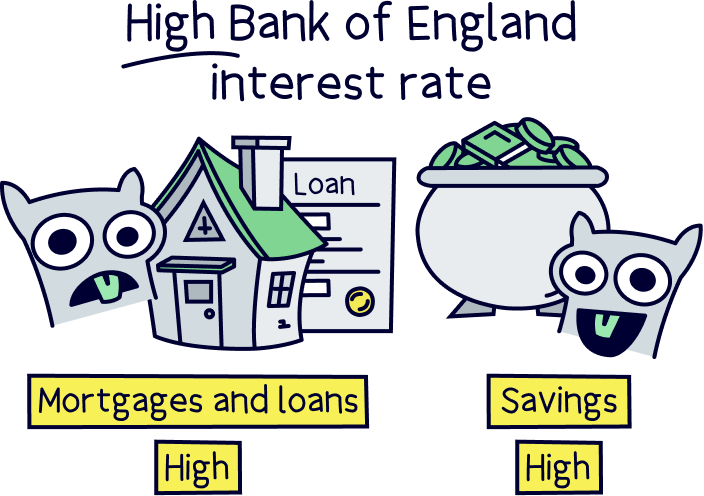

Mortgage rates typically align with the Bank of England base rate, which is the rate they set to control the economy and inflation (the price of things increasing over time). The rate is how much interest they give to banks for storing their money with them. This then often sets how much banks can provide you in interest (such as with a savings account), and also how much they charge you to borrow money (for instance with a mortgage or a loan).

So, when the Bank of England base rate goes up, so do mortgage rates, and when the base rate goes down, typically so do mortgage rates.

The base rate is a lot higher than what it has been over the last 15 years or so, and is the main reason for mortgage rates seeming very high at the moment (as we’re used to very low interest rates).

However, the base rate is not set to go back down to the lows of 2022 where it was just 0.10%. Over modern history, before 2010, 4% has been a low base rate, and it has gone to as high as 17% in 1979.

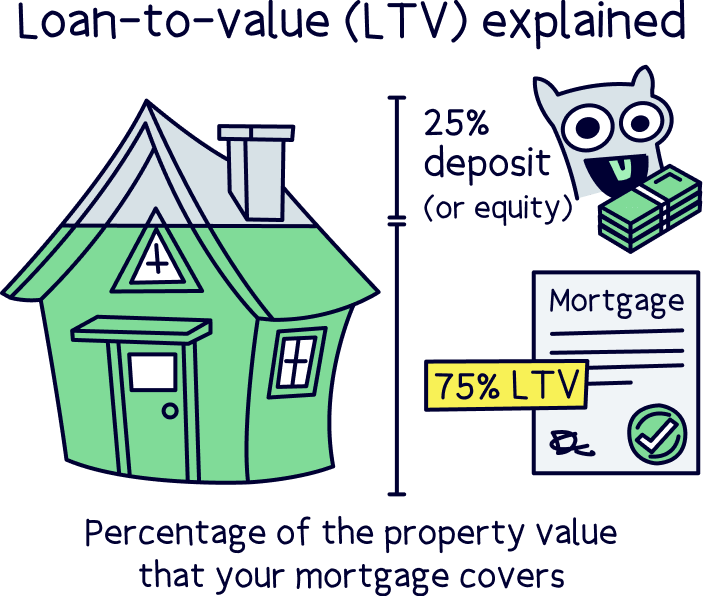

2010 to 2020 was a special time for very low interest rates that will probably never be seen again. So, using 4% as an expected figure for the base rate to be when all is ‘normal’ might make sense – meaning the current mortgage rates are probably ‘normal’ too, and they may not drop far from where they are currently in the future. For the foreseeable future, it could be wise to expect somewhere between 3% and 6% for your mortgage rate depending on your loan-to-value (the lower it is, the lower your mortgage rate).

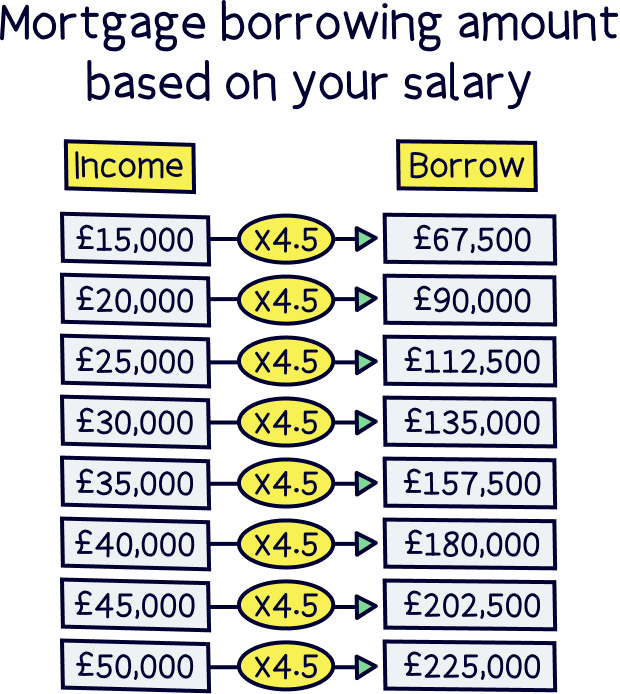

This is all down to your individual circumstances, but as a general rule, you might be able to borrow 4.5x your annual income. So if you earn £40,000 per year, you might be able to borrow up to £180,000 for a mortgage.

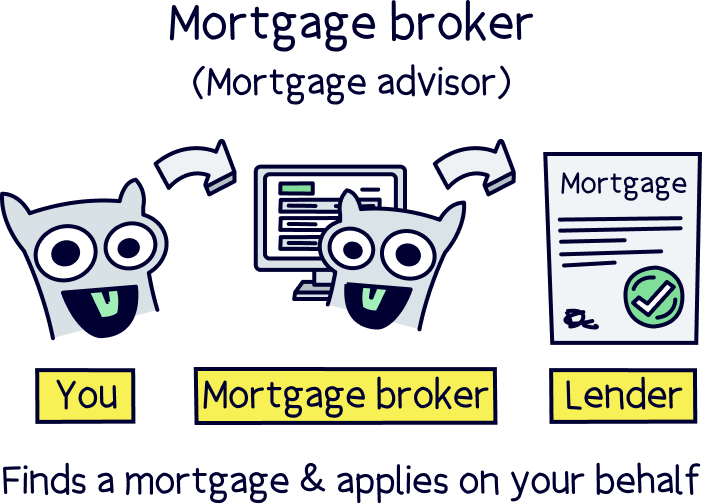

It’s best to check with a mortgage broker who can run through your financial circumstances and determine how much you can likely borrow. They’ll also then find the best deal for you, and apply for the mortgage on your behalf. Easy right?

If you’re not sure where to find a great mortgage broker, we recommend Tembo¹, you’ll get the best deal, and they have award-winning service. Plus they can help you borrow more than you otherwise could. For all the top options, check out the best mortgage brokers.

This bit is easy too. We’ve done the hard work for you. Head over to our mortgage repayment calculator, and enter in your mortgage amount, how long you’d like the mortgage for, and the interest rate, and it will tell you how much your monthly repayments will be, and how much you’ll pay over the lifetime of the mortgage.

All the best finding the best deal with your mortgage. Don’t forget to use our mortgage comparison tool to help you on your way.

Check out Tembo, they’ll find the best deal for you, all with award-winning service.

Check out Tembo, they’ll find the best deal for you, all with award-winning service.

Check out Tembo, they’ll find the best deal for you, all with award-winning service.

Check out Tembo, they’ll find the best deal for you, all with award-winning service.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Check out Tembo, they’ll find the best deal for you, all with award-winning service.