Find your mortgage loan-to-value (LTV) in seconds.

Compare all the top mortgage deals in seconds.

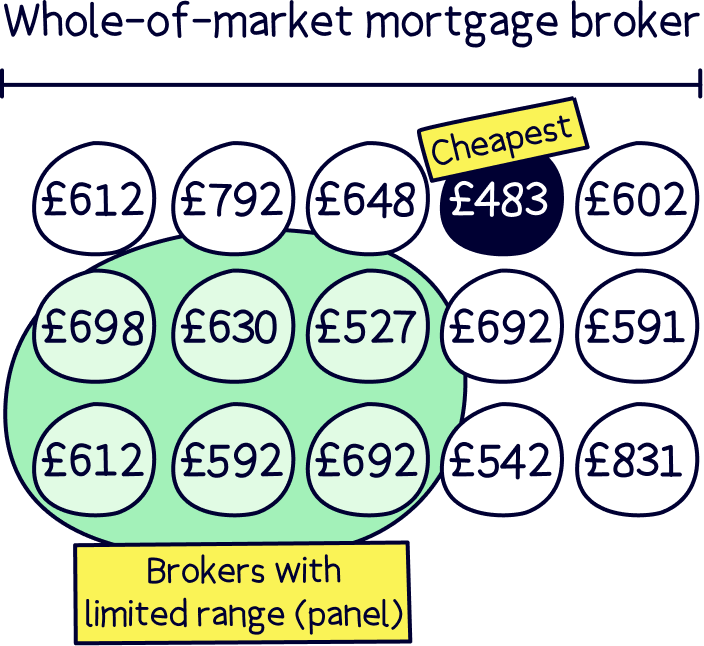

Compare mortgagesA whole-of-market mortgage broker will find the best mortgage deal for you and handle all the paperwork too.

Get 50% off

Tembo is an award-winning mortgage broker, with awesome service. They'll find your best deal, and help increase your affordability and borrow more.

Get FREE advice

Habito is an online service, it's fee-free, and the service is great. They'll help find your best deal, all in your own time.

Want more options? Here's our best mortgage brokers.

Simply enter in your property value and either your deposit if you’re buying a home (or know how much equity you have), or set your mortgage amount, and voila, the correct mortgage LTV appears. That’s it. All done. Now onto getting the mortgage! (We can help there too, check out our mortgage comparison tool.)

By the way, if you weren't sure, it’s better to have a lower LTV – we’ll run through that just below.

Nuts About Money tip: you can also use this LTV calculator for any type of loan, not just mortgages. The calculations remain the same.

How do you calculate the LTV? Good question! Simply divide the mortgage amount by the property amount and multiply by 100. So, if you have a £50,000 mortgage on a £100,000 property, you can divide 50,000 by 100,000, which is 0.5, and then multiply that by 100, giving you 50%. (It’s a bit easier to just use our mortgage LTV calculator isn’t it?)

