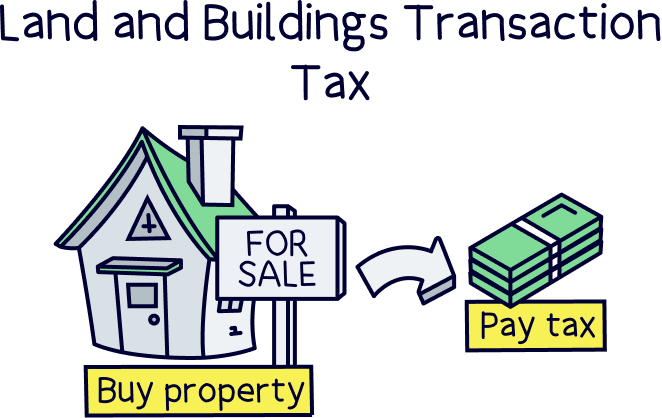

Otherwise known as Scottish Stamp Duty – find out how much to pay for your residential property in Scotland.

First time buyer?

(Buying your first home to live in)

Additional property?

(Buy-to-let or second home)

Note: this LBTT calculator includes the higher rate for additional properties introduced on 5th December 2024.

We hope this helps you plan for your new home in Scotland.

We’ve sorted all the complicated maths behind the scenes to make things easy for you – just add your property value and see how much you’ll need to pay in Land and Buildings Transaction Tax (LBTT).

If you do want to run through the rates (and check our maths), the rates are just below.

Nuts About Money tip: if you’re not sure how much you can borrow for a mortgage, or your repayments, check out our mortgage calculator.

Land and Buildings Transaction Tax is what Stamp Duty is called in Scotland (we’re presuming you might be more familiar with the name of Stamp Duty!).

It replaced Stamp Duty Land Tax (SDLT) in 2015 (for Scotland only), and has different rates to Stamp Duty, which only now exists in England and Northern Ireland. In Wales, it’s called Land Transaction Tax.

Nuts About Money tip: you can compare all the rates with our stamp duty calculator.

It’s a tax that you’ll need to pay the government (Revenue Scotland) when you purchase property. As simple as that. And the amount changes depending on the property price.

You’ll get a discount if you’re a first time buyer (never bought a home for yourself before), and charged more if you’re buying a property to rent out, or buying a second home for yourself (both called an additional property). We’ll cover these just below.

Here’s how much you’ll pay:

For Scotland, the tax free limit rises from £145,000 to £175,000 (meaning you won't pay any Land and Buildings Transaction tax on properties under £175,000).

If you’re buying a buy-to-let property, or another home for yourself (e.g. a second home), and it's under £145,000 the higher rate will apply. It’s 8% more.

This is technically called ‘Additional Dwelling Supplement’ (ADS).

It will only apply if the property is worth more than £40,000.

You won’t pay the higher rate when moving home, it’s only if you’re buying an additional property such as a second home or a buy-to-let property.

Your ‘main residence’, or your main home, will have the standard rate if you’re buying and moving into a new property.

If you temporarily have two homes, for instance buying a new home, but still have your existing property while it’s up for sale, you would have to pay the higher rate, and then apply for a refund when your existing property is sold – leaving you with one main residence.

You have 36 months to sell your existing property, from the date that you purchased your new home. To get the refund, you would fill out a form with Revenue Scotland.

Nope. You’ll pay the same rate whether you’re a resident in the UK or not. (In England and Northern Ireland you’d pay a bit more if you were a non-resident.)

You’ll have to pay LBTT when you complete on your house purchase, and will have 30 days to make the payment.

Your solicitor or conveyancer (a property solicitor) will handle everything for you.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Check out Tembo, they'll find you the best mortgage deal (from 1,000s) and have award-winning service.