Capital at risk. ISA terms apply. Read Lightyear review.

Capital at risk. Interest earned daily, paid monthly.

Read Trading 212 review.

T&Cs apply. Read Moneybox review.

T&Cs apply. Read Moneyfarm review.

T&Cs apply. Read Chip review.

T&Cs apply. Read Plum review.

Lock your money away for 1 year in return for a set amount of interest. All available online. All have FSCS protection. Interest rates are AER* fixed.

Interest paid monthly, annually or end of fixed term.

Lock your money away for 2 years in return for a set amount of interest. All available online. All have FSCS protection. Interest rates are AER* fixed.

Interest paid monthly, annually or end of fixed term.

Lock your money away for 3 years in return for a set amount of interest. All available online. All have FSCS protection. Interest rates are AER* fixed.

Interest paid monthly, annually or end of fixed term.

Lock your money away for 5 years in return for a set amount of interest. All available online. All have FSCS protection. Interest rates are AER* fixed.

Interest paid monthly, annually or end of fixed term.

All data is sourced by Nuts About Money, or provided directly by the provider. Seen something inaccurate? Get in touch.

Our Cash ISA tables are in order of what we believe is best for you – earning the most interest on your cash! The interest rate shown is AER (more on that below).

We’ve also looked at the features and service of the provider, alongside the interest rate, to give a Nuts About Money rating. This includes:

We’re only showing the very best Cash ISAs we’ve found (there are lots out there), and ones that are available nationwide, and open online (via a website or a mobile app).

Interested in learning more? Here’s our full review methodology and how we test.

Note: All accounts we list have FSCS protection (protection up to £85,000) – more on that below too.

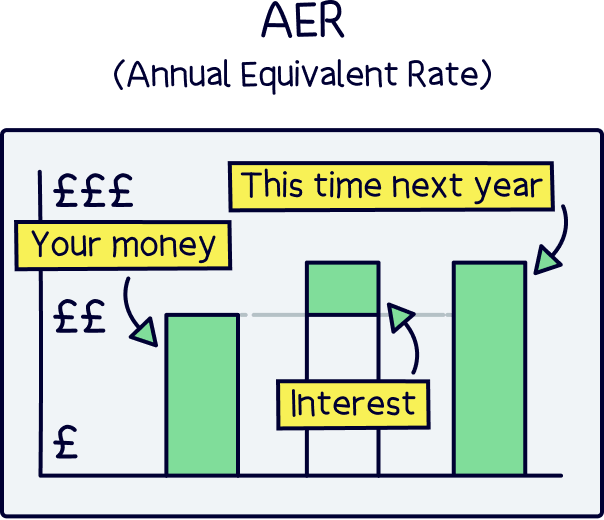

‘AER’, or Annual Equivalent Rate is how much interest you’ll earn this time next year (12 months). It’s used to measure the interest rate of a savings account.

Example: if the AER is 5%, you’ll simply earn 5% of the amount you save in 12 months time.

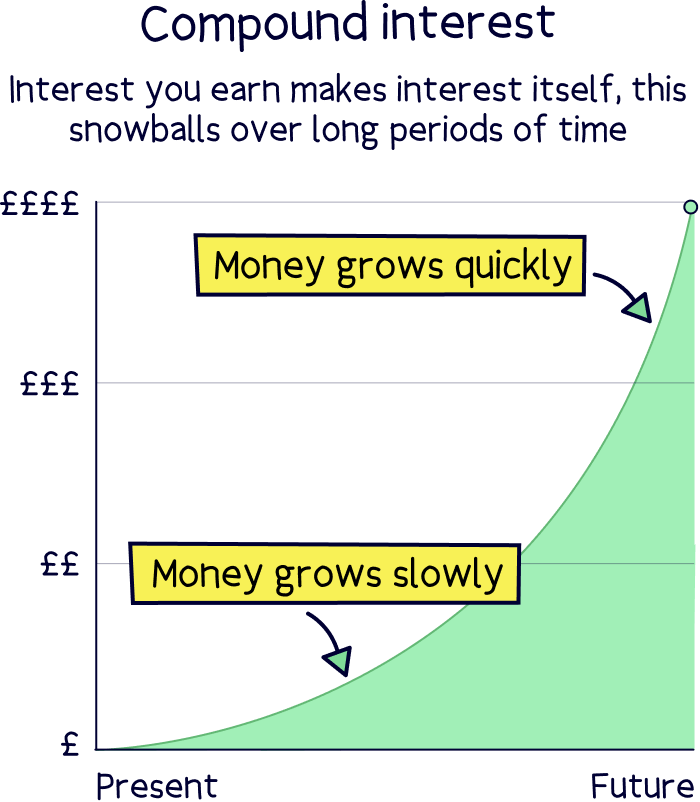

Technically speaking, it counts the interest that you make during the time period, earning money, and making interest too. Which is called compound interest. For example, you might earn interest daily, and this interest earns a tiny bit more interest every day, which snowballs over and over throughout the year.

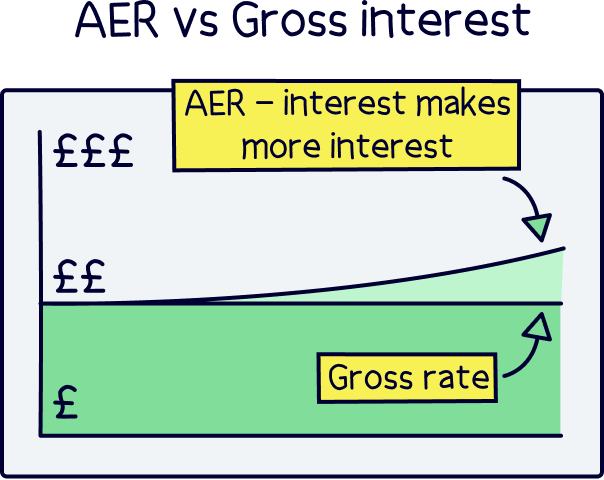

If an interest rate is the ‘gross rate’, it wouldn’t include this compounding interest amount, and therefore typically be a slightly lower rate, but means how much interest the savings account itself actually pays over a year.

Nuts About Money tip: don’t compare gross rate vs AER – use one or the other when comparing savings accounts. Most people and savings companies will simply use AER as it’s easier to compare like for like.

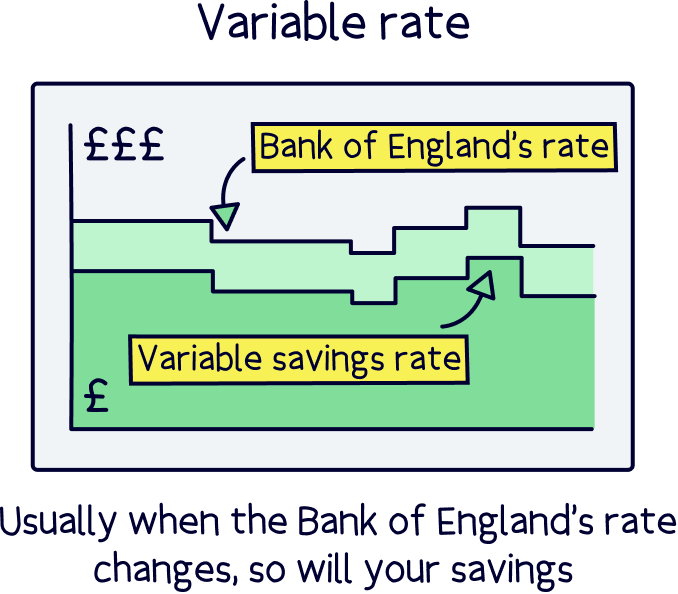

A variable interest rate is where it can change over time (it varies over time). The provider (company) chooses when to change it. Typically the interest rate they offer is linked to the Bank of England’s base rate, and when they change the base rate, cash ISA providers often change their interest rate too (which can be both up and down).

A fixed rate is where the interest rate stays the same (fixed) for a certain amount of time, and the provider can't change the rate (e.g. a 5 year fixed rate) until after the agreed amount of time.

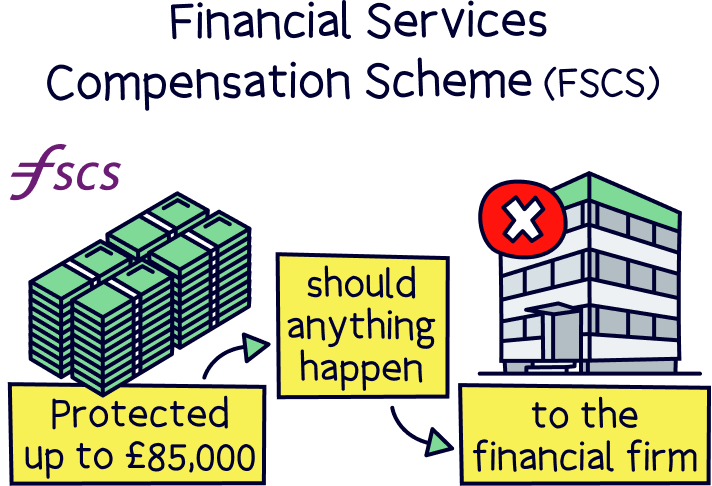

Financial Services Compensation Scheme (FSCS), is like insurance for your cash. It protects your money (up to £85,000) when you save it with a financial services company (such as a bank). You don’t need to pay anything extra for it.

If the company holding your money were to go out of business, and not return some of your money, then the FSCS would step in and give you the money back themselves.

It’s to give you the reassurance that you can save with any approved provider you like, while having the protection your money is completely safe – perhaps one that you haven’t heard of before but offers a great interest rate.

If you’ve got more than £85,000 in savings, you could spread this across a range of different providers to help protect all your money.

However, should a company go out of business holding your money, it’s highly unlikely you wouldn’t receive any of your money back, as customer’s money is typically separate from the company’s own money, and they aren’t able to access it – it's in your name, and can only be returned to you.

An ISA, or Individual Savings Account is an account that’s part of the government scheme to help you save tax-free. So anything you put into an ISA will be exempt from any tax at all (e.g. the interest you earn).

If you save outside of an ISA, you might have to pay tax on the money that you make (it depends how much you make, and how you make it).

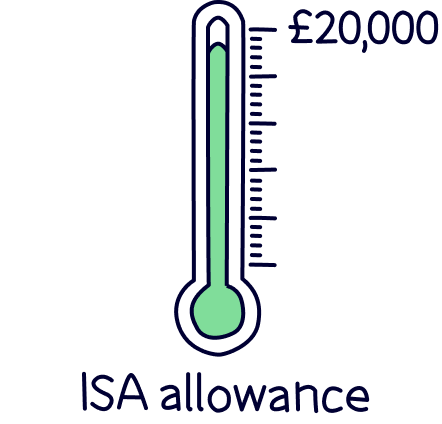

You can save up to £20,000 per year as a total across all of your ISAs (if you have more than one). We’ll cover the limits in more detail just below.

The most popular ISAs are a Cash ISA (for saving cash), and a Stocks and Shares ISA (for investing).

A Cash ISA is where you can save cash in exchange for interest payments, and works like a standard savings account with your bank. You add money, and you get interest in return. Except you don’t pay any tax on the interest you make.

If you had lots of cash in a standard savings account that wasn’t an ISA, you might pay tax on the interest if it was more than your Personal Savings Allowance – which is how much you can earn tax-free in interest before paying tax on it (each tax year). Here’s how much you might pay if you earned more than your allowance:

As an example, if you earned £40,000 per year from your job, you’d be able to earn £1,000 in interest before you have to pay tax on it. And anything above £1,000, you’d pay 20% tax on, until you go into the next bracket (earning over £50,270).

Note: if you have a low income, you might get all of your interest tax-free anyway. Anything under £12,570 is tax-free, and if you earn under £17,570 per year, you’ll also benefit from the ‘starting rate for savings’, which is a £5,000 allowance where interest on savings is tax-free.

If you’d prefer to save within a regular savings account, here’s the best savings accounts.

An easy access Cash ISA means you can get your money back whenever you like – either instantly straight back into your bank account (current account), or within 1-2 days (depending on the provider).

With these accounts, the interest rate is typically ‘variable’, which means it can change over time (up and down), and this rate is up to the provider.

A fixed rate Cash ISA is where you ‘lock’ your money away from a certain period of time in exchange for a set amount of interest each year (a percentage of your savings).

Typically these are a higher interest rate than an easy access ISA, however they don’t have to be – it depends on a lot of different factors such as if interest rates are expected to increase or decrease in future.

These are great if you’d like the certainty of interest over a period of time. They can range from 1 year all the way up to 10 years, but the more popular ones are 1-5 years.

Note: you’ll always be able to get your money back when you need it, but there will probably be hefty fees if it’s before the end of the fixed rate period.

A notice Cash ISA is where you have to give the provider a set amount of time to arrange a withdrawal for you, for instance 30 days notice. You won’t be able to withdraw your cash instantly, but it’s not locked away for years like a fixed rate account.

These can typically range from 30 days to 365 days. And the rate can be fixed or more commonly, variable (meaning it can still change while your money is in the account).

You’re able to save up to £20,000 into all of your ISAs combined each tax year (if you have more than one). A tax year runs from April 6th to April 5th the following year. This limit is called your annual ISA allowance.

So, if you’ve got just one Cash ISA, you can save up to £20,000 into it. If you’ve got two, you can add say £16,000 into one, and £4,000 into another.

You can also have lots of different ISAs with different providers – you don’t just have to have one account of each type of ISA. For argument's sake, you could have 5 different Cash ISAs and pay into all of them at the same time if you want to.

Other types of ISAs include Stocks and Shares ISAs (for investing money), Lifetime ISAs (for saving for your first home) and Innovative Finance ISA (lending money to other people). There’s also a Junior ISA to save for your kids (if you have them, and has a separate allowance of £9,000 per year).

Note: you can only save up to £4,000 per year into a Lifetime ISA, and you can only save into one per tax year.

If an ISA is ‘flexible’, it means you can withdraw money from it, and then re-add it later on in the same tax year, without it counting as a new contribution – so it won’t affect your annual ISA allowance (the £20,000).

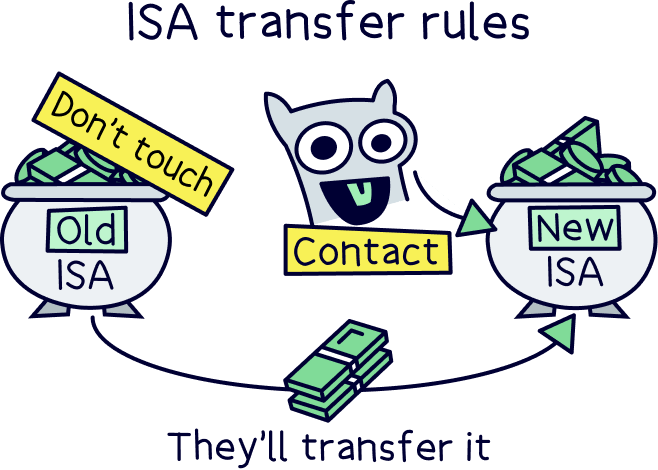

If you already have a Cash ISA, you can transfer it to another provider if you want to – if the new provider allows it. That means you can move all the money you have saved already to a top provider with a better interest rate, so you keep your money working hard for you.

It’s normally always a good idea to transfer your money if you have quite a bit saved. However, don't withdraw your money and then try and re-add it with an ISA account with another provider, as this will count towards your £20,000 annual allowance.

All you need to do is let your new ISA provider know you want to transfer an old ISA, called an ‘ISA transfer’.

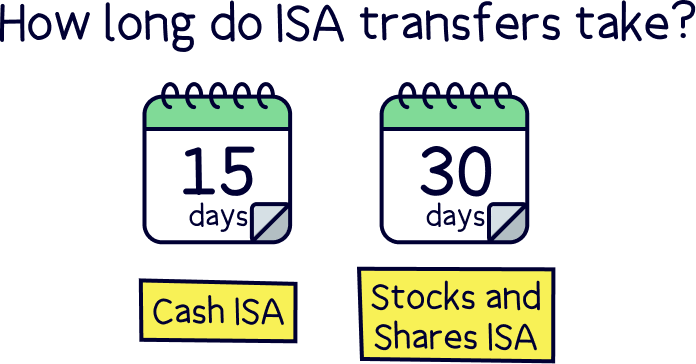

Your new Cash ISA provider will handle the whole transfer process – they’ll get the cash from your old provider, and sort all the admin behind the scenes. Your money will simply turn up in your new account after around 15 days.

Nuts About Money tip: you can also transfer different types of ISAs too. For instance a Cash ISA to a Stocks and Shares ISA (and vice versa).

Picking a Cash ISA can be simple, picking the best interest rate – and that’s normally the case, but have a think about your future plans first, such as what you are saving for and when you’ll need the money back, and which provider you’ll be saving with.

Having an easy access ISA with a great interest rate could be the best choice in the short term, but if you’re not planning on touching the cash for many years, you might want the certainty of a fixed interest rate (if you think rates might come down in the future), or vice versa (or even invest your money via a top Stocks and Shares ISA).

Nuts About Money tip: if you’re saving for your first home, you might want to consider a Cash Lifetime ISA, where you’ll also get a free 25% government bonus. How great is that?!

Also look at the features that each provider has too, such as if you’re able to manage the account online (or via an app), or if you need to go into a branch (in person).

All providers are different, and some are much more old fashioned – and some may only be suited to people near where they live rather than the whole of the UK (e.g. from a local bank).

Note: we are only showing Cash ISAs available nationwide, and ones you can open online.

Watch out for the starting figure with some Cash ISAs – they can be into the thousands of pounds (and even £10,000+).

If you think you’ll need the cash to spend, but not 100% sure if you will use it, you might want to consider a flexible ISA where you can take money out, and then re-add it again, without affecting your total ISA allowance (the £20,000 limit).

Some providers won’t let you transfer any existing ISAs into your new account – so check before you sign up and open an account. Some do of course!

Ideally, you don’t want your cash stuck somewhere where the service is poor, and it’s difficult to speak to someone, whether that’s on the phone or live chat (online). There’s lots of options for Cash ISAs, so you can pick one with great service and a great interest rate.

Cash ISAs are a great option to save your money – make the most of that tax-free saving!

However, if you’re not planning to spend the money any time soon and saving for the long term (over 5 years or more), you’ll likely benefit from saving your hard earned cash into a Stocks and Shares ISA, where your money can grow larger over time. Learn more with our guide to Stocks and Shares ISAs, and the best Stocks and Shares ISAs.

As a quick recap, you can save into as many different ISAs as you like, but you can only save up to £20,000 per tax year in total (although that’s pretty hefty!).

We’ve researched and reviewed all the top Cash ISAs out there and we’ve ordered them based on where you can earn the most cash over time, with a provider offering a great account and service, and where you’re able to create an account online easily. Here's where you can see the Best Cash ISAs (we'll scroll you up to the top of the page).

Happy saving!

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things savings, with many years of combined experience writing and talking about savings (and ISAs). Some of our team were top financial advisors. We understand the ins and outs of planning your finances well, how to communicate savings in an easy to understand way (we hope you agree), and of course, how to get the best savings rate for you.

More than 20 years of combined experience researching and writing about savings

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of savings companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible