Article contents

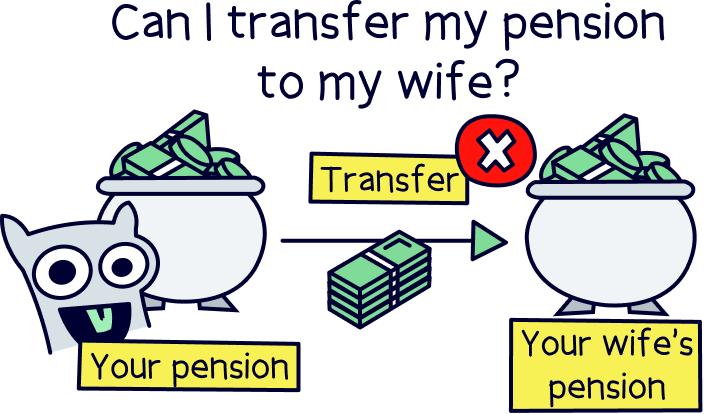

No, you cannot transfer your pension to your wife. However, you can contribute to your wife's pension if they have one, or your wife could easily open one herself. You don’t have to be working to open a pension.

Wondering if it’s possible to transfer your pension to your wife, or put it in her name? Unfortunately it’s not possible.

This is the same with any partner or person, including a civil partner. You can't transfer pensions.

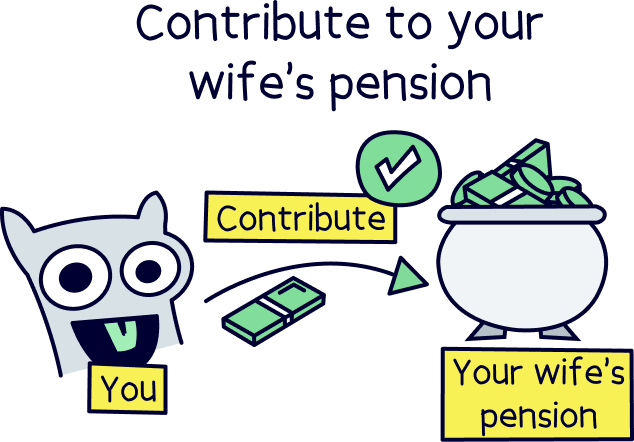

However, there are options to open and build up a pension in her name – you could contribute to her own pension. It’s also worth pointing out that your wife would also benefit from your pension should the worst happen and you pass away, but you can’t transfer it to her while you are still alive.

Check out Unbiased – a free service to find pension experts (financial advisors) in your local area.

Find the best personal pension for you – you could be £1,000s better off.

Unbiased is a great online service to help you find expert financial advisors who can help with your pension.

It’s very popular, with over 10 million customers, and pretty much the go-to-place to find pension advisors local to you.

All advisors are fully vetted, qualified and have years of experience.

You’ll be able to chat on the phone, video call, or visit in person (depending on the advisor).

It’s free to use the service, you’ll pay the advisor directly if you choose to use them (fees vary per advisor and service you’d like).

Find the best personal pension for you – you could be £1,000s better off.

Your best option is for your wife to open her own pension and you contribute towards it. It's easy to do online with great companies such as PensionBee (here’s our PensionBee review). Check out our best personal pensions to learn more.

If your wife doesn’t work and doesn’t pay tax, you can make payments to her pension up to a maximum of £2,880 per year, and get a 25% bonus on what you put in (so they’ll get £3,600 per year in total). Not bad right?

If your wife does work and pays tax, you can make contributions up to her salary figure per year (up to £60,000).

Depending on how soon your wife is set to retire, you could build up a fairly substantial pension pot in a very short period of time.

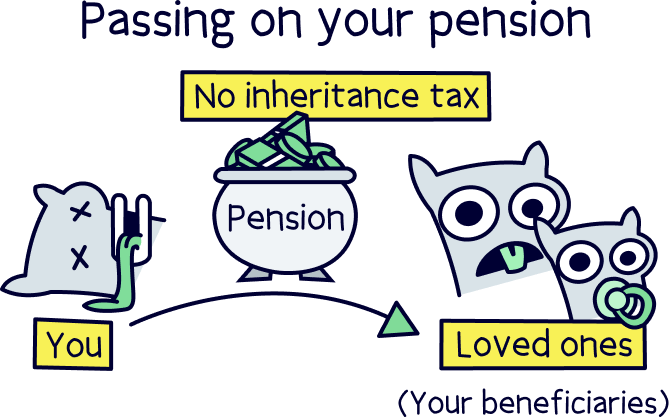

The good news with pensions (among their many benefits, such as tax free saving), is that when you die, they aren’t included as part of your estate (your money), and not subject to Inheritance Tax.

Inheritance Tax is charged if everything you own (your estate) is above £325,000 (called the threshold), and it would only apply to everything above that threshold. It’s a staggering 40%!

Your pension is separate to any of your other assets, such as a Stocks and Shares ISA, which would all be subject to Inheritance Tax when you die.

Although, if you left everything to your wife or partner, they would not normally have to pay tax anyway.

With a pension, you give the name of the person you want to receive your pension (your beneficiary) to your pension provider (the people looking after your pension), and they’ll pass it on when you die. It can be different to your next of kin. Your beneficiary will have to pay income tax (similar to what you have to pay on your salary) on the money if you die over the age of 75.

They’ll have a Personal Allowance of £12,570 before they start paying Income Tax. So if they have no pension savings themselves, they may not end up paying too much tax.

The first 25% of what would now be their pension is completely tax free too. Which they can take as a tax free lump sum. Or, they can take it as income whenever and however they like, and the first 25% of each payment would be tax free cash.

We hope you don’t get divorced in future, but just as a bit of background knowledge, if you do get divorced, your wife can claim a share of your pension. It would then be in her name and she can move it to another pension provider.

And there you have it, it’s not possible to give your pension to your wife, but you can contribute to her own pension, which might be a good alternative if you aren’t planning on retiring soon. Check out PensionBee – our recommended pension provider, it’s easy to open and has low fees.

If you are thinking about providing for your wife in retirement after you die, she’ll get your whole pension, without paying any Inheritance Tax, (as long as you name her as your beneficiary with your pension provider).

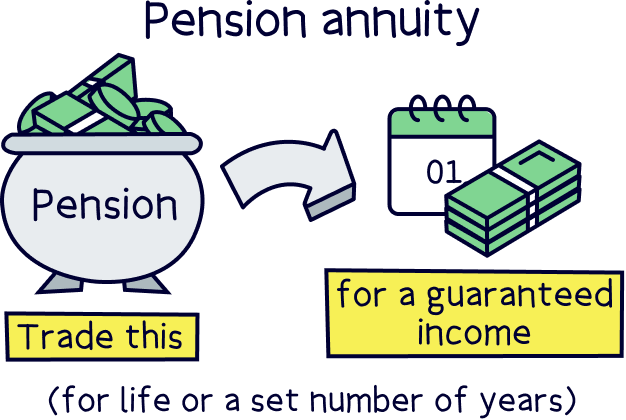

One more thing to mention if you are thinking about using your pension to buy an annuity (which is an income for life after retirement), you could consider a joint annuity which will still make payments to your wife if you die.

Find the best personal pension for you – you could be £1,000s better off.

Find the best personal pension for you – you could be £1,000s better off.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Find the best personal pension for you – you could be £1,000s better off.