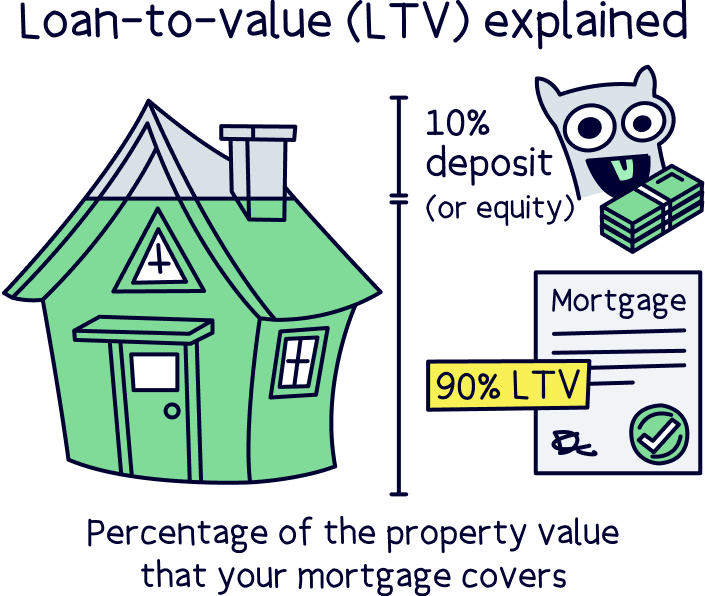

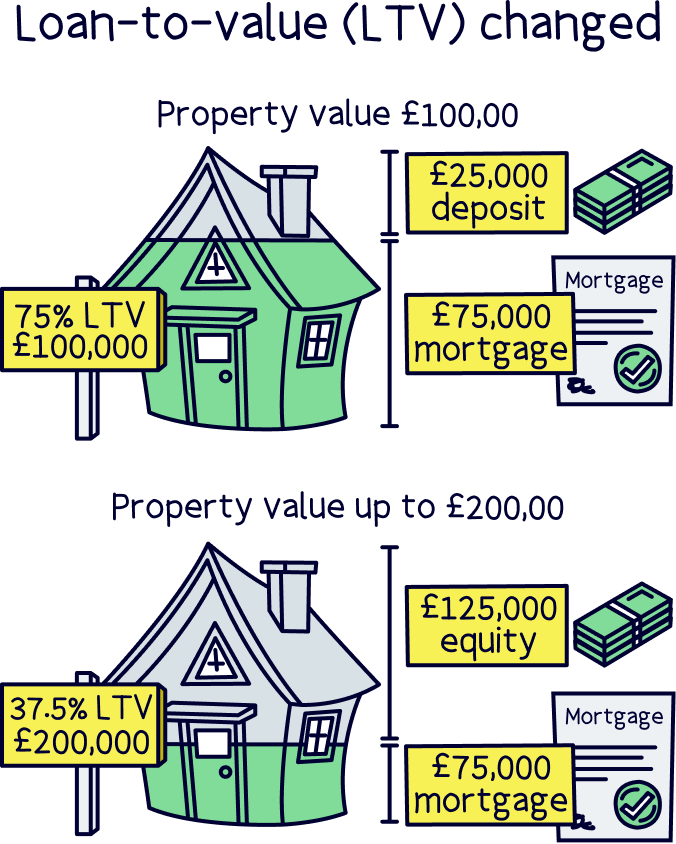

Loan-to-value, or LTV for short, is a way of measuring how much of your property is financed with a mortgage versus how much is owned by you. It’s measured as a percentage of how much of your property value the mortgage is.

So, if the mortgage covers 90% of the property value, then the LTV will also be 90%.

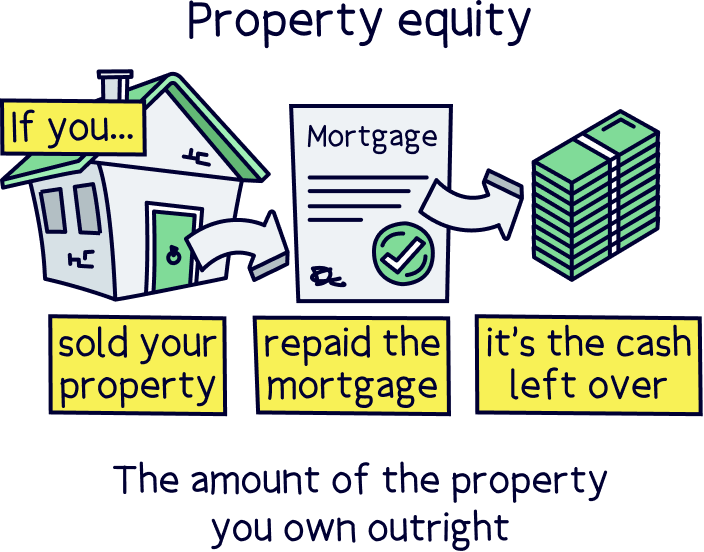

That means 10% of the property value isn’t covered by the mortgage, and therefore that 10% is all yours, called your equity. If you’re buying a property, this is also called your deposit.

Often people say ‘equity’ is how much you own of your property and the mortgage is how much the bank owns (the mortgage lender). Although technically on paper you will own all of the property yourself.

The lower your loan-to-value of your property, generally, the lower your mortgage rate will be when getting a new mortgage. This is because as the bank ‘owns’ a smaller portion of your home, there’s less risk to them of losing their money if you stop paying off your mortgage.

Why is it less risk for the lender? Well, if you do stop paying your mortgage, the bank will typically have to sell the property to get their money back. Often this is at auction and not for the best price – so they may not get all their money back if the LTV is on the higher side, but are very likely to get their money back when it’s on the lower side.

