Review contents

Standard Life is a traditional pension company, and very well established (nearly 200 years old). It’s more commonly known as a pension provider for workplaces, but you can also set up your own pension. However, our opinion is that it's possibly stuck in the past, with a traditional way of doing things, including a dated app and website, a limited range of investment options (only provided by Standard Life), and average customer service. There’s possibly better options out there if you’re looking to combine old pensions or set up a new pension.

Standard Life is a very well established company, and is nearly 200 years old! It’s part of a larger business called Phoenix Group, which is one of the largest financial companies in the UK.

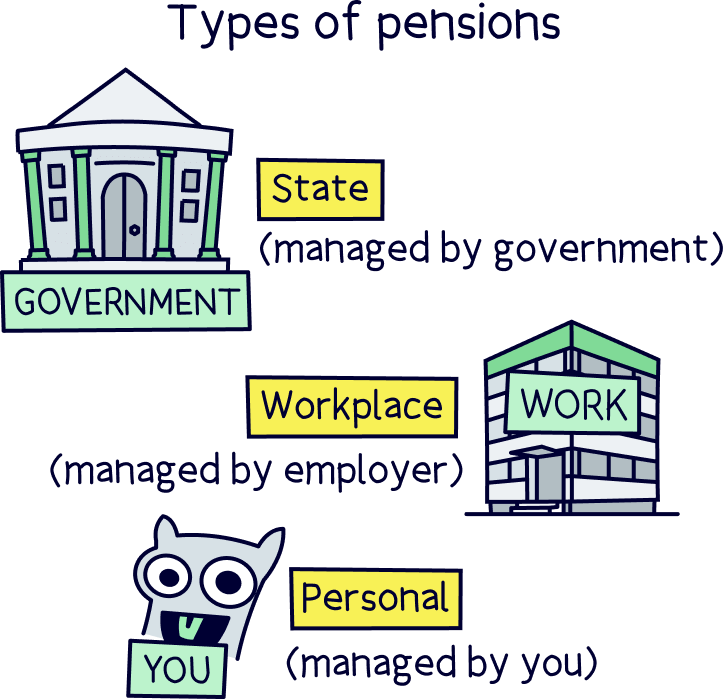

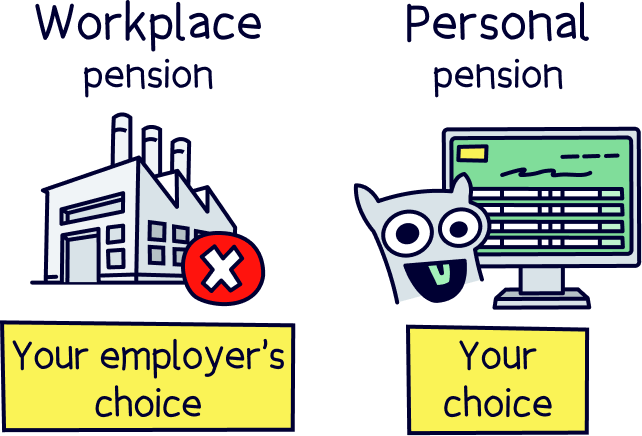

It’s one of the largest pension providers of pensions offered by companies to their employees (technically called workplace pensions), but we’re just going to look at it's personal pension options (often called a private pension), which is a pension you can set up yourself (personal to you), either in addition to a workplace pension (often a good idea to boost your total pension pot or combine old pensions), or if you’re self-employed, it's your only option to get a pension.

By the way, you don’t get a choice which pension provider you can use from work, your employer will decide. And most of them aren’t amazing unfortunately. Which is why a lot of people tend to transfer their pension to a personal pension after they leave their job, as it gives them full control over their money, and they can choose which pension provider to use (some of the modern ones are really great. In fact, check out our best personal pensions table if you’re interested).

Anyway, back to Standard Life, and opening your own pension... As a spoiler, we think Standard Life is okay overall, but has become outdated and potentially struggled to modernise. Their app and website is not that easy to use or understand, and doesn’t offer that much in terms of investment choice (explained below), doesn’t have a reputation for good pension growth (based on reviews), and the customer service could be improved.

It’s a very big, old company, which can suit some people who prefer a traditional pension provider, but we think there’s likely better options out there for a lot of people.

Note: don’t worry if you’ve got a pension with Standard Life from work, you’ll still be getting all the great tax saving benefits, including free cash from your employer (explained below). Adding money to a personal pension is also tax-free (learn more with our pension tax relief calculator).

If you are looking to set up a new pension or combine pensions, we recommend checking out PensionBee¹ – it’s easy to set up and use, there’s a great mobile app, the customer service is excellent (you get a dedicated account manager), and they can combine old pensions quickly and easily. If you like the sound of that, get £50 added to your pension for free too (with Nuts About Money).

Or, as mentioned, check out all our top picks for pension providers. Another great option is Moneyfarm¹. Anyway, back to Standard Life, let’s dive into the details.

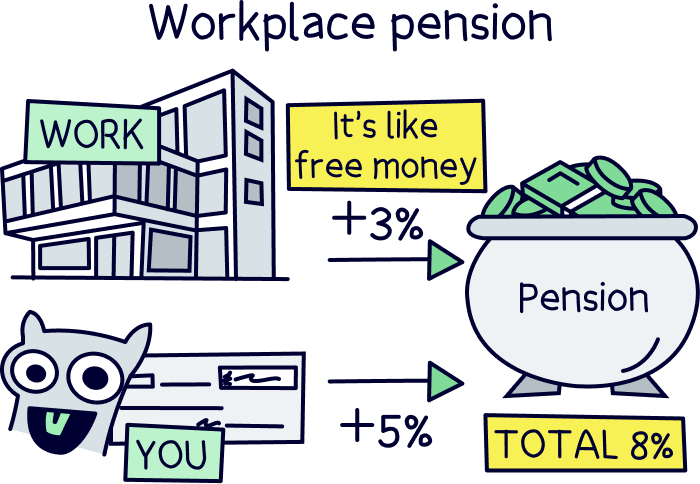

If you’re enrolled onto a Standard Life pension with work, your employer will handle everything for you. This is called auto-enrolment.

Nuts About Money tip: it’s often not a good idea to ‘opt out’ of your work pension, as your employer will normally add free cash to your pension themselves (normally if you pay 5% of your salary in, your employer must add 3% in too, by law).

And we’ll all need a pretty hefty pension pot for a comfortable retirement these days. Check out our pension calculator to see how much you might need when you retire, and our retirement income calculator to see how much your pension pot might provide in future.

With Standard Life, if you’re setting a pension up yourself, you can either get started online via the Standard Life website, or you can apply on the phone too. It should take around 10-20 minutes to fill out your details, and then once you’re set up, you can set how much you want to save (such as monthly top ups), or transfer an old pension from a previous employer if you want to. They’ll run some checks, and then you should be all good to go.

The main bit here is picking which investment option you want, and we’ll run through that below.

PensionBee is easy to use, has low fees and a great record. Plus, get £50 added to your pension for free.

If you’ve got old pensions, such as from an old job, as long as you’re not working there anymore, you’ll likely be able to transfer these to Standard Life if you want to. Technically speaking this is called pension consolidation.

If your old pension is a ‘defined benefit’ pension, which means you have set benefits when you retire, such as a guaranteed income, you might not want to transfer these. These are more common in public sector jobs such as the NHS.

Instead, it might be a sensible idea to simply keep them where they are – as the benefits are normally very good. However, it may be possible to transfer it, but it’s often a good idea (and sometimes legally necessary) to speak to a financial advisor first.

Did you know that your money in a pension is actually invested? This is a good thing, and it’s how it grows over time (often to very large sums by the time you retire). And this applies to all pensions, even workplace pensions. So, when you set up your own pension, you’ll need to decide how your pension is invested.

With Standard Life, you can either opt for their ready made option, which is suited to those who want everything set up for them (so not confident in choosing investments). Or, you can make your own investments (from a select range of Standard Life investment funds).

Ideal for if you don’t know too much about investing and not confident with things like picking funds (how and where your money is invested), don’t worry, not many of us are!

With Standard Life, there is a ‘ready made’ option, which will simply invest your money into a standard plan that will aim to grow your money sensibly over time until you are 15 years out from retirement, and then with 15 years to go, it will gradually change the investments, to provide a steady income ready for when you retire.

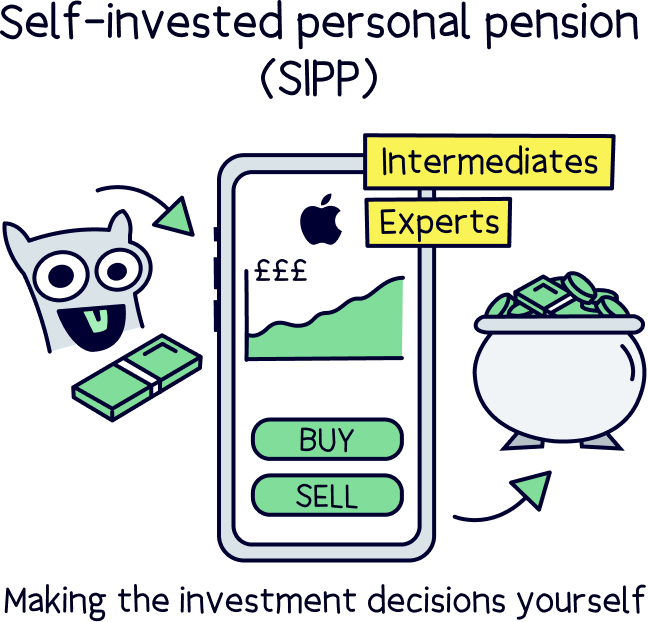

Standard Life also offers a range of their own funds to choose from, and there’s around 50 in total. It’s not an investment platform where you can make lots of investments, such as stocks and shares in individual companies or lots of funds from different investment companies. That’s typically called a self-invested personal pension (SIPP) and offered by investment platforms (although technically the Standard Life pension is also a SIPP). If that’s what you’re looking for, check out our picks of the best SIPPs.

With Standard Life, they operate almost all of the funds themselves, so you are picking a Standard Life fund, and each has a different theme or objective, and you would pick one or a few suited towards your goals and how you would like your money invested. So, really, it’s only for experienced investors.

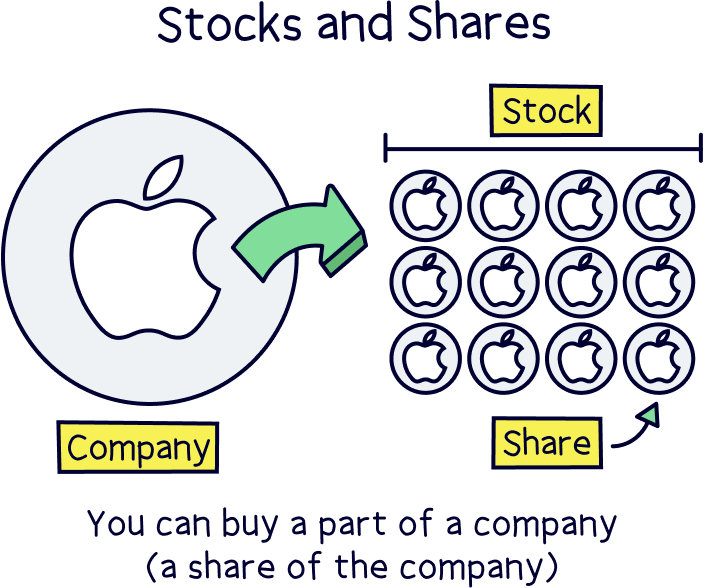

The themes range from stocks and shares (called equities) in various countries or regions, for instance companies in the UK, Europe, North America, the Far East or globally. Or set things such as saving your money as cash to provide regular interest.

There’s not a great range, so if you are an experienced investor, you might struggle to build and manage your own personalised portfolio with just these (again, use an investment platform if you want to do this), but you may find it’s suited to you.

Overall, the total cost will depend on what investments you choose to have within your pension. It’s not on the super cheap side, but also not on the super expensive side either.

The total fee is made up of a ‘service fee’ and a ‘fund charge’. The service fee is what Standard Life charges to essentially manage things behind the scenes (like running their app and website, customer service etc.), and is not part of the investment. This is typically 0.45% per year of your pension pot.

The fund charge is a fee for the experts who actually buy, sell and manage the investments within the fund (which in this case is usually Standard Life). And the fee depends on what investment funds you choose.

For the ready made option, the fund charge is 0.10% per year of your pension pot, so the total fee you’ll pay is 0.55% when added to the 0.45% service fee. For a pension plan, that’s pretty reasonable.

Fund fees in general range from as low as 0.10% (and sometimes lower) to well over 1% and more.

For instance, customers may opt for the Standard Life sustainable multi asset fund range, which has fees of 1% or 0.99% or thereabouts (depending on which specific fund), so overall you would be paying 1.45% per year when added to the service fee.

The amount of ways you can contact Standard Life's customer support is pretty good, but the service maybe not so much. There’s an online help centre on their website which answers frequently asked questions, you can send a message in directly via the website or app if you are a customer too (called a secure message), and you can call them on the phone. The phone lines are open from 9am to 5pm during the week (except Wednesdays when it opens at 10am). There’s no online live-chat service which you would expect these days.

However, there does appear to be issues with the quality of the support, with phone calls not being answered quickly, being on hold for a long time, and responses not being received quickly or issues resolved quickly and accurately. So it's the standard traditional big company service we’re sure you are used to!

Yes, it’s safe to use Standard Life as a pension provider. They are very well established and trustworthy. Standard Life is authorised and regulated in the UK by the Financial Conduct Authority (FCA), which means they have been approved and are trusted to look after and protect your money.

On the popular reviews website, Trustpilot, Standard Life has an average score of 3.7 out of 5. It’s not the worst but it’s not the best. There’s almost as many 1 star reviews as there are 5 stars (and not many in between), which is somewhat unusual.

The volume of 1 star reviews is a bit concerning, and lots of the reviews mention the lack of customer service, which we touched on above. As it’s a very large company, often the service isn’t great, and this is apparent in the reviews.

However, there are some great 5 star reviews, and lots of these are referring to the pension transfer service (which is an online service). But this isn’t unique to Standard Life, most modern pension providers can transfer your old pensions for you.

Here’s a quick recap and the pros and cons of Standard Life:

Standard Life is a trustworthy pension company, and has a strong British heritage of nearly 200 years, but it’s probably fair to say it hasn’t quite caught up with the modern world yet.

The website and app is fairly complicated to use and to set up a pension, with lots of complicated language and explanations, you do need to know a bit about investing and how pensions work to understand it (e.g. what a fund is), especially if you are looking to build your own investment portfolio.

This probably comes from it being a large workplace pension provider (pensions with work), where the customer doesn’t really do much as it’s all set up for them, rather than being designed for people setting up their own pension (a personal pension).

When it comes to the investment choice, you are restricted to their own investment fund options, so you can’t pick and choose investments from lots of different providers, or individual stocks and shares, like you can with other self-invested personal pension providers.

The customer support isn’t particularly great (based on reviews), and has a more traditional approach (e.g. waiting on hold), rather than modern and quick response times via live-chat like some other companies do.

Overall, we’re saying it’s an okay option, and we’re giving it 3 stars. If you’re got a workplace pension with them, there’s nothing to worry about, but if you’re looking to start a new pension or combine old pensions, there’s some really great options out there, which you might want to consider first…

We typically recommend checking out PensionBee¹, as it’s easy to use, has excellent customer service, and a great app to manage things. You’ll also get £50 added to your pension for free (with Nuts About Money). And check out all our top picks for pension providers for more options and information.

To learn more about pensions, visit our pensions page, and if you want to know more about Standard Life, head over to the Standard Life website.

PensionBee is easy to use, has low fees and a great record. Plus, get £50 added to your pension for free.

PensionBee is easy to use, has low fees and a great record. Plus, get £50 added to your pension for free.

PensionBee is easy to use, has low fees and a great record. Plus, get £50 added to your pension for free.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things money, with years of combined experience working in the finance industry and writing about money. We understand the ins and outs, how to get the best deals, save money, and how to communicate money in an easy to understand way (we hope you agree).

More than 20 years of combined experience researching and writing about money

Researched and reviewed a wide range of financial services companies, and have a transparent review process

We follow a strict editorial code to ensure you get the best information possible

PensionBee is easy to use, has low fees and a great record. Plus, get £50 added to your pension for free.