Article contents

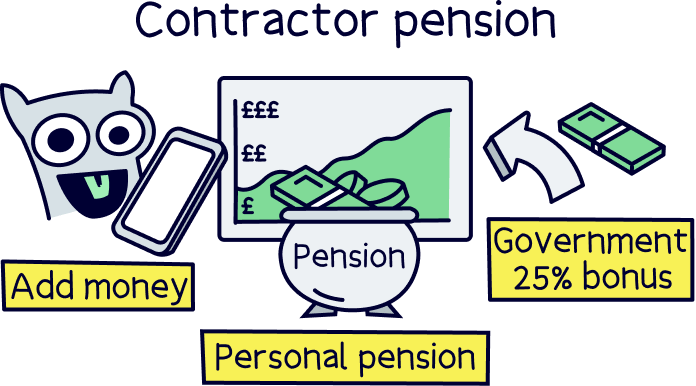

Pensions for contractors are now super easy, all you need to do is open a personal pension – you can pick a provider that’s easy to use, has low fees and a great record of growing pensions. Plus, you’ll get a massive 25% government bonus on everything you put in. And, If you’ve got your own limited company, you’ll be able to reduce Corporation Tax too.

Are you self-employed working as a contractor and not sure what happens with your pension? You’re in the right place.

Saving for your retirement with a pension is super important, and as a contractor, it’s all up to you – there’s no HR department to do it for you.

Let’s run through all your options – you’ll be up and running with your contractor pension in no time.

Note: a contractor pension is actually simply called a personal pension (we’ll run through them in just a mo).

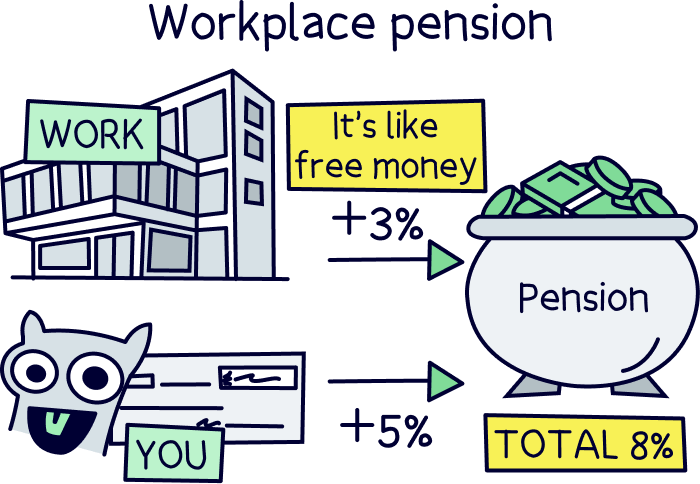

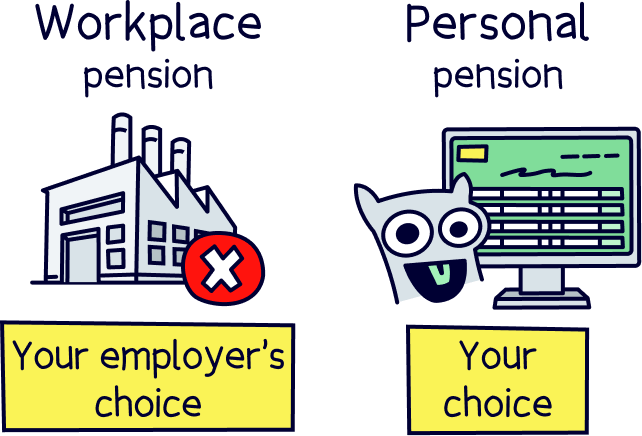

Sorry to say, but as you’re self-employed and not working as an employee, you won’t be eligible for a workplace pension scheme – that’s one that your employer sets up for you as part of the auto-enrolment scheme, and then would contribute 3% of your salary if you contribute 5%.

They’re pretty great for the sole reason the employer contributes too – it’s like a pay rise! But often workplace pension schemes aren’t always the best pensions, employers simply set up any old one because they have to by law. They just get the boxed ticked to call it done, rather than researching and seeking out the best pension schemes for their employees.

That’s where it’s better for contractors and all self-employed people – you get to pick which pension provider you want to use, and can pick from the best ones out there – ones thats are easy to use, have low fees and a great track record of growing money over time.

If you’re already keen to open a pension and not sure where to start, here’s the best pension providers. Spoiler, the top is PensionBee¹, they’re all of the above, and 5* rated. Here’s our PensionBee review to find out more.

Check out PensionBee – it's easy to use, low cost and has a great track record. You'll get £50 added to your pension for free too (with Nuts About Money).

As you’re a contractor, so self-employed, you’re responsible for your own contractor pension, that means you have to set it up yourself, and decide how much you want to pay into it. It might sound daunting, but it's actually a great thing – and super easy to do. The hardest part is taking the plunge, by signing up and committing to a regular saving scheme.

The type of pension you’ll need is called a personal pension (sometimes called a self-employed pension or private pension).

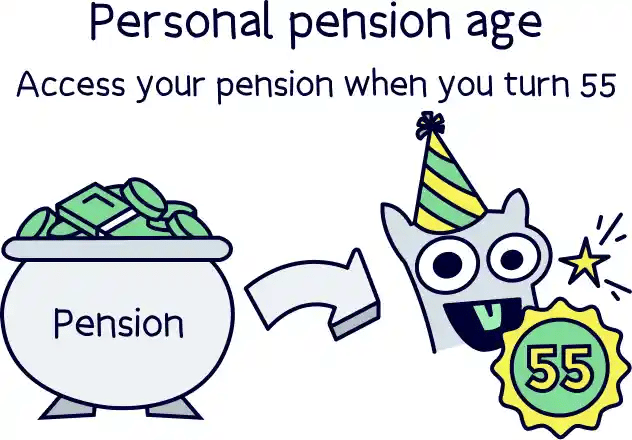

Being a contractor, you’ll have to set up what’s called a personal pension, which is a type of private pension – that’s a pension in your name, private to you, which you manage. That simply means you decide how much you want to pay in and when to take it out, as long as you’re over 55 (57 from 2028).

The other type of private pension is a workplace pension scheme, one that only employees get through work.

With a personal pension, you’ll get all the same great benefits as a workplace pension, except your employer won’t contribute to it themselves (as you’re not employed). With employees, they’ll typically have to add 3% into their employee’s pension, if the employee adds 5%.

The benefits of a personal pension include getting a massive 25% bonus on everything you save into your pension, added directly by the Government (we’re not joking!). This is to refund the tax you will pay on your income (at 20% tax rate), as pensions are intended to be tax-free. Pretty great right?

And if you pay higher rate tax (40%), or additional rate tax (45%), you’ll be able to claim some of the tax back on your Self Assessment tax return. TaxScouts¹ can help you fill in your Self Assessment tax return, their service is low cost and 5* rated.

Your money will also grow tax-free, so it can grow much faster over time, and there’s no paperwork to do.

And, when it comes time to withdraw, 25% of it will be tax-free, which you can take as a tax-free lump sum if you want to – and you can start withdrawing from 55 years old (57 from 2028).

With the remaining 75%, you might pay Income Tax on it (the same as your income now), it all depends on how much your income will be at the time.

All pretty amazing right? And the sooner you start saving, the bigger your pension pot will be when it does come time to retire.

Nuts About Money tip: you’ll need a very large personal pension these days for a comfortable retirement. Use our pension calculator to find out how much you might need for your circumstances, and try our retirement income calculator too.

Typically, we call ‘personal pensions’, pensions that are managed by experts, but you can also make your own investments if you want to, with a self-invested personal pension – more on those below.

If you’re keen to get started but not sure how, check out the best personal pensions, and our top rated provider PensionBee¹. As a bonus, we’ve managed to bag you £50 added to your pension for free too, if you sign up with Nuts About Money.

There’s also a self-invested personal pension (SIPP). They’re exactly the same as a personal pension (so you get all the great tax saving benefits, and a 25% bonus on your contributions from the Government).

However, instead of the experts handling your pension, you’ll be managing the investments yourself – so only recommended for experienced investors.

If this sounds interesting, learn more with our guide to the best SIPP providers.

But, it gets a bit confusing here, as modern SIPPs are actually managed by the experts too – you just pick from an easy to understand range of investment options, all managed by experts (our recommendations above are all actually modern SIPPs!).

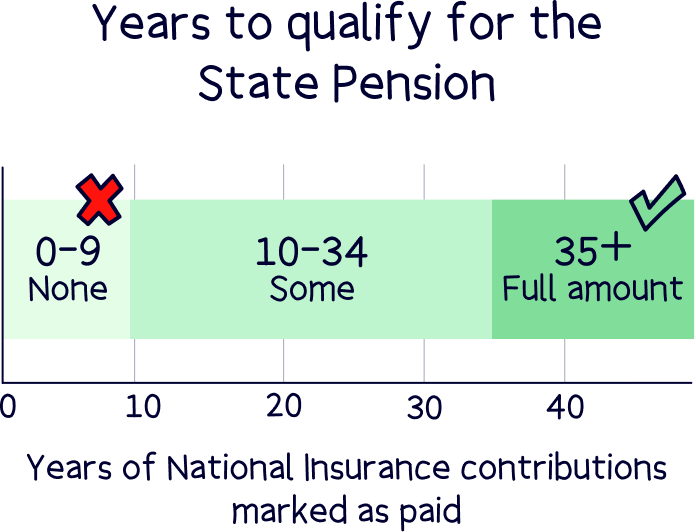

The alternative type of pension is the State Pension, which is the government pension. You’ll get this from the age of 66 (rising to 68), if you’ve paid enough National Insurance contributions over the years. 10 years will get you the minimum State Pension, and 35 years will get you the full State Pension.

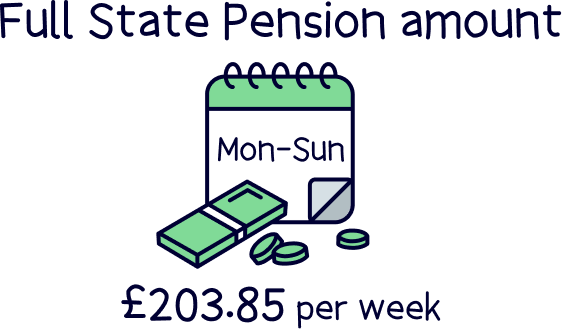

The full State Pension is currently £203.85 per week, which works out as £10,600 per year. Not much to live off, in fact, it's about half of minimum wage.

That won’t cover much in retirement. We strongly recommend building up your own personal pension to provide a bigger retirement income. We’ll cover how much you should be saving into your pension below.

Here’s where to learn more about the State Pension when self-employed.

All make sense so far? It’s pretty simple really. You’ll need to open a personal pension for yourself and make contributions into it.

The great news is that personal pensions have all the same tax benefits as a workplace pension (and even more if you’re a limited company contractor), it’s just handled a bit differently.

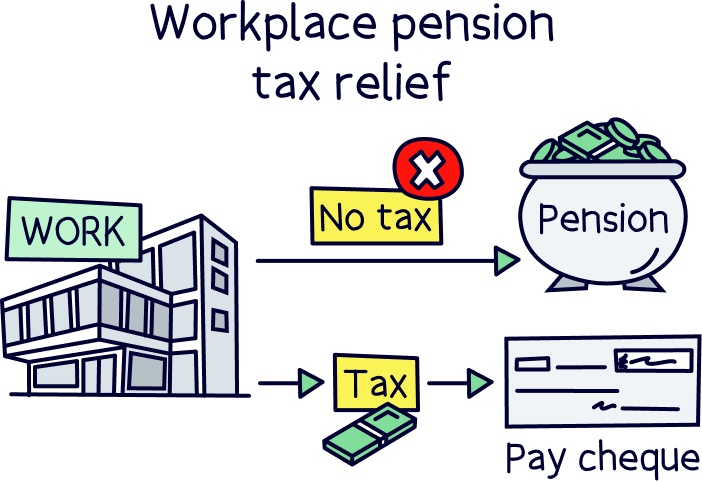

With a workplace pension, your pension contributions are paid directly into your pension before you’ve paid tax, and your employer handles all of this. Your employer should also pay 3% into your pension from their own pocket (called employer contributions), if you pay in 5%, which is part of the auto-enrolment pension scheme. Unfortunately, as contractors aren’t employees, you don’t get this.

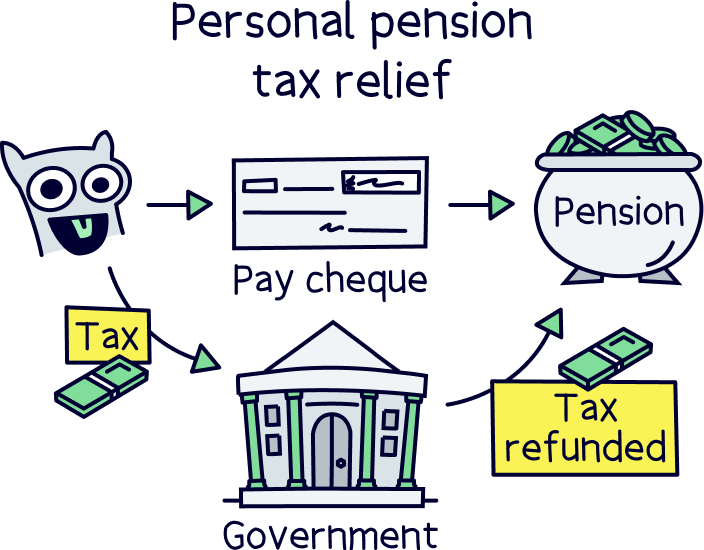

With a personal pension, you’ll have already paid tax on your income, or will do as part of your Self-Assessment tax return, and so you’ll get your tax refunded back as a 25% bonus paid directly into your pension every time you make a contribution. This will do wonders for your overall pension size, it's like getting free money, how good is that?!

And it gets even better if you’re a higher rate taxpayer (40%) or additional rate taxpayer (45%), you can claim what you’ve paid at these rates back too (called personal tax relief, or pension tax relief). All this extra cash can make a massive difference to your total retirement pension pot. It's easy to do too, just add it to your Self-Assessment tax return.

Like the sound of a personal pension (contractor pension)? Great! They’re super easy to set up too. You don’t actually need to do much, simply pick a good pension provider and they’ll handle everything for you. – you’ll be able to pick from easy to understand pension plans suited to you (these are the investments, often called pension funds).

Modern pension providers even have phone apps to help you manage everything, such as your regular contributions and you’ll have complete transparency over your pension balance (like how much is in it, and the projected amount when you retire).

You’ll even be able to decide where your money is invested (which pension plan), for instance in only socially responsible options (e.g. no fossil fuels). We’re a big fan of these at Nuts About Money.

Not sure where to find the best pensions? Don’t worry, that’s what we’re here for. We’ve reviewed the best pension providers and here’s the top ones for contractors:

Get £50 added to your pension

PensionBee is our recommended provider – they’ve thought of everything.

Their 5 star rated app (and website) makes it easy to set up and use. You can open a brand new pension, or transfer your existing pensions across (they’ll handle all the paperwork).

Simply pick from an easy to understand range of pension plans, and that’s it, the experts manage everything from there.

It’s low cost, with one simple annual fee. The customer service is excellent, and you’ll get a dedicated account manager for any questions you might have.

And, when the time comes to retire, withdrawing from your pension is easy too.

You can also use them if you're self-employed or a company director.

Moneyfarm is a great option for saving and investing (both ISAs and pensions). It's easy to use and their experts can help you with any questions or guidance you need.

They have one of the top performing investment records, and great socially responsible investing options too. Plus, you can save cash and get a high interest rate.

The fees are low, and reduce as you save more. Plus, the customer service is outstanding.

Check out PensionBee – it's easy to use, low cost and has a great track record. You'll get £50 added to your pension for free too (with Nuts About Money).

If you're a bit unsure about pensions and would prefer to speak to an expert, check out Unbiased¹ – it's a free service to find pension experts (financial advisors) in your local area.

Unbiased is a great online service to help you find expert financial advisors who can help with your pension.

It’s very popular, with over 10 million customers, and pretty much the go-to-place to find pension advisors local to you.

All advisors are fully vetted, qualified and have years of experience.

You’ll be able to chat on the phone, video call, or visit in person (depending on the advisor).

It’s free to use the service, you’ll pay the advisor directly if you choose to use them (fees vary per advisor and service you’d like).

Check out PensionBee – it's easy to use, low cost and has a great track record. You'll get £50 added to your pension for free too (with Nuts About Money).

If you’re working through a limited company (a limited company contractor), setting up a pension is no different to being a sole trader (not a limited company). You’ll still need to use a personal pension. However, it’s more tax efficient with some big benefits.

Your company pension contributions can actually count as an allowable business expense and therefore reduce your Corporation Tax bill. Which means you’ll be saving an extra 19-25% on all your personal pension contributions. Amazing, right?!

You’ll need to make contributions via your company bank account as a employer, rather than personal contributions (so not your personal bank account) – which is super easy to do with modern pension providers. We recommend checking out PensionBee¹ if you’re a limited company director.

If you’re keen to learn more, here’s our guide to the best pensions for limited company directors.

Now for potentially the most important question, how much should I pay into my pension?

Working out much much you should be paying into your pension each month comes down to how much pension pot you need for the standard of living you want in retirement.

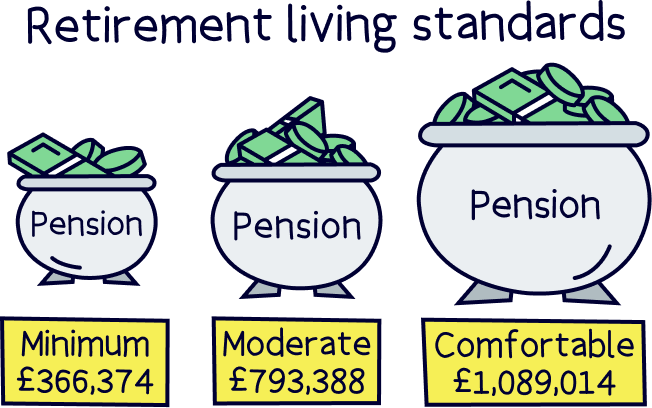

There’s 3 official retirement living standards:

Here’s where to learn more about the Retirement Living Standards – and they’ve been put together by the Pensions and Lifetime Savings Association.

And here’s how much you’ll need as a pension income every year in retirement:

How much you’ll need in your pension pot depends on the level of retirement you’d like – we suggest aiming for at least moderate to comfortable. Here’s how much you’ll need in your pension pot by the time your retire (68):

This is how much you’ll need to save within your personal pension in addition to receiving the State Pension.

If you don’t expect to get the State Pension, here’s how much you’ll need to save within your personal pension:

They’re pretty big numbers, and probably more than you thought! But don’t panic just yet, with the right savings strategy, you’ll be able to build a large pension over time. The key is simply contributing regularly, and letting time do the work to grow your money over time. You’ll be surprised how big your pension could get.

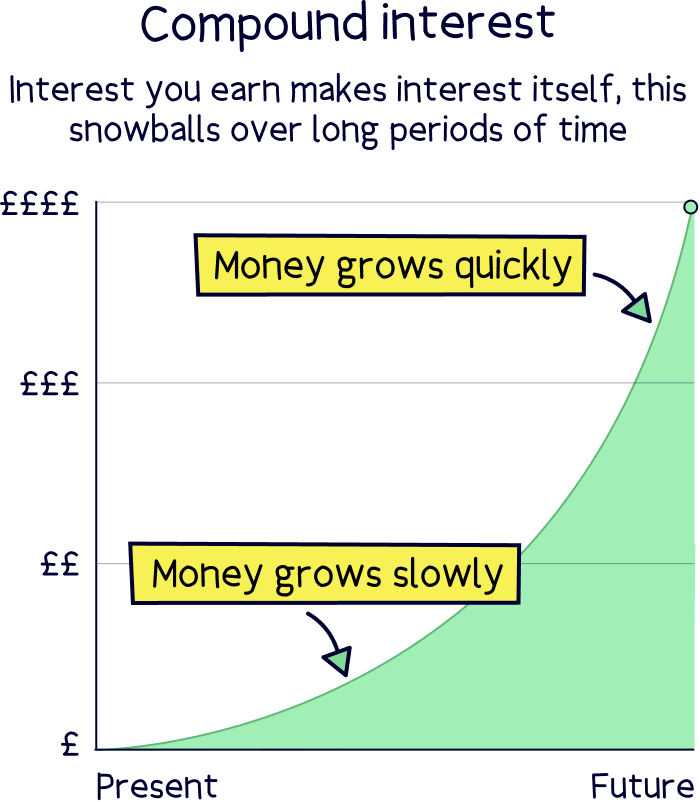

Let’s quickly explain how your pension actually grows over time. It’s all down to something called compound interest. This is when the money you make from your pension each year, also then makes money itself too – and this snowballs (compounds) year after year and turns what can be small figures into very large amounts over time (much more than you actually contribute).

When you save into a pension, your money is actually pooled together with other people’s money into what’s called a pension fund. And the experts managing the pension fund will invest this money in a safe and sensible way to grow it over time, and as it grows, it compounds.

And by making regular contributions, your money grows even more, and your new contributions now begin to make more money for you too.

That brings us to how much you should be contributing per month into your pension to achieve the retirement you’d like. We recommend aiming for a moderate to comfortable retirement if you can.

Let’s take a look at the moderate retirement income, and assuming you don’t already have a pension, here’s what you’ll need to pay each month:

Sorry for the high numbers again! You can learn lots more about this with our guide: how much should I pay into my pension?

If you’ve already got an average pension pot, or any at all to be honest, you could contribute less each month. But we recommend you save as much as possible.

Note: the figures in the table above are just the recommended figures for those starting a pension.

Note About Money tip: you can get a personalised recommendation with PensionBee’s pension calculator.

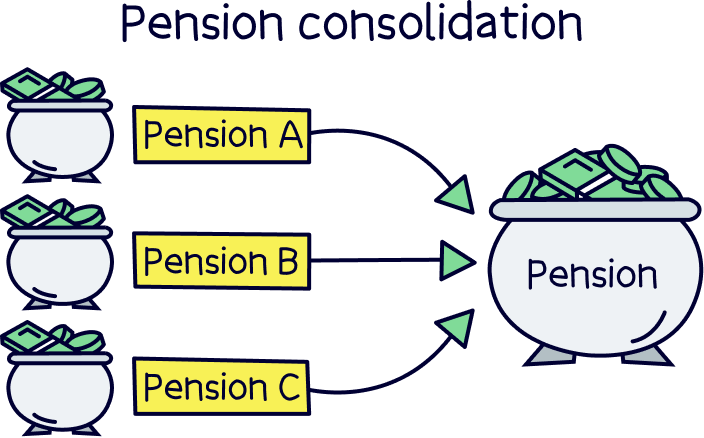

If you’ve got any old pensions lying around, perhaps from your old jobs, it’s a good idea to combine these in your new personal pension, which is called consolidating your pension.

Why? Well, first of all you won’t forget where they are. Your current pension providers likely won’t get in touch with you when you retire, they’d rather you forget about your pension so they can keep charging you fees.

The main benefits though, are that the good pension providers (such as the ones above), will be cheaper and actually reduce their fees when you have more pension savings with them. This can have a big impact on your total pension pot by the time you retire.

And, by using a better pension provider with a good track record of growing money over time, you might find that your pension grows much faster – which again can have a big impact on your pension balance over time.

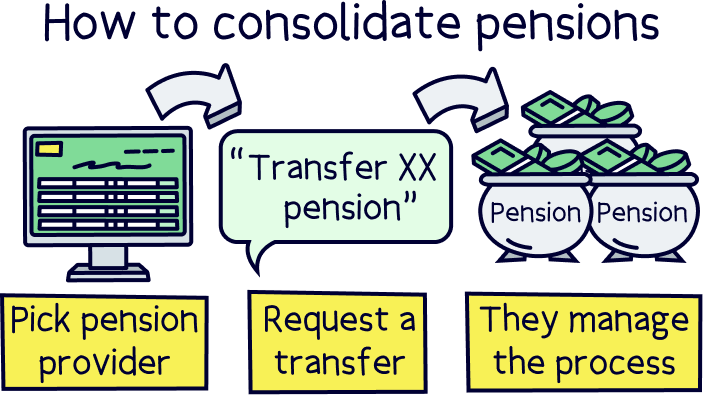

Consolidating your pensions is super easy too – all you need to do is let your new pension provider know who your old pension providers are, and they’ll handle the whole transfer, plus all the paperwork. Your pensions will simply turn up in your account. It really is that simple!

We recommend PensionBee¹ – they’re easy to use, have low fees, and will handle the whole pension transfer process for you, with great customer service.

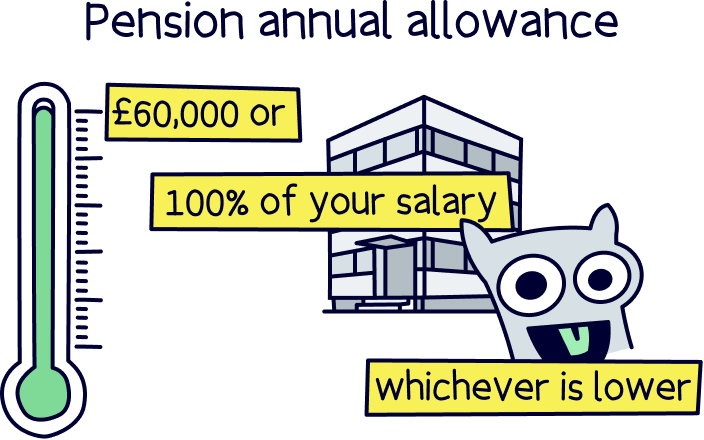

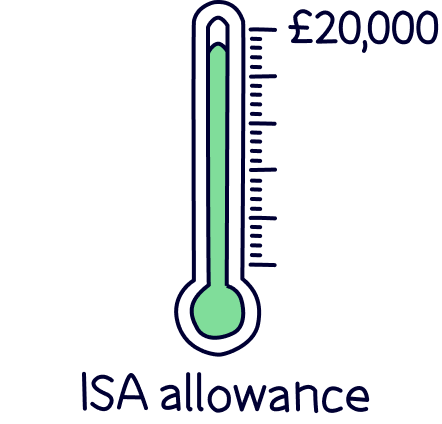

There's a limit on the amount you can pay into a pension each tax year (April 6th to April 5th the following year), called your annual allowance, and it’s either your total income, or £60,000, whichever is lower.

Although if you’re paying into your pension via your own limited company, you can ignore the income rule, the maximum pension contribution per year is £60,000 (across all your private pensions, if you have more than one).

If you think you might hit these limits, consider using a Stocks & Shares ISA alongside a pension – they’ve got great tax advantages, you’ll be able to save up to £20,000 per year tax-free.

Pensions are a bit different when it comes to you sadly passing away. Instead of pensions being included in your ‘estate’ for Inheritance Tax purposes, which is all the things you own, such as property and money. Pensions are completely separate, and their own thing.

Note: Inheritance Tax is typically 40% of your estate (on anything above £325,000).

This means that if you die before you’re 75 years old, your pension would not be taxed at all, and can pass to your family tax-free (or whoever you choose).

If you die after the age of 75, whoever receives your pension would have to pay Income Tax on it, as your pension would count as income. This is the same tax they pay on their salary (if they have a job).

So, they’d pay 20% if they’re a basic rate taxpayer (earning less than £50,270 per year), 40% if they’re a higher rate taxpayer (earning over £50,270 per year), and 45% if they’re an additional rate taxpayer (earning over £125,140 per year).

The beneficiary (person receiving the money), doesn’t have to take it all at once.

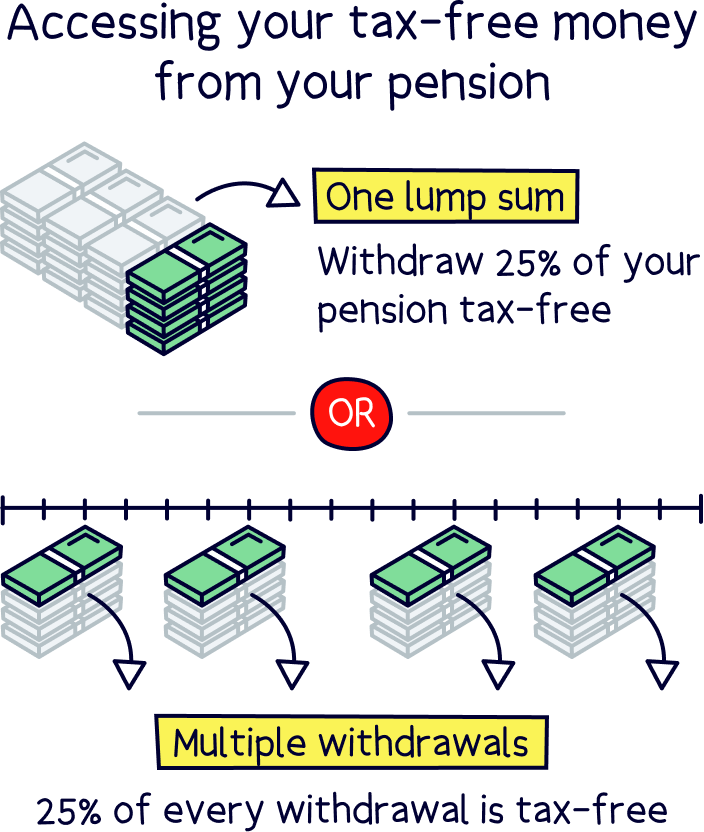

When it comes to retirement, personal pensions are easy too – you get to decide when you want to take your pension, providing you are over 55 (57 from 2028). Although we recommend keeping it in your pension until you really do retire – so your retirement savings have the best chance of growing much bigger!

The first 25% of your pension is completely tax-free, and you can take this as a tax-free lump sum if you like. You could also withdraw as much as you like regularly, and the first 25% of each payment will be tax-free.

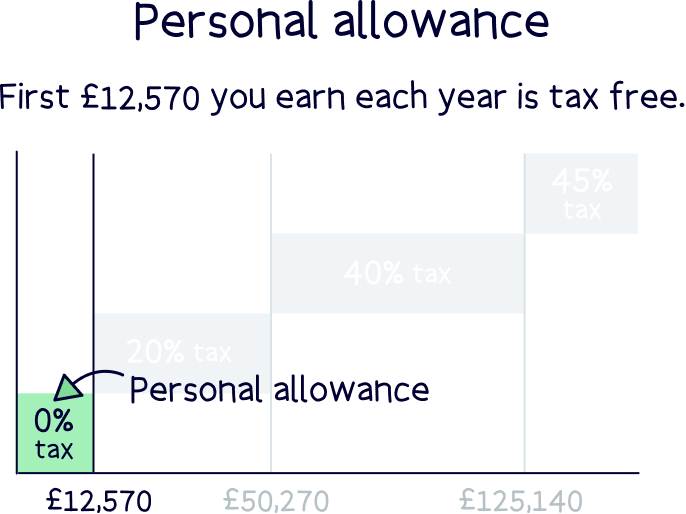

The remaining 75% will count towards Income Tax (the tax you pay now on your income), although how much you pay depends on your income at the time, as you’ll still get a Personal Allowance before you have to pay tax, which is currently £12,570.

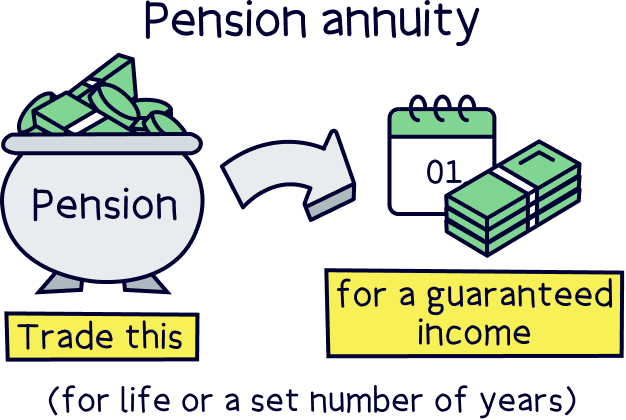

When you do retire, you can either simply withdraw cash from your pension when you want to (called pension drawdown), or buy an annuity…

An annuity is a guaranteed income for the rest of your life (or a set number of years). Your pension provider can help you with this nearer the time, or you can speak to a financial advisor for expert advice. You can find great financial advisors with Unbiased¹.

When you reach the official retirement age (66, but rising to 68), you’ll also be entitled to the State Pension if you qualify.

Nuts About Money tip: if you’re nearing retirement now, learn more about pension drawdown with our guide to the best pension drawdown providers.

Pretty simple really isn’t it? For contractors, all you need to do to sort your retirement savings is to open a personal pension.

A personal pension has some great benefits, you’ll automatically get a 25% bonus on everything you put in. You can also claim tax relief at the higher rate (40%) and additional rate tax (45%) if you’ve paid this.

Plus, you get to pick which pension provider you want to use, and how your money is invested. You can pick one that’s easy to use, has low fees and a great track record of growing money over time.

And, if you work via your own limited company, a pension is one of the best tax benefits you’ve got – as your employer pension contributions can reduce the amount of Corporation Tax you pay, saving even more cash.

If you’re keen to get started but not sure where to find these amazing pension providers, here’s the best personal pensions. And as we've mentioned, PensionBee¹ tops the list – it’s super easy to use, has low fees and a great record. Can you tell we're big fans?!

Moneyfarm¹ comes in at a close second, they don’t just cater for pensions, they have other types of savings accounts too, like a tax-free ISA, plus they offer free expert advice too.

Happy saving! Your future self will thank you. Trust us!

Check out PensionBee – it's easy to use, low cost and has a great track record. You'll get £50 added to your pension for free too (with Nuts About Money).

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Check out PensionBee – it's easy to use, low cost and has a great track record. You'll get £50 added to your pension for free too (with Nuts About Money).