Article contents

You’ve got a lot of options while in your 50s (and beyond), when it comes to mortgages. These days, there’s some great mortgage options to buy a home, or borrow more money on your existing home, which include standard mortgages to specialist interest-only mortgages (so low monthly repayments).

Over 50? You might think it'll be hard to get a mortgage but don't despair – mortgages have changed a lot in the last few years, and they’re not just for the young any more.

It can get confusing with all the different types of mortgages for over 50s, as there’s things like ‘retirement interest-only’ mortgages, which are different to a bog standard mortgage. We’ll cover the details of all of those below.

For now, if you’re just looking for a mortgage, and you’re over 50, our best advice is to speak to a mortgage broker who’s happy to help those over 50 (not too common), and has the expertise to boot. We’ve done the research, and the options are below…

Nuts About Money tip: get an idea of monthly mortgage repayments by comparing current mortgage rates with our mortgage comparison table.

Tembo is an award-winning mortgage broker with outstanding service, who not only offers ‘normal’ mortgages, but also works with a range of ‘specialist’ mortgages – things like mortgages for the older generations and borrowing into retirement.

Tembo are experts in mortgages for over 50s. They’ll find the best deal and even apply for it on your behalf.

Get 50% off the standard fee

Tembo is an all-round amazing mortgage broker, in fact, they're award-winning, and not just online.

They can help with pretty much every mortgage out there, from buying a home to switching deals, and on top of that, have unique options to increase your borrowing such as an Income Boost¹ and Deposit Boost¹.

They'll handle the whole mortgage for you too, and the service is great.

Tembo are experts in mortgages for over 50s. They’ll find the best deal and even apply for it on your behalf.

Habito will find the best mortgage for you, all for free, and with great service. But better than that, if you’re buying a home, they’ll handle the whole process for you – that’s the legal work and survey, and everything else. It’s a huge stress and time saver, and comes at a great price.

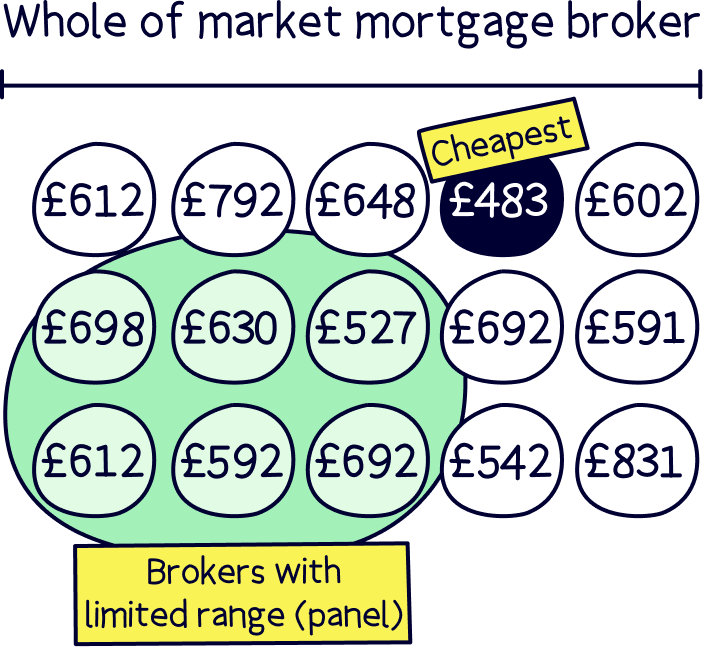

Unbiased help you find the right mortgage broker for you from your local area. Their advisors are all rated 5*, fully qualified and search the whole-market (every mortgage deal).

Tembo are experts in mortgages for over 50s. They’ll find the best deal and even apply for it on your behalf.

With all that wisdom and experience, you’d think you’d easily be able to get a mortgage right? Unfortunately, who you are, and how sensible you are with your money, has little to do with being able to get a mortgage.

Mortgage providers (companies) mostly just look at one thing, and that’s how long you can keep paying your mortgage for – or more specifically, how likely you are still going to have money coming into your bank account from a job (or via self-employment).

So, that means they often put a hard stop at your retirement age – and that used to be quite low in the past, as it was fairly rare for people to be working in their mid-to-late 60s and 70s (how lucky they were).

Note: we’re talking about standard mortgages, but there’s now more options after retirement – we’ll cover those below.

These days, we typically live longer on average, although not quite as wealthy, so it’s very common for people to still be working later in life, or to be at least expecting to work later in life.

And that's good news for those older borrowers looking for mortgages. ‘Normal’ mortgages come down to the year you think you’ll retire – and you can set that to up to 70 (and sometimes later), which means you can potentially get a standard mortgage until well, 70 (that’s when the mortgage should end (the final payment)).

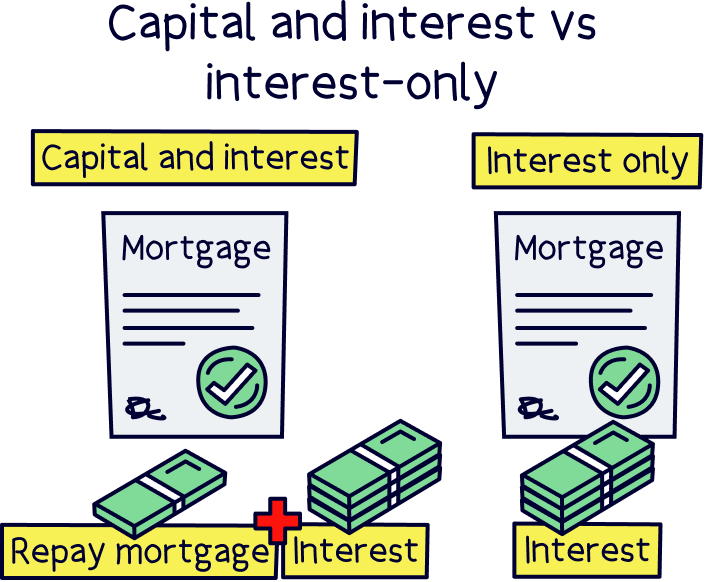

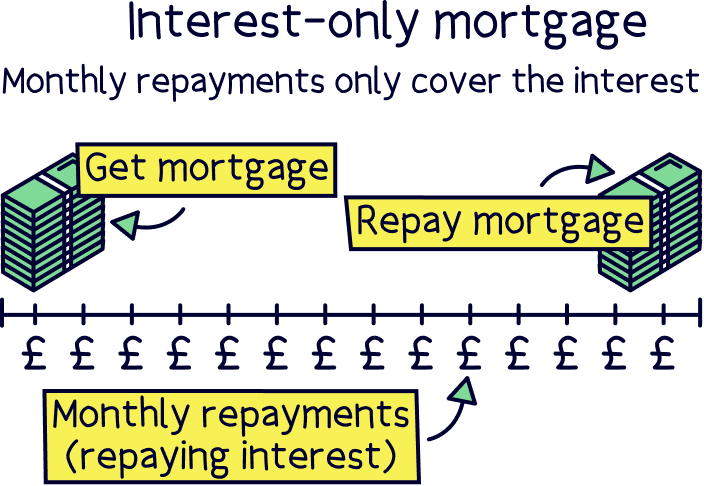

Note: a standard mortgage is where you pay off both the mortgage and interest each month (also called a capital repayment mortgage), but you can also get standard mortgages that just pay off the interest each month, called an interest-only mortgage (often used for buy-to-let mortgages), but common in retirement too.

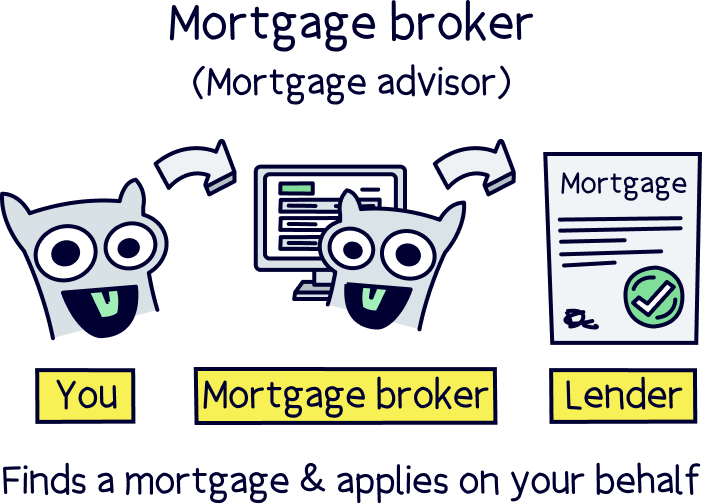

If you’re keen to get started, it’s best to speak to a mortgage broker, they’ll be able to find the best mortgage lender (company) for you and your individual circumstances, and will be able to get the best mortgage deal too (you might save £1,000s)...