Therefore in their calculations, they are happy to lend money at a lower rate if there’s more chance they’ll get their money back if things go wrong.

To get the best mortgage rate possible for you, you want to determine which LTV bracket you fall into (explained below), and then see if there’s any room to move down into the next LTV bracket – this could be by adding money yourself, or offering a certain amount for a property you are buying. It could save you thousands of pounds over your mortgage.

To make things a bit simpler, mortgage lenders use LTV brackets to group mortgages and mortgage rates together, and these are set in 5% intervals. They range from 100%, 95%, 90% etc all the way to 60%.

Generally, if you are at 60% or below, you’re likely going to get the best rate, and this won’t change even if you have 10% or 60%.

LTV brackets round up, so if your mortgage LTV is 76%, you’ll actually be in the 80% LTV bracket. That’s why it might make sense to try to add more money yourself to get into the next LTV bracket if you are close to it – you might save a small fortune over time.

The lower the LTV the better, but that’s easier said than done! House prices are super high and it’s very difficult to get a mortgage, so it’s quite ambitious to think about those LTVs near 60%. Generally speaking, if you’re a first time buyer, you’ll likely have an LTV of 90%, and sometimes 95% (sometimes even 100%) depending on how much you are able to save for a deposit and the property itself.

Anything under 80% is generally considered ‘good’.

Don’t stress too much if it’s 95% LTV, often the main thing is getting those keys to your new home (providing you can afford the mortgage). The LTV will come down over time as the house price increases and as you pay off the mortgage.

Nuts About Money tip: here’s where to find the best 95% LTV mortgage rates and best 90% LTV mortgage rates. For other LTVs, here’s all the best mortgage rates.

Yep, LTV can change over time as your property value increases and as you pay off the mortgage. This means your equity increases, and means more money in your back pocket.

Yep. You can remortgage (get a new mortgage deal) to any LTV you like.

For instance, if you want to borrow more money for a home extension, you can ‘release’ money from your home. This will increase your mortgage amount, and the mortgage lender will give you the money as cash. This will increase the LTV of the mortgage, and typically increase your monthly repayments (and total interest) as the mortgage has increased.

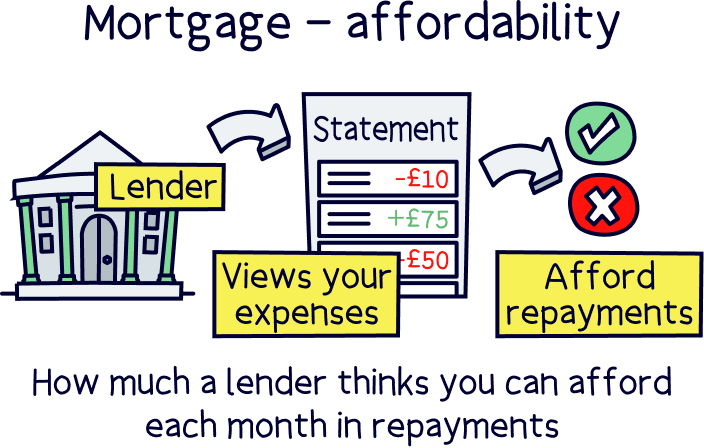

Good question! This all depends on your financial circumstances, such as how much you earn and how big your bills are. There’s a bit of maths involved, but we’ve made it all super easy with our quick and easy to use mortgage borrowing calculator.

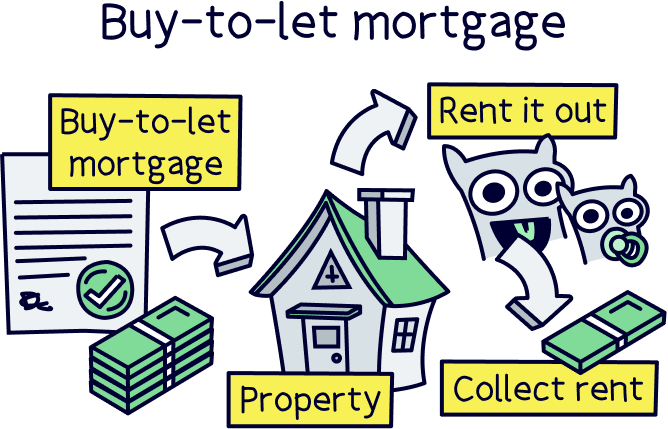

If you want to rent out a property (a buy-to-let) you typically need an LTV of at least 85%, but typically mortgage lenders will ask for 75% (so a 25% deposit). This is because buy-to-lets have a higher risk for mortgage lenders, as the property could be empty or there could be other issues (it’s not quite as simple as you living in the home yourself).

