Article contents

The best money market accounts (easy to open accounts that save your money into a money market fund), are Lightyear, InvestEngine and Trading 212. They’re all easy to use (online and mobile app), and have the top interest rates out there (and low fees).

Looking to save your cash and get one of the top interest rates possible? You’re in the right place – and that’s where money market accounts come in.

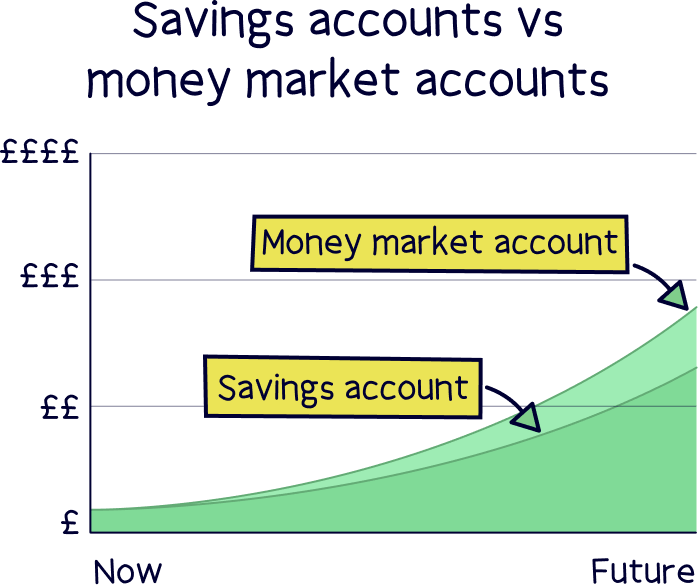

Money market accounts are fairly similar to a savings account you might get with a bank or other financial companies offering savings accounts – where you put money in, and earn interest in return…

But the difference is, with a money market account, your money is technically invested into an investment fund that stores all the cash in places that pay interest, or generate income, which could be with a bank or financial company with a top interest rate, or it could be things like government bonds that pay very high interest rates (effectively loans to governments).

They’re seen as very safe, and very popular for those looking for the very best rates for their cash (like lots of banks themselves, pensions funds, and lots of financial and investment companies).

We’ll cover everything in-depth just below, but if you’re just here for the best options, here’s our top picks:

Lightyear tops the list. It’s easy to use (with a great app), and a top interest rate.

Get up to £100 free share

Lightyear’s ‘high interest Vault’ offers one of the top interest rates out there. Behind the scenes it’s a fund managed by BlackRock, the largest financial company in the world.

You can add and withdraw money instantly to your cash account (in rare cases, your withdrawal will be processed the next business day), and there’s no minimum deposit. The fees are low, and already accounted for in the rate advertised.

The website and app itself are pretty awesome, and very easy to use.

Up to £100 welcome bonus. Promo code NUTS.

InvestEngine is great for investing in exchange-traded funds (ETFs). That’s all they do – and they're very good at it.

It's so low cost, there's in fact no InvestEngine fees at all (to make your own investments).

And for the experts to manage your investments, it's only 0.25% per year.

There's a great range of ETFs (over 700), and the app is pretty great too.

Get fractional shares worth up to £100

Trading 212 is a platform built for everyone in mind – there's over 2,000,000 customers! It’s great for beginners to get started, and perfect for experienced traders looking for more advanced trading options, such as CFDs, meaning you can trade with leverage (borrowed money), and trade the price going down (go short). There's all the trading tools you’ll need too, such as stop-loss and limit orders.

It’s one of the cheapest platforms out there with low fees when buying foreign stocks (currency conversion fee).

Platform experience: good

Device options: website & phone app

Support: 24/7

Stocks & Shares ISA: yes

Pension (SIPP): no

Range of investments: large

Stocks: yes

ETFs: yes

Fractional shares: yes

Crypto: no

CFDs: yes

Forex: no

Account fee: free

Cost per trade: free

Spread fees: yes (low)

Currency conversion fee: 0.15% on stocks, 0.50% on CFDs

• Low cost trading

• Huge range of investment options

• Hold and trade in multiple currencies

• Very low foreign exchange fees (0.15%)

• Offers an ISA

• Great mobile app

• Lots of resources to learn

• Awesome customer service

• No minimum investment

• Fractional shares

• No personal pension (SIPP)

Lightyear tops the list. It’s easy to use (with a great app), and a top interest rate.