Our top pick for mortgages in later life is Tembo¹, and they’ve also got award-winning customer service (and you’ll get 50% off with Nuts About Money). Want a few options? View all our recommended mortgage brokers.

If you know you’re getting a reasonable pension when you retire, that can afford the mortgage payments, you might also be able to get a mortgage that finishes after your retirement age, potentially up to 85 years old.

This comes down to the individual lender, and you’ll need proof of your pension income – so again, it’s best to use a mortgage broker who knows all the ins-and-outs to make sure you have the best chance of getting the mortgage.

Tip: To find out how much your pension will be, we've got a handy pension calculator.

There’s also some alternative mortgages that are suited to those in retirement (we’ll cover them just below).

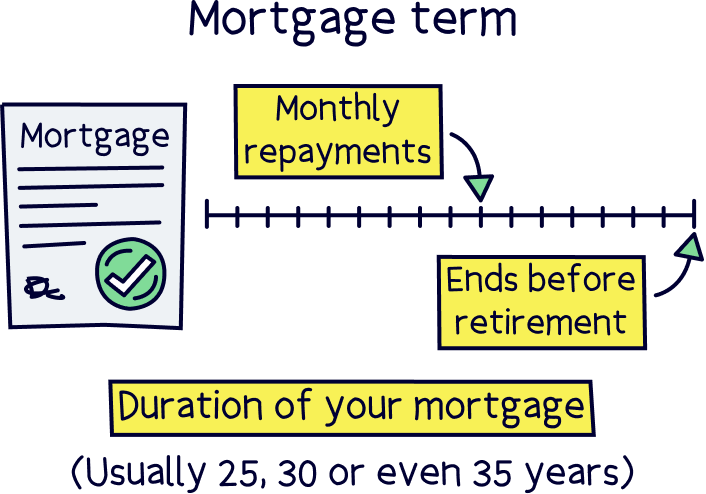

As we mentioned, most mortgage providers will only give you a regular mortgage (often called a standard mortgage) until the age that you retire, or up to 70, and that means, as you’re in your 50s, you’ll have to opt for a shorter mortgage term – that’s the amount of time the whole mortgage is for…

Typically mortgage terms for new mortgages were 25 years, and these days, as house prices are pretty crazy, younger people are able to borrow for up to 40 years.

The longer the term, the lower the monthly payments are. So, with a shorter mortgage term, the higher the monthly payments will be – which can cause some problems if you’re taking out a new mortgage in your 50s.

If you’re just 50, you might be able to get a 20 year mortgage term with some lenders. And if you’re nearing 60, you might only be able to get a mortgage for 10 more years – which can be far bigger monthly payments.

However, your monthly mortgage payments will also depend on how much you’d like to borrow…

Find out how much your monthly repayments will be with our mortgage repayment calculator.

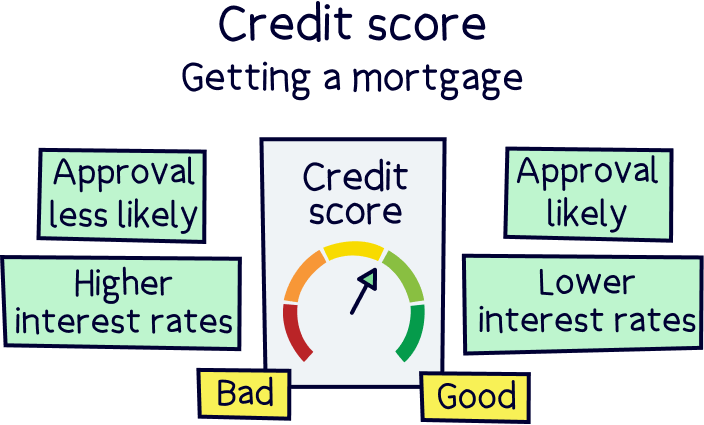

Note: As you're over 50 you’ll likely need a good credit score to prove you are able to make mortgage repayments (and other payments) on time (your credit history).

Right, the important question right? How much can you actually borrow with a mortgage?

It all comes down to your income, and that’s things like your salary, and any other money you might have coming in regularly. For most people, it’s just their salary.

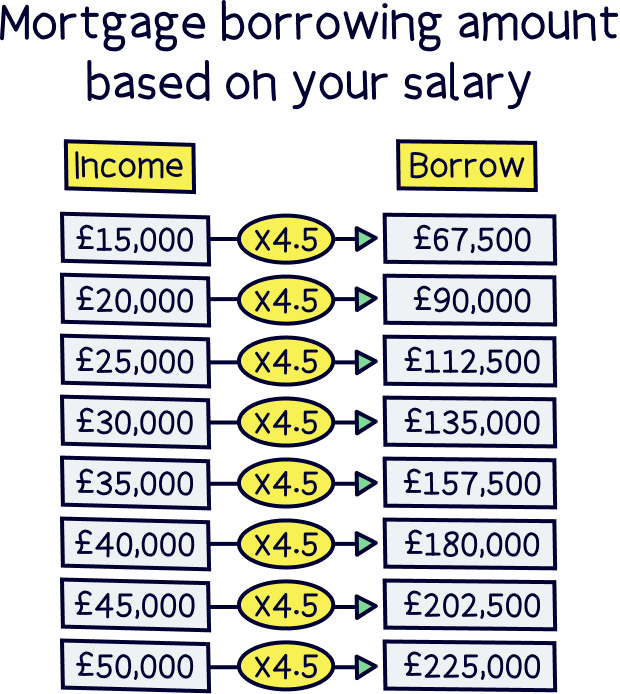

As a general rule, you can borrow around 4.5x your income. So, with a £50,000 salary, you can borrow up to £225,000.

However, the actual amount will vary depending on your personal circumstances. The mortgage lender will look at how much you’re paying out each month on things like bills, loans and rent (your total outgoings) – which is to make sure you can afford the monthly repayments.

The monthly repayments themselves can change depending on how long the mortgage will be for, so there is some flexibility in your 50s, for instance, you might be able to opt for a 20 year mortgage and get lower monthly repayments.

To find out how much your monthly payments are likely to be, and how much you can borrow, it’s best to use a mortgage broker, such as Tembo¹, who’ve got friendly experts to run through your options, or for a rough guide, use our Nuts About Money mortgage repayment calculator.

If you’re self-employed, don’t fret. You can still use your self-employed income to get a mortgage – it’s a bit different to a salary from a full-time job, but you should be able to use the last 2 years income as evidence you have a stable income.

If you’re just newly self-employed, you might struggle, so it can be best to wait a bit longer, but you never know – speak to a mortgage broker to see what they can do.

Mortgage lenders will also need to know your income is going to continue into the future, which could be from a pension in the future (called a pension forecast).

Tip: To make sure you have enough money for the mortgage we've got a take-home pay calculator.

If you think you likely won’t get a regular mortgage, or won’t be able to afford it (perhaps you are nearing 60, or in your 60s and planning to retire soon), there are still options available. Let’s run through some of the more common options.

A long-term fixed rate mortgage is where the interest rate on your mortgage is set for the whole mortgage, which can be for as much as 40 years – and you can borrow up to 6x your income.

With these, there’s no maximum age limit, so you can often borrow into retirement, and you can even apply for a mortgage up to 80 years old.

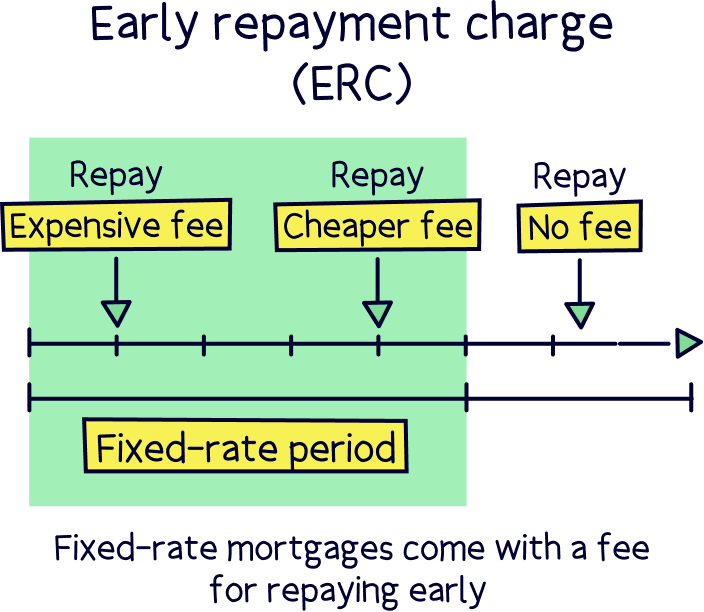

Typically, you’ll be able to change your mortgage deal after 5 years if you’d like to (for instance if interest rates are lower). And, you can even move out and rent the property (after 1 year), and there often won’t be any fees to repay the mortgage off once you’d had it for 5 years (called early repayment charges (ERCs)).

Note: you can’t currently use these mortgages in Scotland or Northern Ireland, or if the building is over 5 storeys (e.g. a large block of flats).

Retirement interest-only mortgages (RIO mortgages), are designed for people who want to borrow money after retirement, and who already own a home (often without a mortgage currently, but not necessarily).

You can borrow money for a whole range of things, such as travelling, home extensions and improvements, and even helping your family get on the property ladder themselves.

You’ll get the mortgage amount (the loan), and pay interest each month, and traditionally you won’t pay back any of the actual loan – which means lower monthly payments, so much more affordable for those living on a pension income.

The downside is that you’ll be paying interest each month when you otherwise wouldn’t be (without a mortgage), and it doesn’t go towards paying the mortgage off – the mortgage amount doesn’t reduce (normally). The interest rates are often higher than other interest-only options too.

The loan will then be repaid if the home is sold, or if you move into long-term care, or pass away (sorry to put a downer on things).

There is some flexibility however, and if you want to, you can repay some of the loan in order to reduce it, and possibly even pay it off – so your home doesn’t need to be sold to repay the loan later on.

You’ll often only be able to get an RIO mortgage if you’re over 55, although some lenders have a much higher minimum age.

An enhanced interest-only mortgage is where you borrow up to 7x your income (e.g. your pension), as you’ll only pay back the interest each month (so low monthly repayments).

You’ll choose how long the mortgage is for, and will have to have a plan to pay back the mortgage when the mortgage term ends (e.g. from savings, investments or a pension) – so different to retirement interest-only mortgages, which don’t have a repayment date, they last until the home is sold (e.g. when you pass away).

The maximum age the mortgage terms can go up to is 80 years old.

You can use these mortgages for a variety of reasons, such as travelling, and helping family members, but you can also use them to buy a home too (as long as it’s over £30,000). And even remortgage (which is switching your current mortgage for another one).

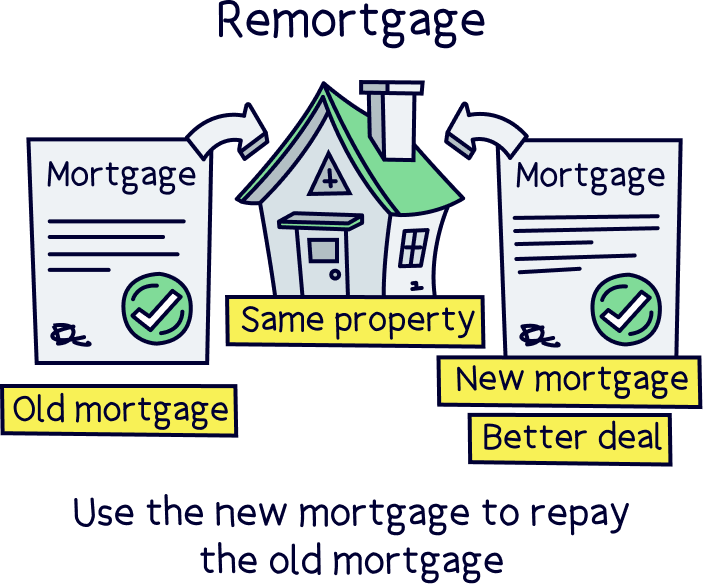

If you’ve already got a mortgage, you can typically switch to another mortgage, which is called remortgaging – well, you simply pay off your current mortgage and take out a new mortgage technically, but it all happens in one go.

So, if you’ve got a standard mortgage (where you’re paying it off each month), but you’re planning ahead and want to borrow money into retirement, or for a bit longer than you are now, or maybe want lower monthly repayments – you might be able to switch to a mortgage designed for the over 50s, such as all of those options above (and even more).

