Article contents

The best pension drawdown provider is PensionBee. It’s easy to use, has low fees, and offers simple, easy to understand pension options suited to your retirement plans. You’ll get dedicated customer support too. If you’re looking for expert advice, check out Moneyfarm. To make your own investments, check out AJ Bell and Interactive Investor, both low cost, with a wide range of investment options.

Ready to start taking an income from your pension? All those years of hard work and saving have hopefully paid off, and you’re ready to enjoy your sunset years.

Although there’s just one final thing to decide right? Where’s the best place to keep your pension? Well, you’re in the right place. We’ve reviewed all the best options, and narrowed it down to the very best pension drawdown providers.

So, without further ado, here they are:

We recommend PensionBee, it’s easy to set up and use, low cost, with simple, easy to understand drawdown options.

Get £50 added to your pension

PensionBee is our recommended provider – they’ve thought of everything.

Their 5 star rated app (and website) makes it easy to set up and use. You can open a brand new pension, or transfer your existing pensions across (they’ll handle all the paperwork).

Simply pick from an easy to understand range of pension plans, and that’s it, the experts manage everything from there.

It’s low cost, with one simple annual fee. The customer service is excellent, and you’ll get a dedicated account manager for any questions you might have.

And, when the time comes to retire, withdrawing from your pension is easy too.

You can also use them if you're self-employed or a company director.

Moneyfarm is a great option for saving and investing (both ISAs and pensions). It's easy to use and their experts can help you with any questions or guidance you need.

They have one of the top performing investment records, and great socially responsible investing options too. Plus, you can save cash and get a high interest rate.

The fees are low, and reduce as you save more. Plus, the customer service is outstanding.

We recommend PensionBee, it’s easy to set up and use, low cost, with simple, easy to understand drawdown options.

AJ Bell is well established, with a good reputation.

It's one of the cheapest SIPPs out there (charging a low annual fee).

There's a huge range of investment options – pretty much every investment out there (including both funds and shares).

The customer service is excellent too.

Overall, it's one of the best options for a SIPP.

Get £100 - £3,000 cashback

Interactive Investor is a well established company, and very popular.

Instead of paying a percentage of the investments in your account (like other investment companies), you’ll instead pay a fixed fee per month – and it’s pretty low, starting at just £5.99 per month for a pension (SIPP).

This makes it one of the cheapest SIPP providers out there, especially if you have a fairly sizeable amount within your pension (e.g. over £30,000).

On top of that, there’s a huge range of investment options (e.g. shares and funds) – one of the largest.

It's easy to use, and the website and app are great. The customer service is excellent too.

A great choice overall.

We recommend PensionBee, it’s easy to set up and use, low cost, with simple, easy to understand drawdown options.

If you're a bit unsure about pensions and would prefer to speak to an expert, check out Unbiased¹ – it's a free service to find pension experts (financial advisors) in your local area.

Saving for your retirement is very important, as we’re sure you know! And, withdrawing from your pension is just as important too, if not more so – there’s lots to think about (we’ll cover that below), and of course, there's a wide range of pension providers to choose from.

We’ve narrowed it down to the very best pension providers for pension drawdown. Here’s the criteria we’ve looked at:

There’s actually a good range of drawdown pension providers, although not quite as many as general pension providers (pension companies), and not all of them offer pension drawdown.

Our recommendations (above) are ones we've recommended to our friends and family, and lovely readers of course.

So, whichever provider (from our recommendations) you opt for, you can be confident you’re using one of the very best in the UK.