There's lots of options when it comes to saving your cash in a money market account (and money market fund) – some options are easy to use and suited for the general public, and some are suited to professional investors and financial companies…

We’ve narrowed down our list to suit everyone, rather than just the professionals – so you don’t need much knowledge about investing and money market funds – but want to save your money somewhere to get a top interest rate.

Here’s the criteria to looked:

That’s quite a lot – but when it comes to your hard earned money, you want to know it’s in a great place, earning you that extra cash, and safe as possible.

All of the accounts we recommend above are all ones we recommend to our friends and family (and readers of course) – so you can be confident that whichever one you choose from our recommendations, you’ll be using one of the top options out there.

Our definition of a money market account is an account where you can simply add your money, and it’s automatically invested into a money market fund (below), earning you that high interest straight away.

To summarise, they bring the more complicated aspects of investing in a simple account, where all you need to do is add money.

You could think of them similar to a savings account from a bank – although they’re quite different behind the scenes (and you’ll often get a much higher interest rate with a money market fund).

They are also not provided by banks, but other financial companies (authorised by the Financial Conduct Authority to do so (more on that below)).

Separate to a money market account, and for those more professional investors, you are also able to invest through a stock broker, or investment platform, but you’ll typically need to make more decisions about which broker to use, which money market fund to use, and how to use the platform itself (plus any fees that might be applicable)...

So using a money market account specifically, can be much simpler, where all the decisions have already been made – you just add your cash and earn interest.

Note: although we’re calling the money you make ‘interest’, it’s technically called ‘yield’, which means the return from an investment (and typically measured historically rather than into the future).

Within a money market account, your money is saved into a money market fund…

A money market fund, or MMF, is a collection of people’s money that is pooled together (into what's called a fund), and invests in cash investments that often simply provide interest in return, and are able to turn back to cash very quickly (they have a focus on liquidity).

That sounded pretty complicated, but you can think of it like investing your money in places where it can get a high return for very little risk and easily exchangeable back for cash…

That could be places such as banks that pay the top interest rates for large sums, or it can be things like ‘cash equivalents’ and short-term debt securities, both of which can be things like Treasury Bills (lending money to governments in exchange for interest).

The aim of the funds are always to be a place for people and organisations to store cash when they don’t need it, and always be able to get their cash back quickly when they do – all while earning a top interest rate.

Money market funds can differ slightly across the world – depending on which country or region the fund is issued, such as the US or Europe, as the rules around them can be different. However, there’s typically similar types of MMFs – here’s a quick overview the three main ones:

These funds must have at least 99.5% of assets either in cash, government assets, or investment agreements that are guaranteed by the government. These are seen as the most safe type of MMF.

These have a wider range of cash equivalent assets, where the assets don’t need to be guaranteed by, or issued by a government, and can be issued by companies such as banks and other large financial institutions.

These can be low volatility (stricter rules on liquidity) or variable (with looser rules for liquidity).

These can hold lower quality assets, with less liquidity, such as longer duration maturity assets (takes longer for the fund to get its money back from a loan) – but still have to maintain strict rules to ensure investors can reclaim their cash back whenever they like.

Money market funds typically have some of the best interest rates you’ll find for your cash – that’s because they’re often designed for financial institutions who don’t want to pay hefty hidden bank fees to store their cash (like most savings accounts). MMFs can effectively bypass most fees that are paid to a bank for storing cash, and get a top rate directly.

Note: there will often be fees included within the fund itself (typically not very much), and within the money market account itself (the company providing the account).

This interest rate isn’t guaranteed like it is with a typical savings account with a bank, as they work a bit differently (although banks can typically change it anyway if it’s ‘variable’).

With a MMF, you effectively earn money from investments, so can only look at the expected return from your money (or historical return), based on the cash investments within the fund, rather than agreeing a set interest rate with a bank. However, you can get a pretty good estimate of what you’ll be getting…

Note: this is why it’s called yield, rather than an interest rate.

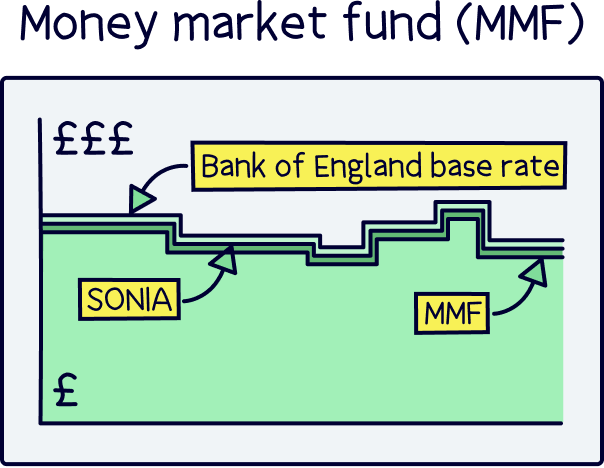

In the UK, most of the top MMFs will aim to achieve a return near to something called SONIA, which is the Sterling Overnight Index Average (can also be called SOIA). This is the average of the interest rates that banks and other financial companies pay each other to borrow money cash (and measures only borrowing for one day, and unsecured lending – so no borrowing linked to an asset).

Although it’s not specifically the base rate set by the Bank of England (the interest rate banks get for storing their cash with the Bank of England), the SONIA rate is typically very very close to it (just under by a tiny fraction) – and it’s also measured by the Bank of England.

So, if you see a money market fund is tracking SONIA, or using SONIA to compare their fund against a benchmark, you can assume the rate you’ll get will be around the current base rate set by the Bank of England (which is pretty much the highest possible rate you can get).

However, not all MMFs are the same, and the interest rate (yield) is different across them all – it all comes down to the assets within the fund itself, which are made up to suit the goals of the fund to suit different investors…

We’ve looked at where you can get the very best interest rate in our top picks above – suited for the general public, and quick access to your cash.

Note: there can be different benchmarks across the world, such as the Lipper Institutional Money Market Fund Average, which is used in the US (among others).

MMFs are typically seen as very low risk, and suited to save cash, but they’re not entirely risk free. Here’s the two main risks:

If the main interest rate of a country is changed, such as the Bank of England base rate, this will affect the interest rate you’ll get (the yield of the fund) – this can go both up and down.

As MMFs aren’t fixed interest rates (they are variable), such as a fixed rate savings account, this can happen almost immediately. Whereas if your savings were in a fixed rate savings account, you’d continue to get the same rate until the end of the agreed period (the term).

An MMF suits those looking for a high interest rate but also quick access to their cash, rather than locking it away for a set period of time.

Not all of the money within an MMF is held as cash, there can be lots of different types of cash investments that may not be readily available if needed (to the fund itself) – for instance if all the investors were to take their money out at once, there could be issues repaying everyone (very unlikely).

There can also be issues if the fund is forced to sell some of the investments because the investment itself may have changed, such as receiving a lower credit rating than the MMF allows – this can mean the price it receives from selling the investment isn’t the best price, and results in a small loss to the fund.

These risks are managed by the fund manager, and a range of different investments are often used, with ongoing risk management. MMFs are seen as very safe investments overall but it's good to know all the information!

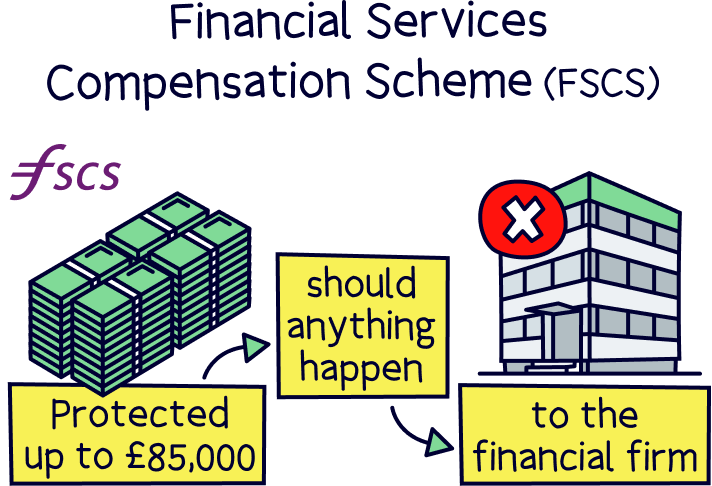

In the UK, there’s something called the Financial Services Compensation Scheme (FSCS), which provides up to £85,000 in compensation if a financial company holding your money goes out of business (e.g. a bank).

However, this doesn’t apply to MMFs and money market accounts, as your money is within the investment fund itself, rather than say a savings account with a bank, and so FSCS isn’t really needed.

If your money market account provider were to go out of business, your money would still exist within the MMF itself, which is all in your name, and only you can access it – and this would be returned to you, or transferred to a new provider (you would be notified).

If the actual fund provider were to go out of business, and if it’s based in the UK, you may be covered by FSCS protection (or equivalent in the relevant country). However the funds themselves are ring-fenced, and the cash isn’t accessible by the provider for their own business needs – the fund would be closed down and your money would typically be returned to you in this scenario.

Money market funds can have a range of minimum deposit amounts before you can start saving into them (some can be into the £10,000s). However, lots are low (such as £1), and all the best money market accounts we’ve showcased above have a low minimum (from £1 to £500), so you can start earning that high interest rate without needing a massive budget to start.

Money market funds are a very popular option, especially for those familiar with investing, and if you’re looking for the very best place to earn the most from your cash, but access when you need it, it’s probably an MMF.

However, if you’re not comfortable with using a money market fund just yet, there are alternatives…

An easy access savings account is where you can simply deposit your cash with a bank or financial company and they’ll give you interest in return – and being easy access, it means you can get your money back when you like (normally within a day or two).

The interest rates can be good, but expect slightly under an MMF – and the interest rates are variable, which means they can change up and down, set by the financial company (typically when the Bank of England changes the base rate up or down).

You can learn more about these with our guide to the best easy access savings accounts.

With a Cash ISA, the interest you’ll make is tax-free! And with an easy access account, you’ll be able to withdraw your cash when you need it to.

You can save up to £20,000 per tax year (April 6th to April 5th the following year). And this is an annual allowance that applies as a total to all of your ISAs – for instance a Stocks and Shares ISA too (where you can invest tax-free).

For that reason, you might want to use your annual allowance for investments within a Stocks and Shares ISA (depending on how much you are investing each year), rather than cash savings – as investments are likely to grow much more over time compared to cash savings (so longer term you can benefit from more tax saved).

You can also buy MMFs within a Stocks and Shares ISA too (if you want to), which would provide income tax-free.

The main difference with a savings account and a money market account is that with a savings account the bank or financial institution is giving you the interest themselves, and the money is held entirely with them.

This can be a good thing, as in the UK you’ll be covered by the Financial Services Compensation Scheme (FSCS), which protects your money up to £85,000, should the financial company go out of business and not return any of your cash.

The downside is the rate is decided by the financial company, and they need to make profit on your cash too – so the interest rates can be lower than a money market account, and you need to shop around for the top rates.

Nuts About Money tip: if you are saving more than £85,000, you might want to spread your money across various different accounts.

With a money market account, your money is managed by the fund manager (the company behind the fund), and they’ll typically aim to get the highest rate possible in line with the rules of the fund (e.g. only government backed assets).

As it’s not a savings account, you don’t get FSCS protection, so there’s potentially a higher risk. However, it’s not necessarily needed, as money is held in cash and cash equivalents within the fund itself, often with very large financial companies – who cannot access the cash for themselves.

Alongside that, MMFs need to go through rigorous checks with regulators such as the Financial Conduct Authority (FCA) in order to operate (the people who make sure financial companies are looking after you and your money) – and are continually monitored.

That’s it for the best money market accounts – hopefully not too complicated (ok maybe just a bit!).

Money market accounts are some of the best places to save cash – easy to use, and you can get one of the best interest rates out there. The amount of interest you can get between a money market account and a savings account with your bank account can be huge!

We typically recommend using a money market account if you’re comfortable to – you can get access to your cash straight away, and they’re really not complicated to set up and use either (just add cash and you’re away).

They are slightly different to a savings account, as your cash is earning interest in a different way to a savings account with a bank – but that’s why the interest rate is typically higher. Your cash is pooled together with lots of other people, and put in places that earn high interest – which can be cash, or it could be things like short term loans to governments (like the UK government).

You also won’t get FSCS protection (compensation up to £85,000 if a savings account provider goes out of business), but your money is separate from the money market account provider, and all in your name, and would be returned to you (or transferred) if they were to go out of business.

We’ve put together all the best money market accounts we think are great for our readers – all above – so we hope we’ve helped put you on the right path to earning more cash from your money.

All the best saving!

Lightyear tops the list. It’s easy to use (with a great app), and a top interest rate.

Lightyear tops the list. It’s easy to use (with a great app), and a top interest rate.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things savings, with many years of combined experience writing and talking about savings (and ISAs). Some of our team were top financial advisors. We understand the ins and outs of planning your finances well, how to communicate savings in an easy to understand way (we hope you agree), and of course, how to get the best savings rate for you.

More than 20 years of combined experience researching and writing about savings

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of savings companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Lightyear tops the list. It’s easy to use (with a great app), and a top interest rate.