To find the best deal, we recommend using a mortgage broker – and we’ll cover why just below.

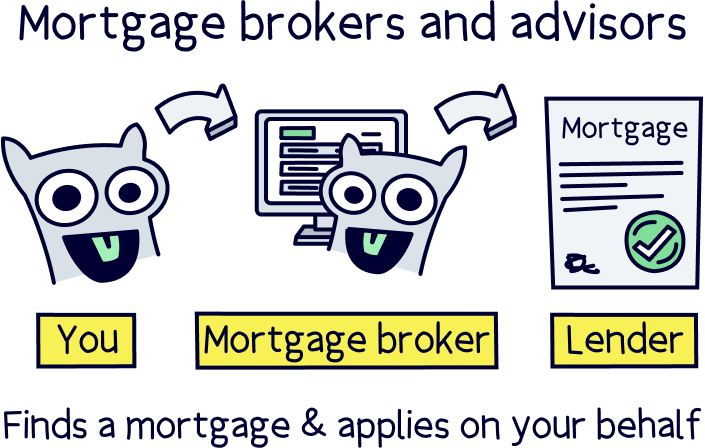

We’ve banged on about it a bit, but let’s just highlight the point again – it’s often best to use a mortgage broker to find the best mortgage for you, and there’s a lot of options that are all quite complicated.

And, for each different type of mortgage, there’s lots of different mortgage lenders, charging different fees and interest rates – meaning the difference between a good deal and a bad deal can potentially be £100s per month.

A mortgage broker will get to know your individual circumstances and what mortgage would be best for you, and then go off and search all the different mortgage lenders to find the best deal for you. And, they’ll even handle all the paperwork (mortgage application) for you too.

You can simply put your feet up, knowing an expert is sorting everything, and that you’ll be getting the best deal out there.

Trying to do it yourself could end up costing you a lot more in the long run by ending up on the wrong mortgage – however you can get a rough idea of costs with our mortgage comparison table.

Not sure what mortgage broker to use? Here’s our recommended mortgage brokers.

You might have heard of equity release, and they are similar to retirement mortgages, or mortgages for over 50s, however they’re suited to people who own their own home already, often outright without a mortgage, and want to borrow fairly large sums of money – which can represent a large part of the property value.

You’ll still be able to live in the property of course – but will lose the home when you pass away or move into long-term care, and at which point the home will be sold to recover the loan amount.

There’s 2 types of equity release options, lifetime mortgages and home reversion plans…

A lifetime mortgage is where you’ll borrow money while still owning the property, and can either make repayments each month, or none at all, and let the interest be added to the loan amount.

A home reversion plan is where you sell part of your home in return for a lump sum or even regular payments. You’ll still own the portion you don’t sell, which can go up in value.

Equity release is very complicated, and there are lots of finer details to assess, with not all in your benefit (for instance not getting the current value of your home if using a home version plan) – so it’s a great idea to speak to a financial advisor to run through your options.

Surprisingly, there's lots of great options when you're over 50 – you can still get a mortgage and borrow money, and for a variety of reasons, such as going on a grand travel adventure, or helping your kids or family with their finances, or buying their first home.

There’s lots of mortgage options for over 50s, and even 60s, 70s and even at 80. We’ve outlined the main ones, which are:

It’s a great idea to speak to a mortgage broker (an expert in mortgages), who can determine the right type of mortgage for you, and the right mortgage lender to get the best deal – the difference really can be large, and the advice can potentially save you £1,000s per year. Again, here's our recommended mortgage brokers for the over 50s.

And that’s all there is to over 50s mortgages. All the best for a happy retirement.

Tembo are experts in mortgages for over 50s. They’ll find the best deal and even apply for it on your behalf.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things mortgages, with years of combined experience working in the mortgage industry, and some of our team are qualified mortgage advisors. We understand the ins and outs of mortgages, how to communicate mortgages in an easy to understand way (we hope you agree), and of course, how to get the best mortgage deal for you.

More than 20 years of combined experience researching and writing about mortgages and mortgage advice

Qualified team (CeMAP - Certificate in Mortgage Advice and Practice)

A wide range of mortgage companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Tembo are experts in mortgages for over 50s. They’ll find the best deal and even apply for it on your behalf.