If you’re interested in buy-to-lets, here’s our guide to buy-to-let mortgages, our buy-to-let calculator, and here’s where to find the best buy-to-let mortgage rates.

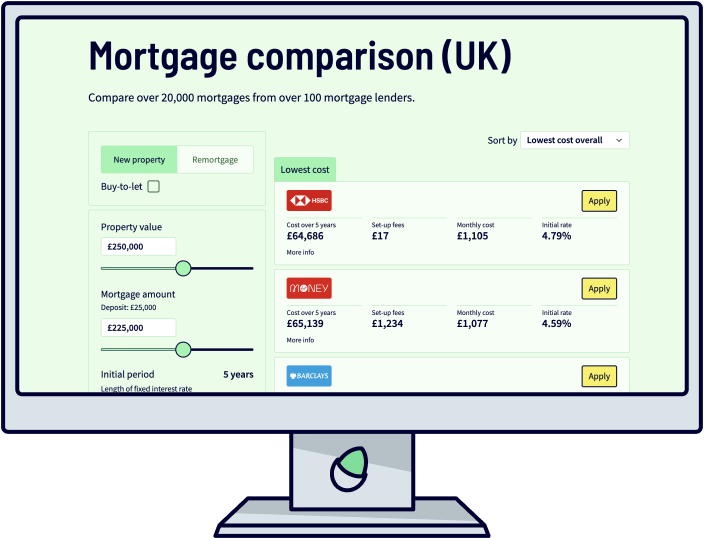

Loan-to-value is just one element of how a mortgage works and what deal you’ll ultimately get. There’s lots of mortgage lenders out there (over 100), and all have a wide range of mortgages (there’s actually over 20,000 mortgages).

You likely won’t be able to search all these yourself, but good news for you, we search almost all of them here at Nuts About Money with our mortgage comparison tool. Check it out – you can search current mortgages to find the best one for you in just a few seconds.

If you do see a mortgage you like, it’s always best to check with a mortgage broker to ensure it truly is the very best for your circumstances. The lowest rate might not necessarily be accessible to you (mortgage lenders can be picky).

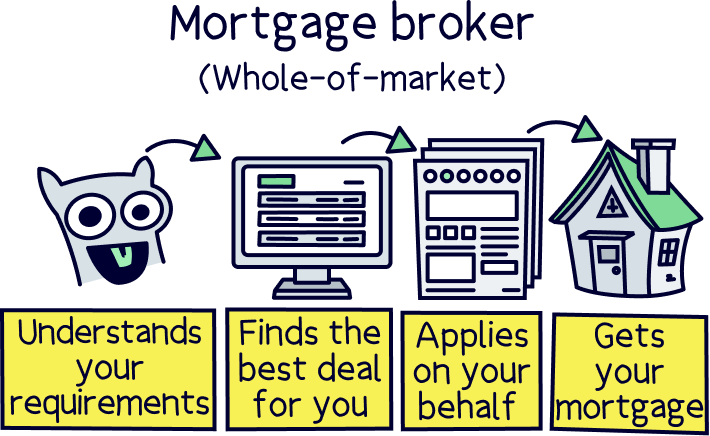

A mortgage broker can search for the best mortgage deal for you (so you don’t need to look yourself), and make sure it’s the right lender for you too. They’ll also handle the paperwork when applying and chase the lender for updates. You basically don’t need to do much at all, and can be assured you’re getting the best deal.

There’s just one thing to watch out for, and that’s to make sure the mortgage broker is a whole-of-market mortgage broker. That means they are able to search all the different mortgages out there to find the very best. If they can’t search all the deals, you can’t be sure you’re getting the very best deal for you. This could mean you end up paying much more than you should be. Some mortgage brokers are tied to certain lenders (such as if you just walk into your high street bank and speak to their advisor, they can only recommend their own mortgages).

Our top picks for mortgage brokers are Tembo¹ (get 50% off), thanks to their award-winning service and ability to borrow more than you normally could, and Habito¹ (free), who also have great service, and are fast and online. For all the top options, here’s our best mortgage brokers table.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible