Review contents

Moneybox is one of top go-to places for saving and investing – their Cash ISA has one of the best savings rates out there (5.0%*), and you can save cash, or invest within a range of different accounts, including an ISA, a Lifetime ISA (for saving for your first home) and a pension. The mobile app is easy to use, the fees are pretty low, and the customer support is excellent. 5 stars from us.

Moneybox is fast becoming one of the most popular places for savings and investing in the UK – there’s now over 1,000,000 customers with over £10 billion in savings!

The main reason for that? The ability to save cash and earn a great interest rate on your savings, and the ability to invest your money (with the aim to grow it more), in a range of tax-free investment accounts.

Note: we’ll explain what all the different accounts are, and their benefits below.

The savings rate for cash is currently 5.0%* with their Cash ISA – that’s amazing.

There’s also a great, easy to use phone app that's very highly rated – 4.8 out of 5 from 58,500 reviews on the App Store, and 4.7 out of 5 from 18,700 reviews on Google Play.

If you’re looking to save cash, Moneybox has a range of savings accounts, including an easy access Cash ISA (tax-free), a regular easy access account, and notice accounts (which can give higher rates, but you ‘lock’ your money away – with up to 95 days notice to get your money back).

If you're only looking to save cash, check out the Cash ISA on the Moneybox website¹, for one of the best savings rates you’ll find.

If you’re looking to invest, Moneybox makes investing easy. You’ve got all of the main investment accounts available – a Lifetime ISA to save for your first home (tax-free and 25% bonus), a Stocks and Shares ISA (tax-free), and a personal pension (to save for retirement, and includes a 25% government bonus).

There’s a limited range of investments to choose from, which is ideal for those just getting started with investing, as you'll only choose from a handful of investments selected by Moneybox.

The investments include a range of popular investment funds (groups of different investments, all put together into a single investment), suited to different investment goals. More on these below.

For those more experienced, you can also buy individual US stocks (e.g. Apple and Amazon), and all commission-free (other fees apply).

Plus, Moneybox also has some great features to help you save more, such as rounding up your spare change when you spend, and calculators to show you much you’ll likely need to be saving to achieve your goals (e.g. a house deposit or retirement).

Right, that was a lot of information wasn’t it? If you’ve heard enough already, head to the Moneybox website¹ to get started.

Otherwise, let’s dive into what it all means and all the details.

Get a top saving rate with the Moneybox Cash ISA. The mobile app is easy to use and the customer support is excellent.

Yep! It’s perfect for beginners in fact – it’s designed for those who are new to saving and investing, and it’s very easy to use.

If you’re just looking to save cash, maybe you’re saving an emergency fund, or saving for your first home, or even transferring your life savings, you can simply open an account in a few minutes, add your money, and that's it!

With investing, you don’t need to know a lot to start with, although knowing which investment account you’d like will help (e.g. a Stocks and Shares ISA), we’ll cover those in detail below.

Otherwise, the app and website will guide you through all the investment options you can choose from, and if they might be suitable for you – we’ll cover the range of investment below too.

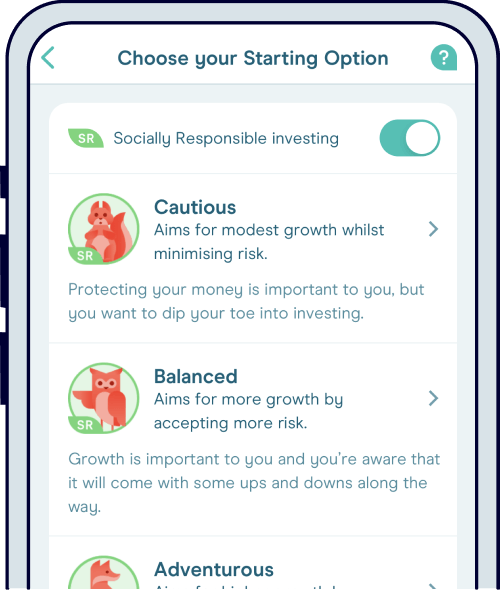

There’s three easy to understand ‘starter options’, which you can simply pick, and let the expert investors handle things (recommended for beginners).

On the app and website, there’s a wide range of information in the ‘Learn Hub’, with some great articles on investing and saving in general, for instance how to get started investing.

Looking to just save cash? Moneybox has got some great options – and one of the best rates out there right now with their Cash ISA…

A Cash ISA is a savings account where you get an interest rate for saving money and it's completely tax-free! That means all the interest you earn, is completely tax-free forever – you don’t have to worry about paying a penny. Want to know how much you'll make over time? Check out our Cash ISA calculator, and here's all the Best Cash ISA accounts.

If your money isn’t within an ISA (Individual Savings Account), you might have to pay tax on your interest, depending on your total income (e.g. your salary), and if the interest is over a certain amount.

Outside of a Cash ISA, you’ll pay tax on interest above your ‘Personal Savings Allowance’, which is:

If you earn less than £17,570 per year, it gets a bit more complicated (but you’ll be paying less than 20% tax). Learn more with our guide to Cash ISAs.

In an ISA, you can save up to £20,000 per tax year (April 6th to April 5th the following year), and this applies as a total across all your ISAs if you have more (perhaps a Lifetime ISA to save for your first home).

With Moneybox, the interest rate you’ll get is pretty great – it’s currently 5.0%*.

It’s that high because there’s a bonus of 0.47% for the first 12 months. After 12 months, the interest rate will reduce.

By the way, you’ll need to save at least £500 in your account to get the higher rate. If you’re saving under £500, you’ll get a low rate of 0.75%.

Also, and this bit is important, if you are intending to make lots of withdrawals, you’ll likely be better off with the Simple Saver account (below).

With the Cash ISA, you can make as many withdrawals as you like, but you can only make 3 withdrawals per year (12 months) to keep the same high rate.

After the 4th withdrawal, the rate will reduce to 0.75% (until you’ve had the account for 12 months, and then goes back up, and the 12 months starts again), a bit confusing we know!

Overall, it’s pretty great for long-term saving – learn more and get started on the Moneybox website¹.

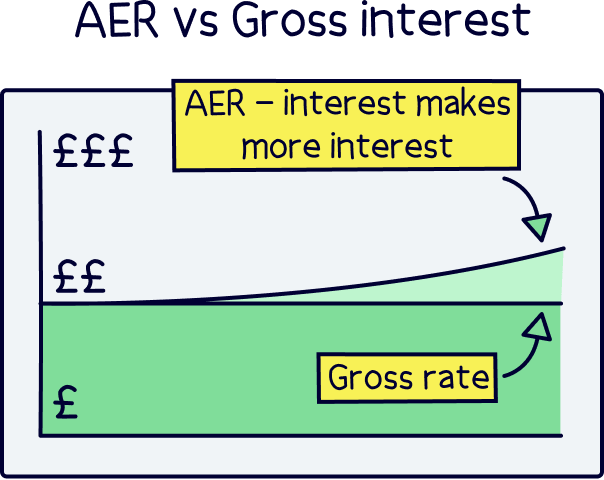

Note: *This is AER, which means it’s the rate after saving for a full year, so includes your interest making a bit of interest too. You’ll still get paid interest monthly. It’s also ‘variable’ which means Moneybox can change the rate in future.

The Simple Saver is your typical savings account, you can add and withdraw money whenever you like, often called an ‘easy access savings account’. However, you are limited to one withdrawal per month.

With Moneybox, you’ll get a savings rate of 3.5%. That’s pretty good for an easy access account. Normally, you’ll get a higher rate if you lock your money away for a certain amount of time, which is typically in a notice account – more on those below.

Note: The savings rate can change in future. If you’re making lots of cash in interest, you might have to pay tax on it (explained above).

Notice accounts are where you ‘lock’ your money away, and you can only get it back after you give ‘notice’ – that’s asking for a withdrawal, and then it will be returned after a certain amount of days.

With Moneybox, you can choose from:

The number of days represents how long you’ll have to wait to get your money back after requesting a withdrawal.

Typically, the longer time you wait, the higher interest rate you’ll get (although not always the case). The rates are generally really good with Moneybox. For up-to-date rates, check the Moneybox website¹.

Note: again, this savings rate can change in future. If you’re making lots of cash in interest, you might have to pay tax on it (explained above).

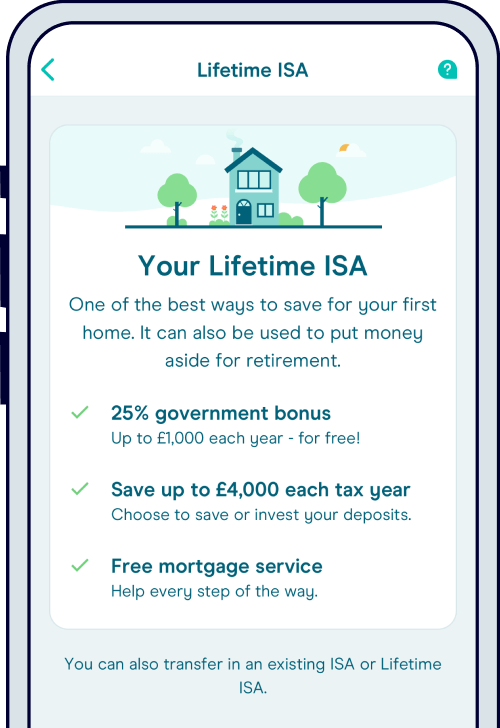

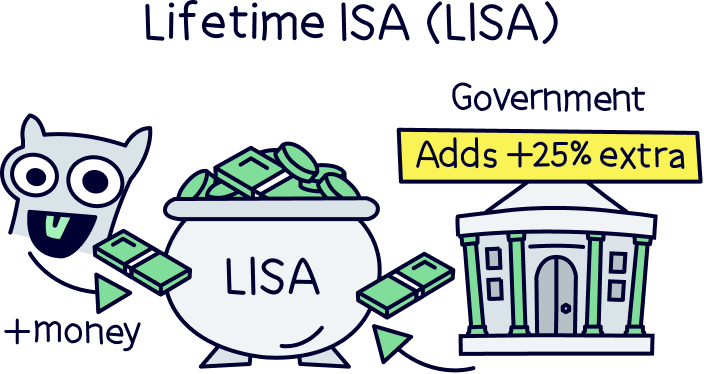

A Lifetime ISA is designed to help you save for your first home, and has some pretty great benefits – you can save up to £4,000 per year, and you’ll get a massive 25% bonus on anything you save, and alongside that, everything you make within the account is tax-free!

To find out how much you could save check out our Lifetime ISA calculator.

There are some limitations, you can only use it to buy a home worth less than £450,000, and you have to have the Lifetime ISA account open for at least 12 months. So open it soon to get the clock ticking!

With Moneybox's Cash Lifetime ISA, you’ll also get a great saving rate (5.0%), in fact, it’s one of the best out there. Visit the Moneybox website¹ to find out what it currently is, you can also check out our Best Lifetime ISAs.

This rate lasts for the first 12 months, as it includes a 1% bonus, and after that it will reduce drop.

Note: *This is AER, which means it’s the rate after saving for a full year, so includes your interest making a bit of interest too. You’ll still get paid interest monthly. It’s also ‘variable’ which means Moneybox can change the rate in future.

Aside from the Cash Lifetime ISA, you can also invest within a Stocks and Shares Lifetime ISA (25% bonus and tax-free), a Stocks and Shares ISA (tax-free), a General Investment Account (not tax-free), a personal pension (25% bonus), and a Junior ISA (if you have kids).

With the Stocks and Shares Lifetime ISA, instead of saving cash, you can make investments with the intention of making more money over time (although not guaranteed).

You’ll still get the 25% bonus from the Government on everything you save, and your money grows tax-free. You can save up to £4,000 per year.

If you’re just starting out saving for your house deposit, and think it will take quite a while to save (over say 5 years), you might want to consider this option, as typically, you have a stronger chance of making more money over time. We’ll cover the investment options below.

Again, check out our Lifetime ISA calculator to find out how much you could make, or to learn more about Moneybox Lifetime ISAs, visit the Moneybox app¹.

With a Stocks & Shares ISA, you can invest up to £20,000 each tax year (April 6th to April 5th the following year), and everything you make is tax-free, forever! It’s pretty great.

The £20,000 allowance is shared across all of your ISAs, so if you’ve got a Cash ISA or a Lifetime ISA too, it’s shared between them. You can take the money out whenever you like too.

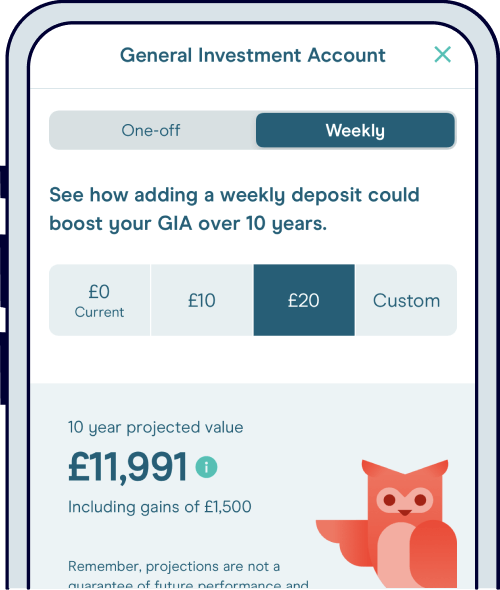

This is your standard investment account where there are no tax-free benefits. You’ll have to pay tax on the money you make over £3,000 per tax year (if you sell your investments). Expect to pay 10%-20% on your profits, and it’s called Capital Gains Tax.

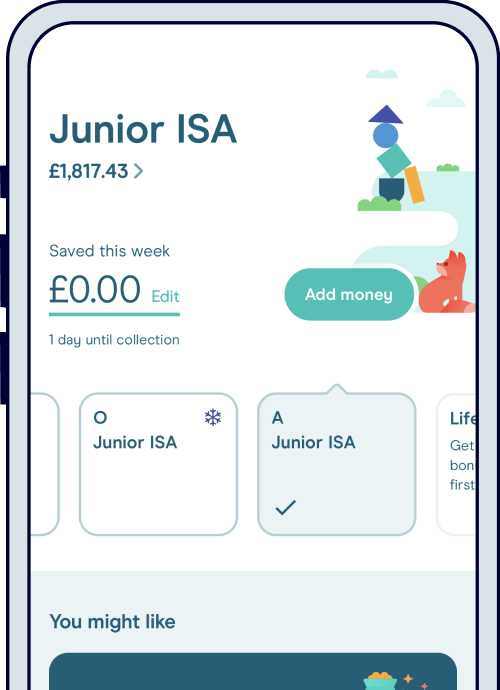

Got kids? This is a great option to build a little nest egg for them for later in life.

You can add up to £9,000 into a Junior ISA each tax year, and everything it makes is all tax-free. It’s all in their name and doesn’t affect your own ISA allowance of £20,000. They’ll get access to it when they turn 18.

You can invest within the full range of Moneybox’s investment options.

Note: at the moment, only existing customers can open a Junior ISA.

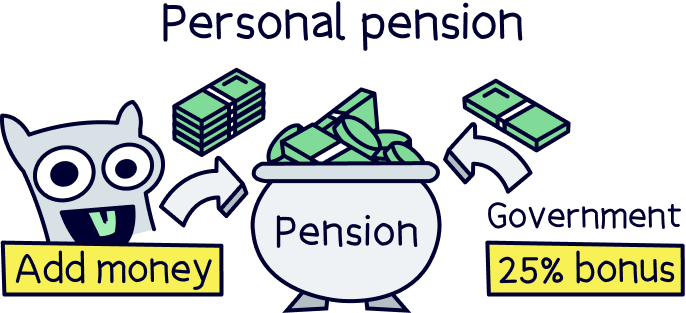

You can also open a personal pension with Moneybox – that’s a pension you manage yourself, rather than your employer (called a workplace pension).

It’s a great idea to open a pension alongside a workplace pension (and your only option if you’re self-employed), you’ll get a huge bonus of 25% from the Government, on everything you add, the bonus is added automatically to your account.

Plus, you can claim back 40%, or 45% tax if you’d paid it, if you earn over £50,270 per year.

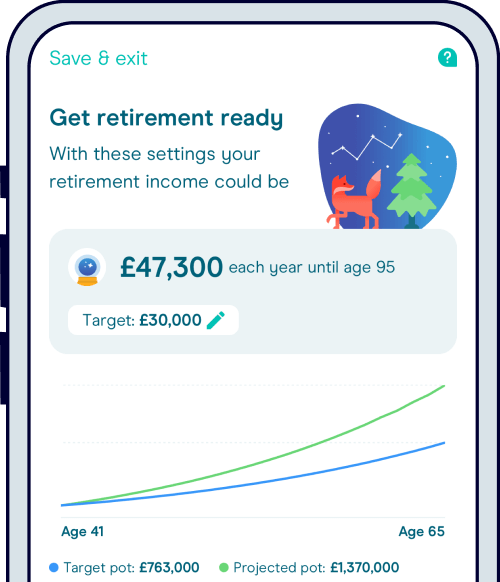

However, it is for retirement, so you won’t be able to touch the money until you’re at least 55 (57 from 2028), but it could seriously improve your lifestyle in retirement if you start saving early and regularly. Estimate your yearly retirement income based on your pension pot with our retirement income calculator.

Nuts About Money tip: want to learn more about saving for retirement? Here’s our guide to personal pensions and where to find the best personal pensions. or check out our pension calculator to estimate your total pension pot at retirement and your yearly retirement income.

With Moneybox, you’ll have to decide how you want to invest your money.

There’s a good range of investment options suited to those new to investing, and those looking to be more hands-off with their investment strategy.

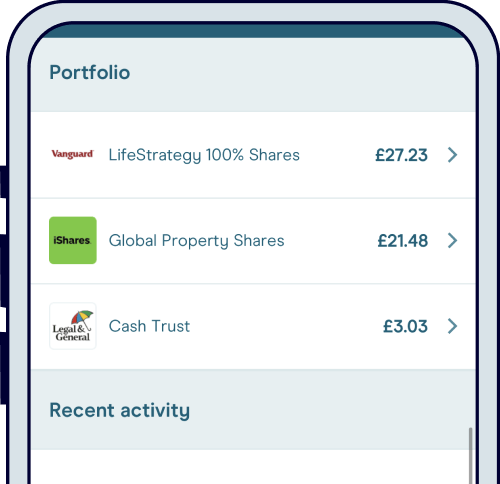

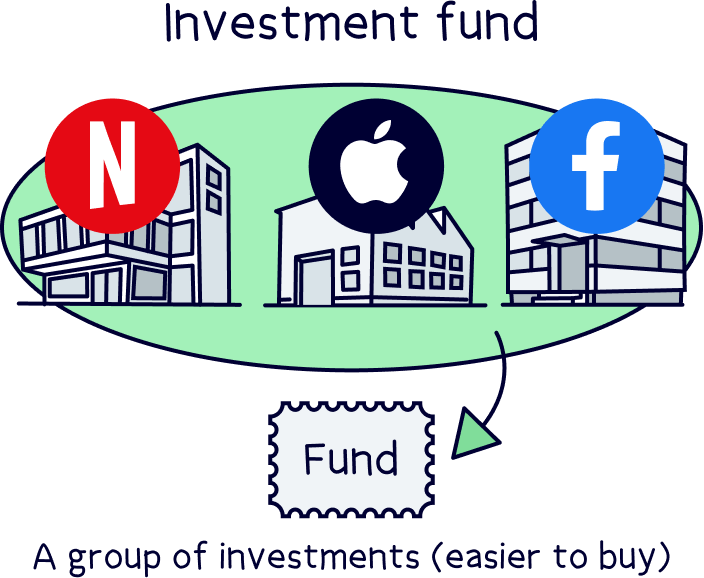

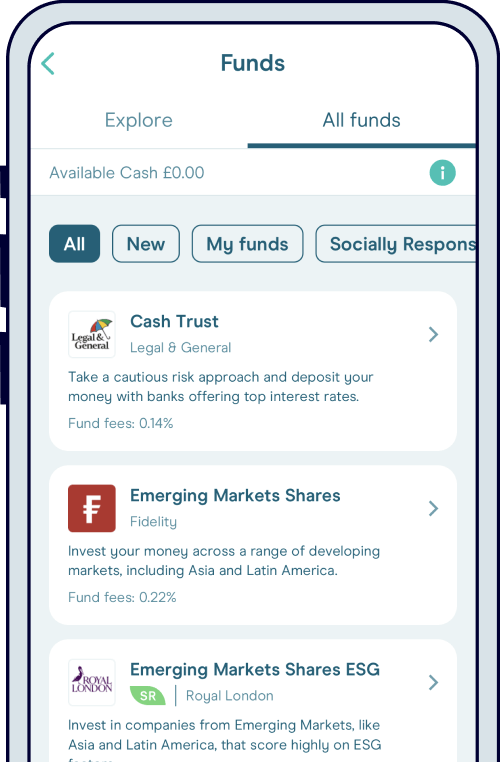

There’s two different types of investments you have with Moneybox, which are investment funds, and individual stocks and shares…

Investment funds are a collection of lots of different investments, all packaged into a single investment, making them easy to buy and sell (and often cheaper).

These can be a range of individual shares (covered below), or things like bonds, which are effectively loans to governments and large businesses, and there could even be commercial property.

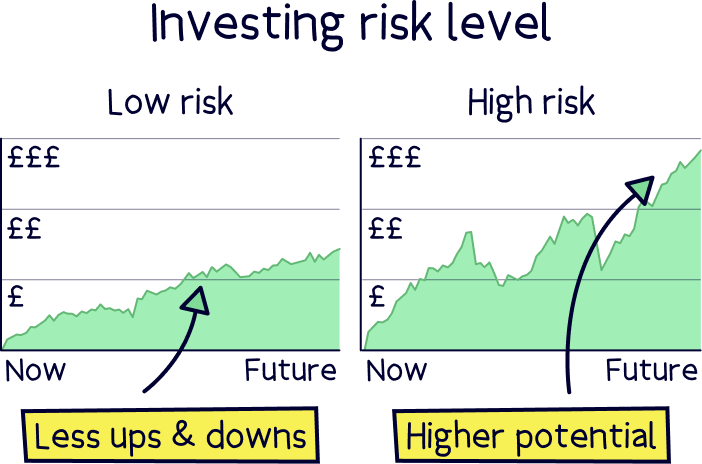

The investment fund is put together by a group of experts, and they’ll make the decisions when to buy and sell the investments within the fund. With Moneybox, there’s three ‘starter options’ that cover different risk levels (low, medium and high).

Note: risk is how big the ups and downs can potentially be over time, with lower risk having smaller ups and downs, and higher risk having bigger ups and downs – with higher risk, the idea is your money could grow larger over time.

A fund typically has a theme or a goal, for instance, it could be the top 100 companies in the UK (FTSE 100), the top 500 companies in the US (S&P 500), or things like growing companies across the world.

A fund could also have a goal, which could be to simply grow over time, where you can let the experts handle things. Or, they aim to provide a regular income (kind of like getting a salary), with little risk to your money, for instance depositing the investment money with banks that pay high interest.

For the full range of funds, you’ll need to download the Moneybox app¹.

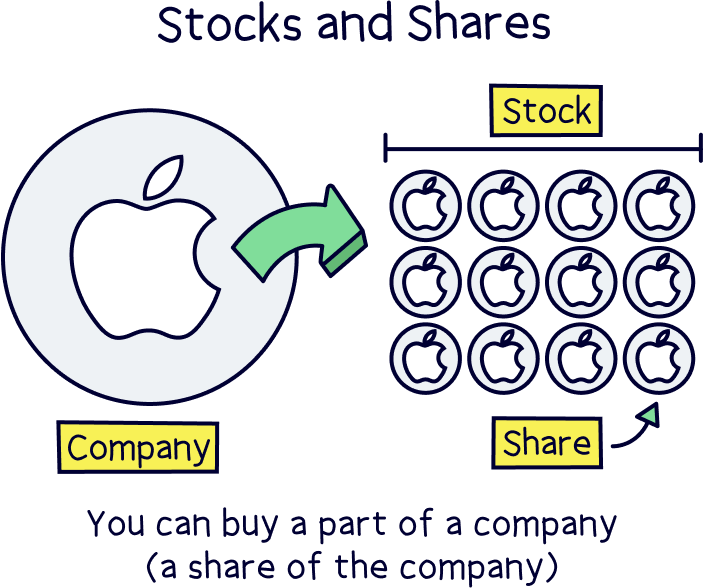

You can also invest in a range of individual companies, by buying their shares (also called stocks).

A share represents a small part of company ownership. All the shares of a company added together represent the total value of the company, and typically if a company does well (e.g. make more profit), their value increases and so does the price of their shares.

With Moneybox, you can only invest in US companies (so no UK companies, or companies from across the world).

There’s a good range, and includes all the popular companies such as Amazon, Alphabet (Google), Microsoft, Nike, Tesla, and loads more.

For the full range of stocks, you’ll need to download the Moneybox app¹.

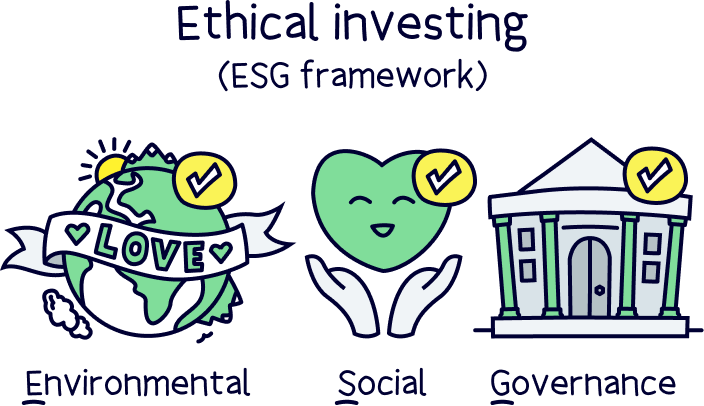

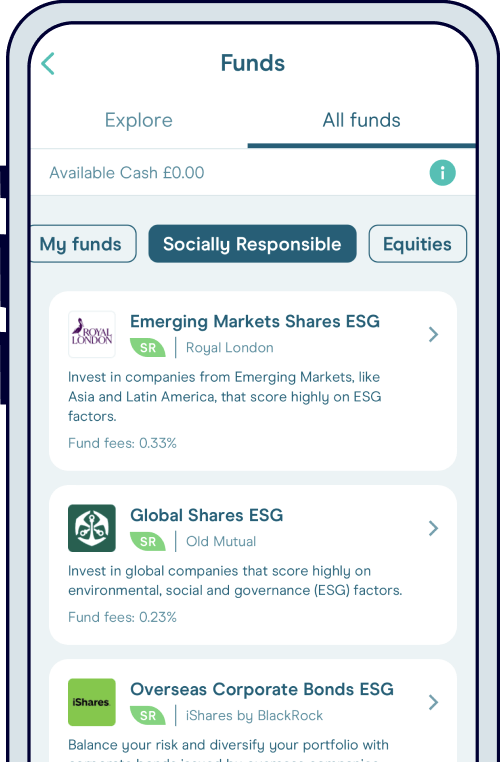

You can also choose to invest your money ethically and socially responsible. This means your money won’t be invested in any businesses that are damaging the environment, such as large energy companies, and only invested in businesses that look after their employees and are well managed (i.e. no corruption).

This is called ESG:

Environmental: combating pollution, climate change, water usage, and deforestation.

Social: great treatment of employees, good health and safety, diversity, and helping local communities.

Governance: corruption, inequality and bribery – and steps that are taken to mitigate this.

Moneybox allows you to browse ESG funds to find the right one for your money.

Moneybox also has some great tools to help you save and set goals.

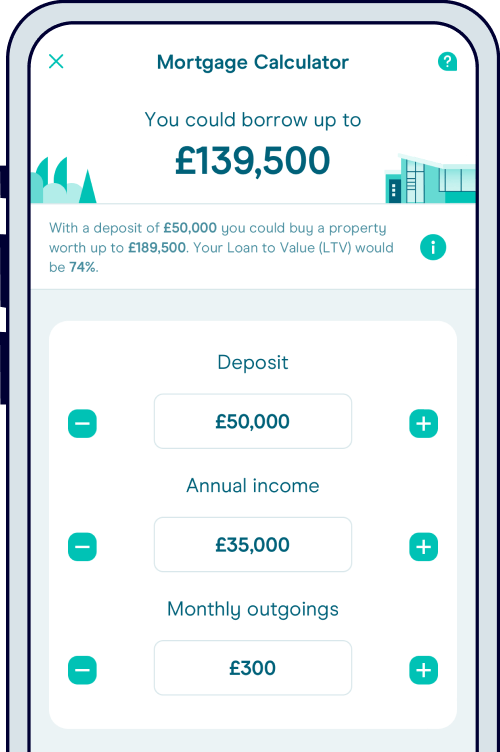

There’s a house deposit calculator¹ to help you work out how much you’ll need for a house deposit, and how much to save – which you can then use with their Lifetime ISA.

And, there’s a pension calculator¹ to help you plan how much you’ll need in your pension pot, and how much you should be saving for the retirement you’d like (or use our own pension calculator (we think it's pretty great)).

Spoiler: how much you should have in your pension is normally a lot more than you think! It’s a great idea to put away something extra into a personal pension regularly, alongside your pension from work, to help boost your overall pot. Small savings now can have a big impact down the line. Learn more with our guide to the best personal pensions.

And there’s loads of helpful content tackling some of the more complicated topics in personal finance.

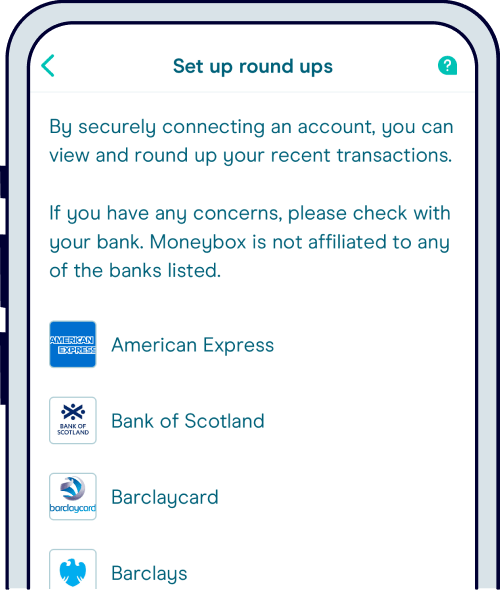

You can link your bank account to your Moneybox account, and whenever you spend, you can round up your spare change and put this into your savings account. Pretty great for building those savings without even really noticing.

Fees (what you’ll end up paying) can get slightly complicated, and it all depends on which savings and investments accounts you’d like. Let’s run through what you’d be paying:

If you just want to save cash, for instance in a Cash ISA, there’s no fees to pay.

Note: Moneybox will still earn money, but they essentially get a fee from the bank where your money is actually saved.

With investing, there’s a few different fees:

Note: if you have multiple accounts for instance a Stocks and Shares ISA, and a pension, you’ll only pay the £1 monthly subscription once.

And, with a pension, if you have over £100,000 saved, the annual charge reduces to 0.15% for anything above £100,000.

These charges are all taken from your savings automatically too, you don’t need to pay them manually.

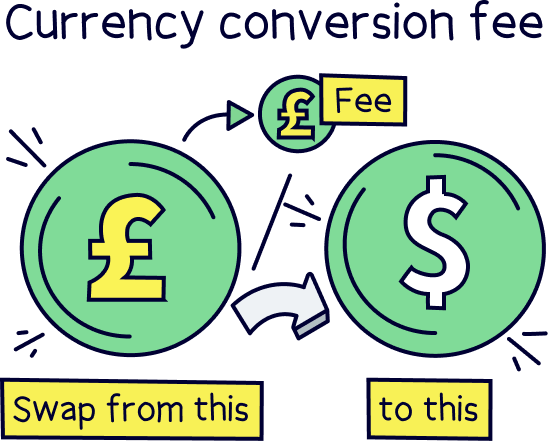

And great news, when buying investments, including individual stocks and shares, there’s 0% commission! So no fees to buy and sell, although there are currency conversion fees for individual US stocks…

If you do buy individual stocks and shares, for instance Apple shares, as they’re all US companies (with Moneybox), they’re priced in US Dollars.

So, in order to buy the stocks, Moneybox will need to change your Pounds into Dollars – this is all handled automatically by Moneybox when you buy the stock, but there will be a charge of 0.45%, when you both buy and sell.

This is pretty reasonable, and in-line with most stock brokers (this fee typically ranges from 0.15% to 1.50%).

Note: if you want to exchange currencies check out our currency converter tool.

The customer support is great. There’s a very good FAQs section on their website which covers pretty much everything you might want to know, and in an easy to understand way.

You can also speak to their customer support team directly, by messaging within the app itself, and the response time is great, or if you like you can email in. Unfortunately, you can’t speak on the phone.

The team is also available seven days per week, and from 9am to 5:30pm.

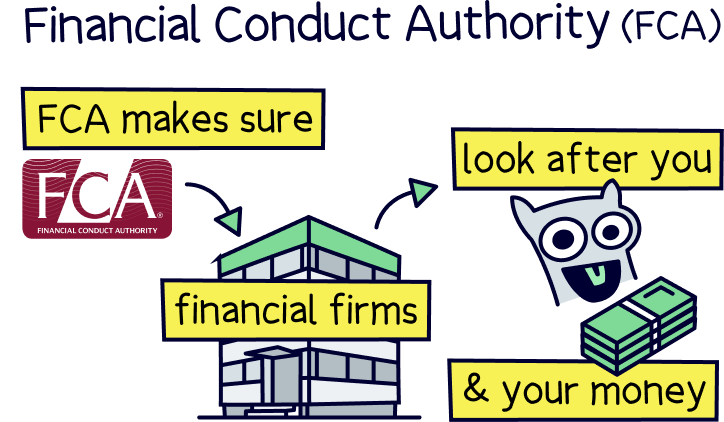

Yep! It’s perfectly safe. Moneybox is authorised and regulated in the UK by the Financial Conduct Authority (FCA), which means they’ve been reviewed and approved to look after your money.

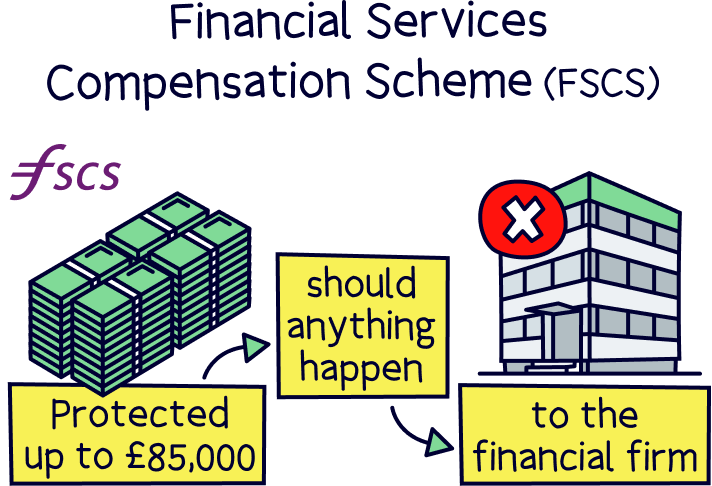

Any savings you have are also protected by the Financial Services Compensation Scheme (FSCS), which gives you protection up to £85,000, should anything happen to your money – which is highly unlikely. Your money is stored safely with large banks and not Moneybox itself.

Your investments are also held with the fund themselves (in your name), and not with Moneybox, so you’ve got extra protection – your investments can only be returned to you.

Let’s run through the pros and cons of Moneybox.

Customers love Moneybox. On the popular reviews site, Trustpilot, it has an excellent score of 4.4 out of 5 from over 2,500 reviews.

In financial services, this is an especially great score – most financial services companies get very low ratings, as they’re typically very complicated and offer very poor customer service.

With Moneybox, most of the reviews mention the great customer service, and how great the app is.

We think Moneybox is great! Our mission here at Nuts About Money is to help the UK with their money – and we love companies doing the same.

Moneybox is great for those of us who struggle to save, the app itself is super easy to use too, and the customer support is great. Although there’s a lot going on within the app itself, with all the different account options – so it might take a while to get used to it initially.

It’s also one of the best savings rates out there for a Cash ISA (5.0%*) – so if you’re looking to save cash, and tax-free, it’s a great option. There’s also a range of different savings accounts with good rates.

With investing, it’s great too. The investment options are great for those new to investing, or have a more hands-off approach to investing. These include investment funds and US stocks (with 0% commission).

The range of investment accounts is great too – including a Lifetime ISA, Stocks and Shares ISA, Junior ISA and a pension.

When it comes to fees, it’s pretty low cost. And, there’s extra features to help you save more, such as rounding up your spare change.

Overall it’s a big 5 stars from us. If you’re keen to learn more, or get started, head over to the Moneybox website¹, or download the Moneybox app¹.

Get a top saving rate with the Moneybox Cash ISA. The mobile app is easy to use and the customer support is excellent.

Get a top saving rate with the Moneybox Cash ISA. The mobile app is easy to use and the customer support is excellent.

Get a top saving rate with the Moneybox Cash ISA. The mobile app is easy to use and the customer support is excellent.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things money, with years of combined experience working in the finance industry and writing about money. We understand the ins and outs, how to get the best deals, save money, and how to communicate money in an easy to understand way (we hope you agree).

More than 20 years of combined experience researching and writing about money

Researched and reviewed a wide range of financial services companies, and have a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Get a top saving rate with the Moneybox Cash ISA. The mobile app is easy to use and the customer support is excellent.