Before we rush into all the nitty gritty details (we know pensions can be ever so slightly boring), let’s run through how to set up a drawdown pension. It couldn’t be simpler:

1. Decide if you’d like the experts to manage your investments, or make them yourself

2. Pick the best pension drawdown provider for you

3. Pick the right drawdown pension plan for you – using simple Investment Pathways options, or your own choice (explained below)

4. Transfer your existing pension across (it’s super easy)

5. Retire!

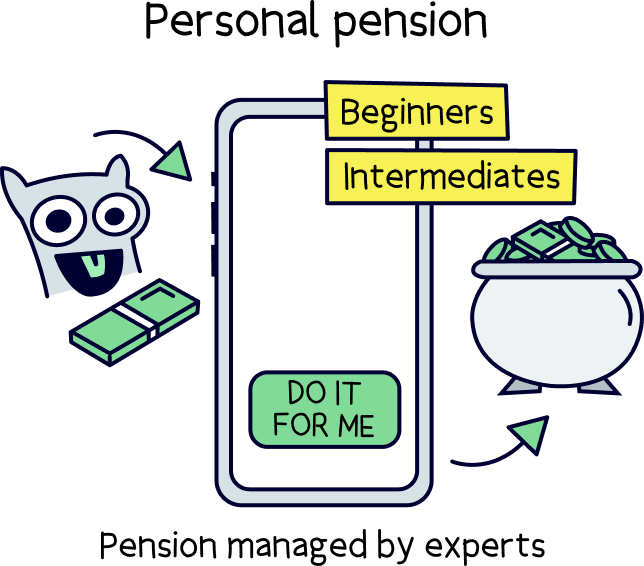

You first need to decide if you want the experts to handle things, or if you want to make your own investment decisions.

We recommend letting the experts handle things, unless you know what you’re doing when it comes to investing – the experts are highly experienced, and know how to grow your pension sensibly over time.

If you’re not quite sure, here’s a run through of both options:

This means the experts manage all of your investments, you just pick from a small range of pension plans suited to retirement goals (in this case, pension drawdown). There’s help on hand if you need it too.

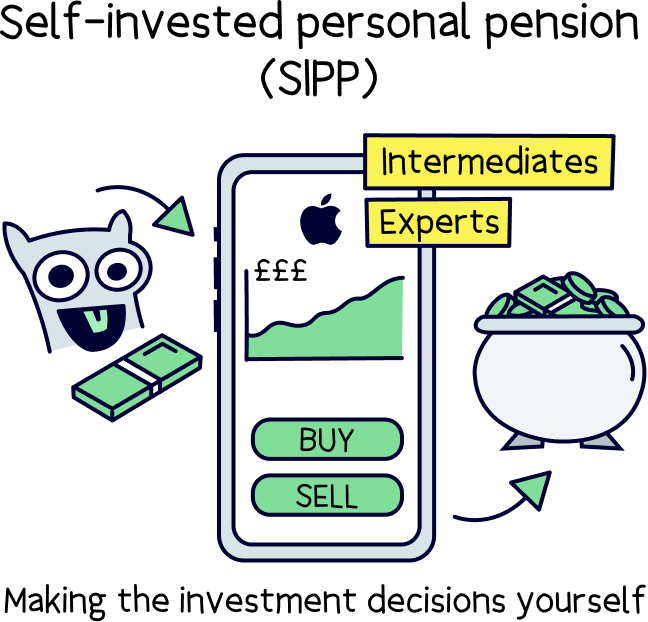

A self-invested personal pension (SIPP) is where you make all the investment decisions – so that’s typically which investment funds (or pension funds) to buy and sell (a fund is a group of investments), or which stocks and shares to buy too (if you want to).

After that, pick your favourite drawdown pension provider.

As a recap, our top recommended expert-managed drawdown provider is PensionBee¹ (closely followed by Moneyfarm¹). They’re both easy to use, have low fees, and have simple, easy to understand pension plans. Plus, great customer service.

If you’re making your own investments, we recommend AJ Bell¹ (followed by Interactive Investor¹). They’re both very low cost, and have a huge range of investment options.

Here’s the full range of the best SIPP providers, if you’d like to see all the top options.

Here’s where things can be a bit more complicated, and that’s why the government has introduced a simple way of making your own decision when it comes to drawdown pension plan options – it’s called Investment Pathways…

Note: just so you know, you can always change your mind later on. A great benefit of flexible drawdown pensions.

To make pension drawdowns a bit clearer, and to help you make the right decision for yourself, the Government has come up with 4 common options, called Investment Pathways:

These options should suit most people, and it gives pension providers the ability to match their drawdown pension plans with each option – making it simple for you to match yourself with the right drawdown pension plan for you.

For example, if you look at PensionBee¹, our top recommended provider, they’ve matched their plans to each option, which we’ll run through quickly now:

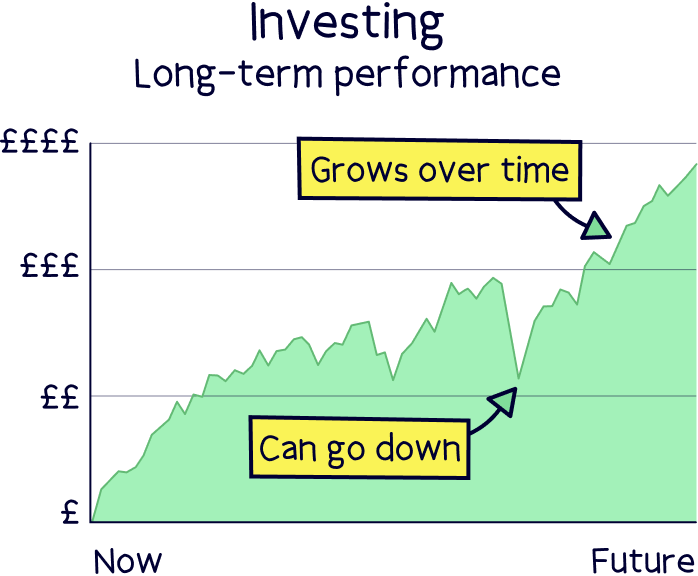

If you’re not sure about the details, ‘equities’ means investments in stocks and shares, which typically grow much more over time, but the value of your pension can go 'up and down' along the way.

Whereas ‘fixed income’ means loaning money to governments and large corporations in return for interest payments – these are often called bonds, and typically seen as more stable investments.

Most drawdown pension providers should offer these options to you in order for you to pick the right pension plan for you (the pension fund investment).

Even self-invested personal pensions should offer this. You don’t have to pick any of the recommended investment options, you can still make your own investment decisions.

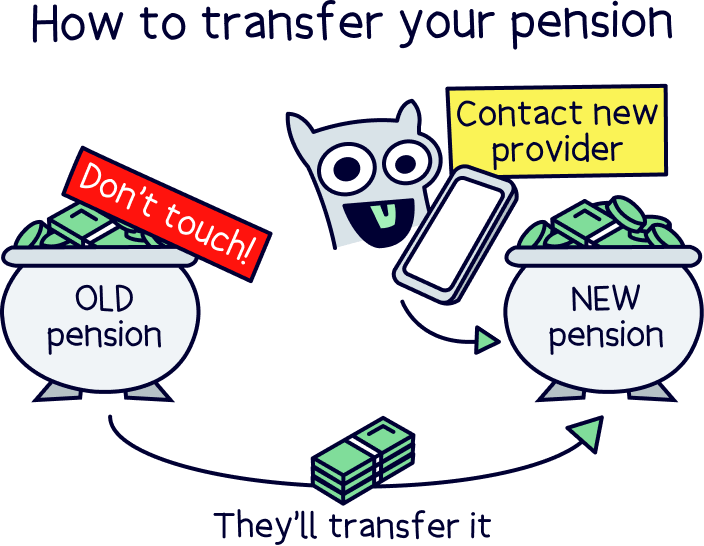

Once you’re happy with your pension provider decision, and the pension plan you’d like (or if you’re making your own investments, simply the range of investment options on offer), all that’s left to do is to transfer your pension(s) across.

This couldn’t be easier too – if you pick one of our recommended options, your new pension provider will handle everything for you. That’s all the paperwork, and all the communication with your existing provider.

All you need to do is let them know who your old provider is. If you’re not sure, and you have an old workplace pension (a pension set up by your old employer), your old HR department should let you know. Or, you can try the Government’s pension tracing service.

After that, your money should be moved across after a few weeks (or sometimes months).

You’ll normally be guided through the whole process by the customer support team, and they’ll keep you up to date with the transfer progress. With PensionBee¹, you’ll have your own dedicated account manager.

Ahhh, retirement. Finally. It’s time to put your feet up.

Well, there is one last thing, and that’s to decide how much income you’d like to take out of your pension pot, and when. And that’s all down to you.

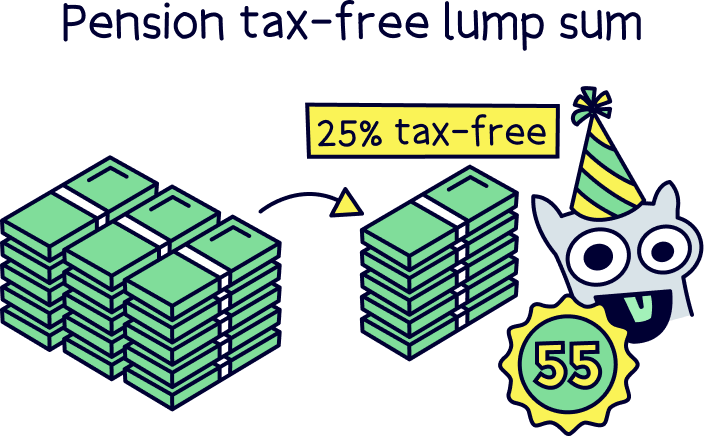

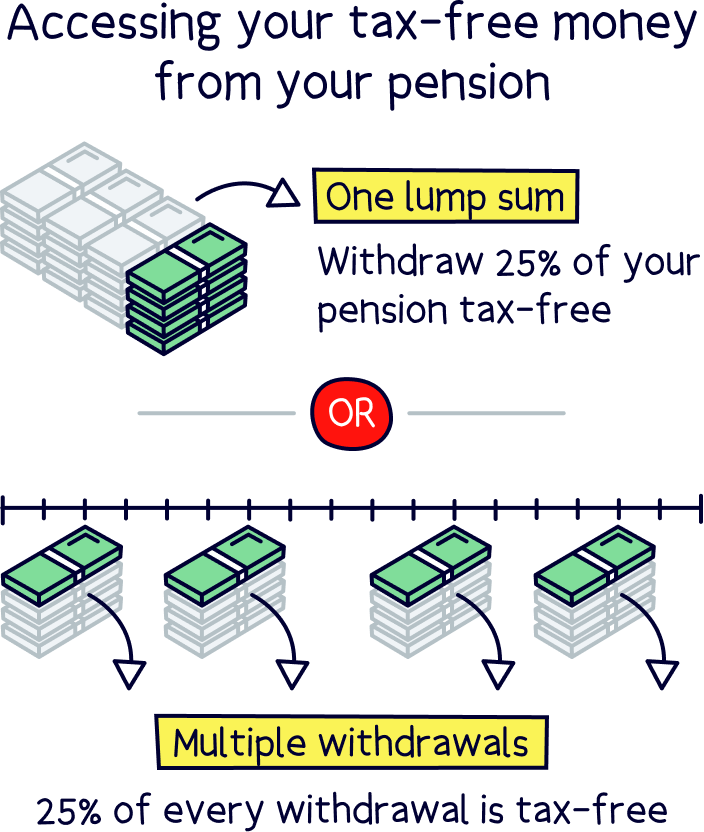

You can take 25% completely tax-free, and with the rest, you’ll pay Income Tax on it. (We’ll cover the details about drawdown pensions below.)

Simply let your new pension provider know what you want to do – which can all be done online (or via the phone app), if you’re using one of our recommended providers that is.

They’ll also handle all the Income Tax payments too – you don’t need to do a thing.

The great thing about the very best pension drawdown providers, is that the fees typically don’t change from when you were building up your pension savings in the first place. There’s not typically a drawdown fee, or anything like that.

So our recommendations make up a fair proportion of our best pension providers, as well as the cheapest pension drawdown providers too.

So, for the experts to handle your investments (money), PensionBee¹ comes out on top, where fees range from 0.50% to 0.95% depending on the plan (and reduce by 50% if you have more than £100,000 saved). Closely followed by Moneyfarm¹ (who also provide expert advice).

To make your own investments, AJ Bell¹ is low cost (an annual fee of 0.25% per year, which reduces if you have more saved, and low dealing fees (fees to buy investments) for pension funds (£1.50).

They sit alongside Interactive Investor¹, who have a flat monthly fee (£12.99), plus dealing fees, which can make it cheaper for large pension pots (also called investment portfolios) – we're talking over £60,000 for a pension.

Let’s make sure we’re all on the same page when it comes to pension drawdown.

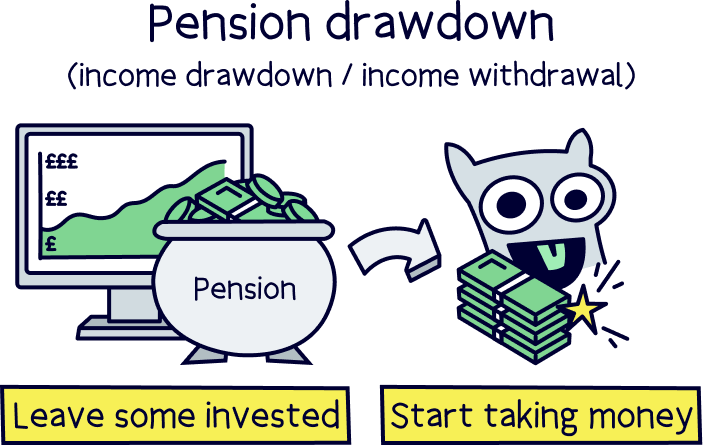

Pension drawdown is where you start taking money from your pension (retirement savings), also known as income drawdown, or income withdrawal, but you still leave some of your pension invested, so it can hopefully keep growing over time.

You can start withdrawing money from age 55 (57 from 2028).

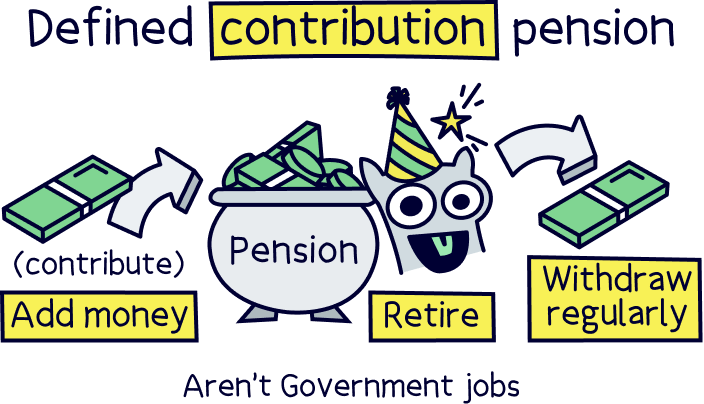

It only applies to defined contribution pension schemes, which are pensions you pay into (contribute) over your working life, that build up your pension pot (pension savings) over time.

You decide what pension provider to use, and when to withdraw it.

These are the most common types of pension, and include all personal pensions (pensions that you set up yourself, rather than a workplace pension, set up by your employer).

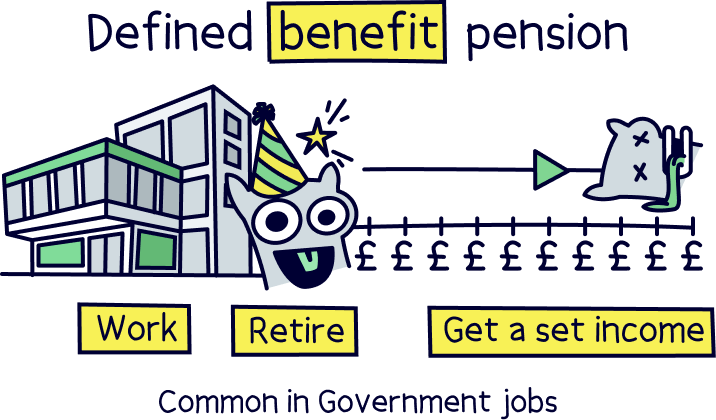

The alternative is a defined benefit pension scheme, which are typical in government workplaces, such as the NHS, and are where you get a set income when you retire, direct from the pension scheme – and it depends on things such as how long you’ve worked there and your salary. This can be called a 'final salary pension'.

Pension drawdown has become very popular since 2015, when it became allowed to withdraw money from pensions at age 55 (which will be rising to 57 in 2028), meaning more control over your own pension. Known as the ‘pension freedom rules’.

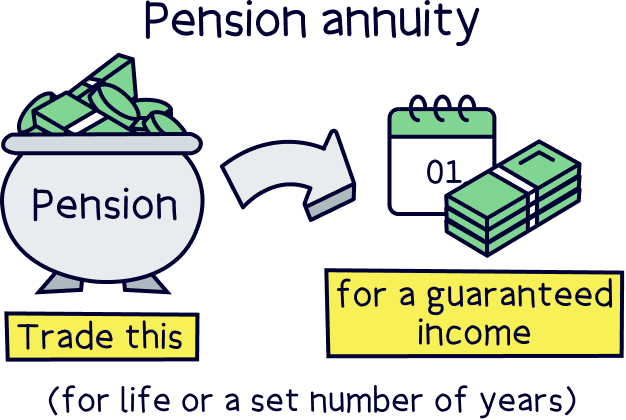

Before that, most people bought a pension annuity with their pension pot when they retired. An annuity provides a guaranteed income for the rest of your life (or a set number of years). You trade your pension pot for the future guaranteed income.

You can still do this, and it is popular. Plus you now don’t have to use your whole pension pot to buy an annuity, you can use a part of your pension pot to buy one, and withdraw cash from your remaining pension pot (drawdown), as and when you like, too.

Nuts About Money tip: learn more about pension annuities and drawdown with our guide drawdown vs annuity.

One of the great things about pensions is the great tax-free benefits – there’s no tax to pay as your money grows (a great reason to keep your money in a pension).

When you want to withdraw some, or all of your money, the first 25% will be completely tax-free. This can be withdrawn as a tax-free lump sum if you want it.

Note: there is a maximum of £268,275 you can take out tax-free.

With the remaining pension pot (the 75%), you’ll have to pay Income Tax on, just like a salary, and how much you pay depends on your total income at the time. Here’s the current tax bands:

Best of all, with pension drawdown, you don’t need to worry about paying tax yourself, your pension provider will handle it all for you.

If you are employed, the tax is taken in the same way, it's all automatic. Technically it’s called PAYE (Pay As You Earn).

You might find that the first payment from your pension is taxed at a higher rate (called emergency tax).

This is because your pension provider won’t know the right tax code for you until after a payment is made, and they can get the right code for you from HMRC (the tax people – officially called HM Revenue & Customs).

This will typically resolve itself with the second payment, as the provider will know the right code for you – and they’ll be able to take less tax over the year to refund the overpayment you’ve made with the first payment (the emergency tax).

You can also claim the tax back directly from HMRC – which you’ll need to do if you take the whole pension pot at once (as there’s no further payments to offset).

The pension commencement lump sum (PCLS), is simply the official name for the 25% tax-free lump sum you can take from your pension pot.

When it comes to pensions, there’s lots of complicated terms unfortunately. If you haven’t accessed any of your cash yet, then your money is technically ‘uncrystallised’, and if you’re over 75 and haven’t accessed your cash yet, it’s called ‘unused’ – you can still access the money whenever you like.

By the way, there used to be a ‘lifetime allowance’, which was the most you could save into a pension to still get all the great tax benefits, which was £1,073,100. If you withdrew more money than this, you’d pay a massive 55% tax.

This has been scrapped now, so you can save more (if you’re rich), and withdraw as much as you like, and you’ll be taxed at the same rate as Income Tax (tax rates above).

However, the maximum limit of taking out 25% of your cash tax-free still remains. Confusing right?

So, you can only take out 25% of the previous lifetime allowance tax free (£1,073,100), which is £268,275 – so anything above this, you’ll pay tax on, even if you have more than £1,073,100 in your pension.

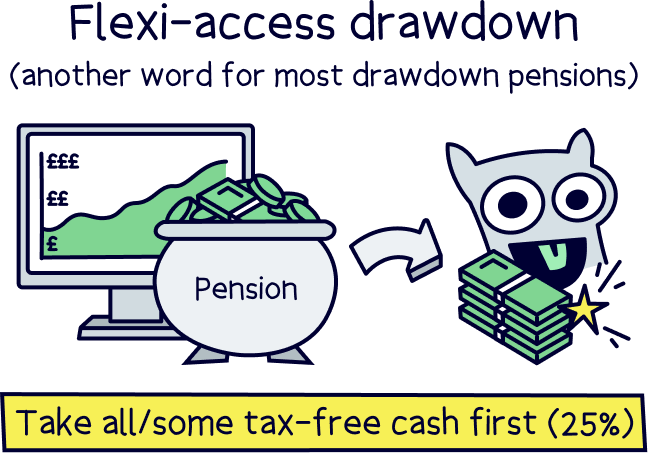

Flexi-access drawdown is just another word for most drawdown pensions – where you have a flexible income in retirement.

You decide how much you want to withdraw from your pension pot, and when you want to withdraw it, as long as you’re over 55.

Typically, with a flexi-access drawdown pension, you would take either all, or some of the 25% tax-free cash first. Then pay tax on the remaining 75% later down the line when you take it out – this money is kept within the flexi-access pension.

The money you haven't taken out will remain invested and hopefully keep growing over time.

The uncrystallised funds pension lump sum (UFPLS) is a different way of taking your money out of your pension (not a drawdown pension).

Instead of a drawdown pension, you would withdraw all of your pension, or lump sums, and with each withdrawal, 25% of the cash would be tax-free, and 75% of it would be liable for Income Tax.

Note: your pension wouldn’t be moved to ‘drawdown’ and can stay where it is, but it does trigger the money purchase annual allowance (covered below), reducing your future pension contributions to a maximum of £10,000 per year. You also need to be over 55.

When you start taking money out of your pension, this triggers the ‘money purchase annual allowance’ (MPAA)...

This means that you can no longer add the same amount of cash into your pension as you could before, which was previously £60,000 or as much as your total income, in a tax year (April 6th to April 5th the following year).

Instead, you can only add up to £10,000 per tax year.

Yep! However, as we mentioned just above, the most you can pay into your pension, after you start withdrawing from it, is £10,000 per tax year, rather than £60,000 or your total income per year.

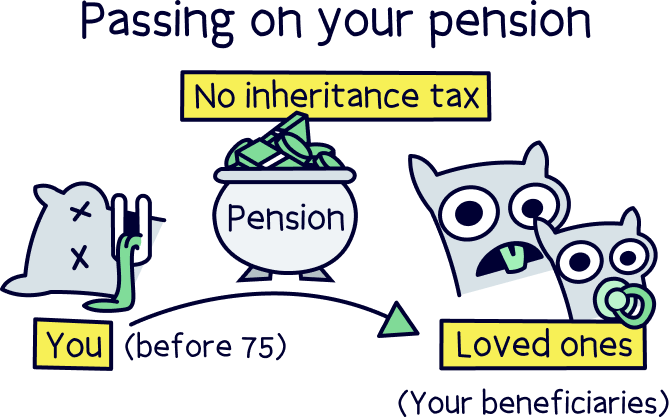

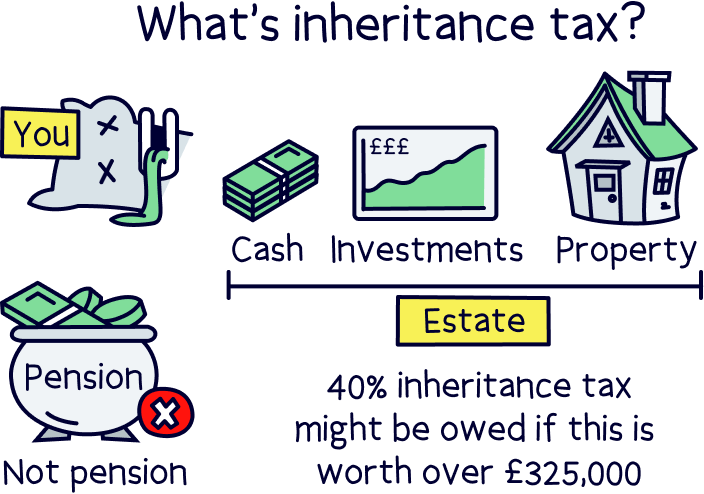

Did you know pensions are entirely separate from everything else you might own? (cash, property, shares etc). All those other things count towards your ‘estate’, which is the total of everything you own, but not pensions.

Pensons are their own separate thing, and don’t count towards any Inheritance Tax that your family might pay when you sadly pass away.

Instead, if you pass away before the age of 75, your pension can pass to your loved ones completely tax-free, and after 75, whoever receives it will pay Income Tax on it, instead of Inheritance Tax. The actual rate will depend on how much their income is at the time (tax rates are above).

However, if you’ve taken cash out of your pension, such as a 25% tax-free lump sum, this amount is no longer in your pension and will count towards Inheritance Tax.

You can also tell your pension provider who you want to receive your pension (called your ‘beneficiaries’). These people can be different from your next of kin. However, it’s not legally binding, so your pension provider doesn’t have to, should there be any legal issues.

There we have it – the best drawdown pension providers in the UK. We hope we’ve also made pension drawdown a bit easier to understand.

We recommend letting the experts handle your investments and pension drawdown, so your money can keep growing in a sensible pension plan, suited to your retirement goals. Then take money as and when you like, giving you that comfortable retirement you deserve.

Our top recommendation is PensionBee¹ – they specialise in pensions, it’s easy to use, low cost, has suitable pension plans for drawdown pensions, and you’ll get a dedicated support to help you whenever you need.

We also recommend Moneyfarm¹, it’s great too, low cost, and provides expert advice if you’d like it.

If you do want to make your own investments, and have a bit more control over your pension, we recommend AJ Bell¹ (low cost, huge range of investment options), and Interactive Investor¹ (flat monthly fee, great for large pensions). They both offer great drawdown pension options, and excellent support if you need it.

If you’re still a bit unsure, don’t worry. If you’re over 50, you can get free advice about your pension with Pension Wise, a service from MoneyHelper, which is a government scheme.

You could also speak to a financial advisor, who can give you independent financial advice, where they can go through all of your options too (there will be fees). You can find great advisors, local to you, with Unbiased¹.

And that’s it. All that’s left to say is enjoy your retirement!

We recommend PensionBee, it’s easy to set up and use, low cost, with simple, easy to understand drawdown options.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

We recommend PensionBee, it’s easy to set up and use, low cost, with simple, easy to understand drawdown options.