Article contents

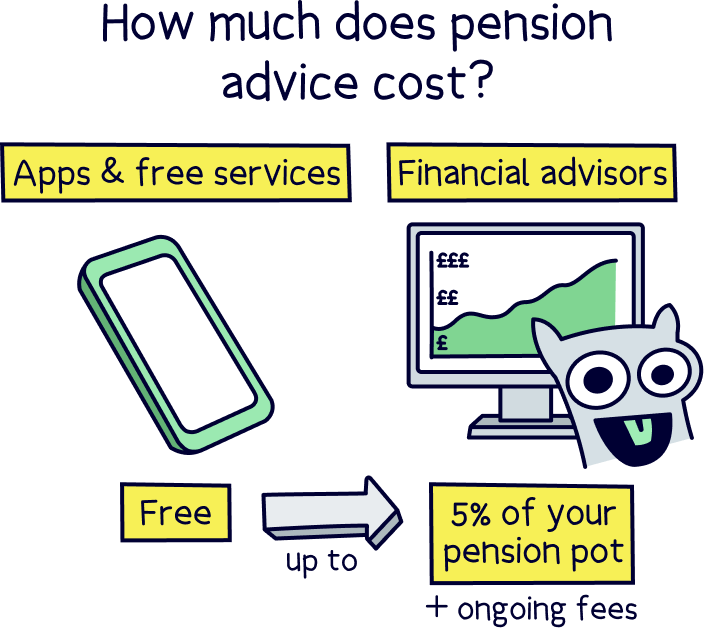

Good news! There’s lots of great options for free pension advice these days. There’s a free government scheme called Pension Wise if you’re over 50 – or even better, modern pension providers provide guidance on pensions and their services, all for free! If you want more traditional financial advice (face-to-face), expect to pay up to £350 per hour or an initial fee (around 3% of your pension) and ongoing charges (2.14% on average, per year) for them to manage things for you (ouch).

Need some advice for your pension but a bit worried about the cost? Don’t worry, you’ve got lots of options for help and advice in the UK. There’s even a range of free pension advice services.

Overall, pension advice can cost anywhere from being free, to 5% of your pension pot (ouch!), and then ongoing fees (with a financial advisor).

But don’t fear, using the right free advice is often an excellent idea, and their experts can look after your pension too (for a much cheaper management fee).

These days, pensions are a bit easier to manage, thanks to a few Government changes over the last 10 years or so, and because technology has finally caught up with pensions! (Kind of.)

Lots of the best pension providers (pension companies) are online now, making them easy to use, and the technology behind the scenes means you can move your pensions to a new provider super easy too (and for free).

Check out PensionBee – their experts can explain the ins-and-outs of pensions and their pension options for you to make the right choice.

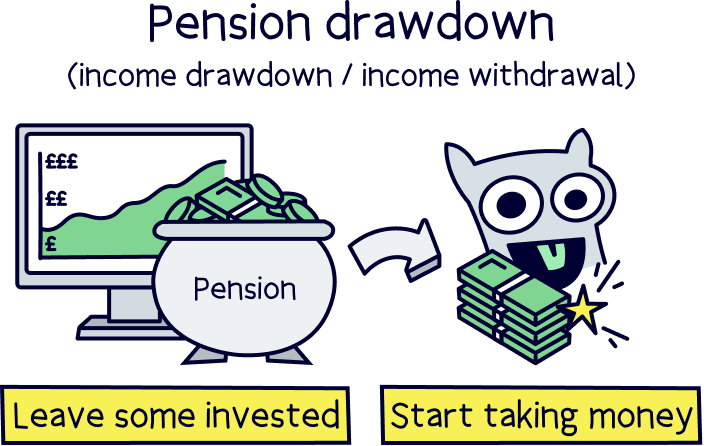

You also have the option to withdraw some of your money directly from your pension after 55 years old (57 from 2028), while keeping the rest saved in your pension so it can keep growing (this is called pension drawdown, and it’s becoming very popular).

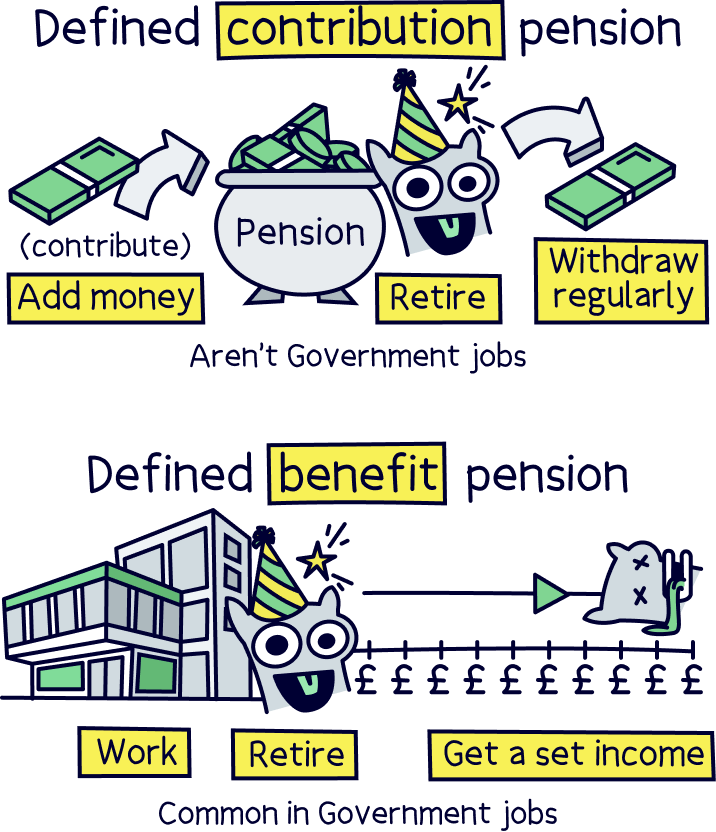

Getting a bit technical now, we’re talking about defined contribution pensions – which are ones you pay into from your work salary, or directly via a personal pension (a pension you set up yourself, usually online), rather than defined benefit pensions, which are more common in government jobs and the NHS, where you get a certain pension income when you retire based on how long you’ve worked there, and your salary (sometimes a final salary pension).

Anyway, back to pension advice cost – with these new, modern pension providers, you can also get free guidance on pensions, and how their pension service might be able to help you. Whoop!

They can explain all the finer details about their service, so you can be informed to make the right decision for you, which can save you a small fortune (and often for a similar or maybe even better outcome than going to an expensive financial advisor).

Let’s run through all your options:

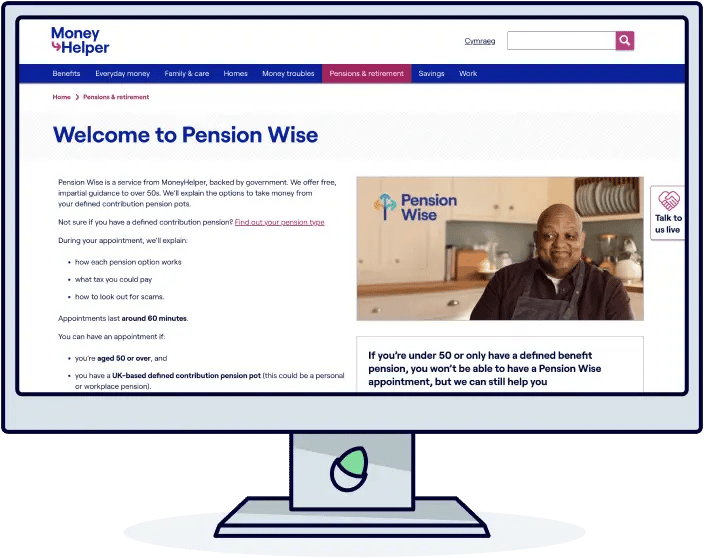

If you’re over 50, you’ll be able to get a free appointment with Pension Wise, which is a friendly service provided by MoneyHelper, which is backed by the Government (and in turn part of the Money & Pensions Service. Confusing right?).

Essentially it’s a government scheme to help the UK understand finances better.

You’ll be able to chat with an expert advisor for pensions advice, for up to 60 minutes – they won’t necessarily tell you what to do, or do anything for you, but will give you an overview of all your options. It’s not the same as getting financial advice.

To book your consultation, head over to the Pension Wise website.

Note: they can only provide advice on defined contribution pensions, rather than defined benefit pensions (so no pension from jobs such as the civil service, police, teachers or the NHS).

Remember those modern pension providers? PensionBee is one of the best. It’s easy to use, has low fees and a great track record of growing pensions over time.

There’s a small range of easy to understand pension plans, and all you need to do is pick one you prefer (such as socially responsible (helping the environment)), sharia-compliant, or use their standard plan, and your pension is all set up and ready to go.

And as a bonus, you can move any or all of your old pensions across too – they’ll handle everything for you.

You’ll also be able to keep your pension with PensionBee after you retire or want to start withdrawing from it, and simply withdraw as and when you like (e.g. monthly). Again, this seems simple but with pensions, this option hasn’t been around for long.

Anyway, what’s great about PensionBee in this instance is that their customer service is excellent – you get a dedicated account manager when you sign up.

Before you sign up, you can simply chat online, or call them on the phone, and have a chat with a pension expert to run through all of your options.

They can’t give financial advice, which means a personal recommendation of what to do, but they can give you all the information you need to make an informed decision that’s right for you.

Their service is completely free (e.g. the chat over the phone), they'll just charge a fee (taken from your pension) if you decide to use them – just like your pension now (if you have one). It’s also one of the cheapest pensions out there.

Can you tell we’re big fans? Anyway, head over to the PensionBee website¹ to learn more and get started. We've also secured a deal where you'll get £50 added to your pension when you sign up with Nuts About Money.

If you just want to chat on the phone first, their number is: 020 3457 8444 (remember to come back to Nuts About Money if you choose to use them and get the free £50).

Similar to PensionBee although a little more complicated, Moneyfarm is another modern pension provider – all online (and over the phone). However, instead of just doing pensions, they do general investing too (for instance a tax-free ISA).

They’ve got a team of friendly experts to give you guidance on pensions over the phone (called retirement planning), and it’s all free!

It’s not financial advice, so they won’t give you a personal recommendation, but they’ll give you all the information you need to make your own informed decision.

You can book a free appointment on the Moneyfarm website¹.

Again similar to PensionBee, you can transfer over any old pensions you have too, and they’ll handle everything for you.

If you choose to go with Moneyfarm for your pension, just like with all pensions, you’ll pay a fee as part of your pension plan, and Moneyfarm is also one of the lowest cost providers.

Bestinvest is an online investment platform provided by a large financial advice company called Evelyn Partners.

It’s a bit more complicated than PensionBee and Moneyfarm, as the experts don’t manage your pension for you, you’ll have to make your own investment decisions.

However, they do offer basic financial advice, where they’ll run through your personal circumstances, what you’re looking to achieve with your pension, and any specific questions you might have, and then give you a personal recommendation of what to do.

It’s not free, it’s £295, which is fairly reasonable – however, they’ll only provide you with advice relating to the investments on the Bestinvest platform, rather than general advice about what you could do with your pension.

They also offer a free version of this, but don’t provide the personal recommendation, so it’s more guidance on how to get set up on the Bestinvest platform.

To learn more, or book in a call with an expert, head over to the Bestinvest website¹.

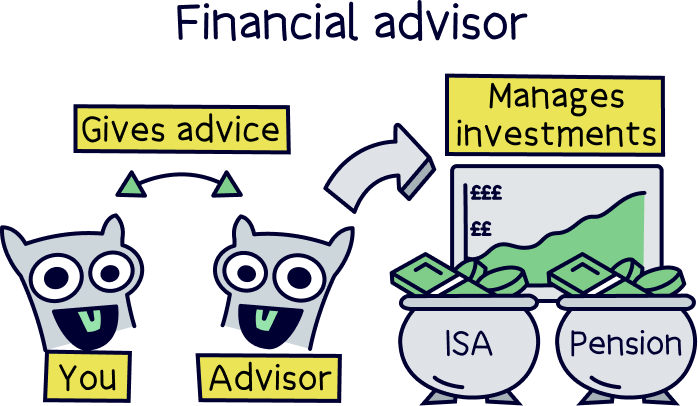

Finally, you could opt to go with a financial advisor – these are qualified experts and will run through your personal circumstances and understand what you’d like to do as part of your retirement planning, answer any questions you might have, and then give you their recommendation on what to do.

This can be done online, video chat and even face-to-face (in their office or at your home).

Normally their recommendation involves the financial advisor managing things for you. You’ll transfer your pension to them, and they’ll invest it to achieve your goals.

However be warned, some are pretty slick salesmen, and it’s not always in your best interest to do this, or use them. Don’t decide on the spot, go home and research and have a think before committing, as it can be hard and expensive to move your money away afterwards.

Now, there’s options with which advisor to use, and this could be an independent financial advisor, which means they can choose investments from a range of different investment companies to put together the right mix of investments for you (or often, they’ll have another company manage the investments on their behalf).

Or, it could be a ‘restricted’ advisor, which means they’ll only recommend and use their own investments that their company manages. This isn’t necessarily a bad thing, but it can mean your money might not be in the very best place to grow over time (as their investments may not perform well). An example of this is St James’s Place, the largest financial advice company in the UK.

That was pretty complicated right? Anyway, with financial advisors, they’ll either charge an hourly fee, which is anywhere from £150 to £350 per hour (the higher fees are usually in London and more experienced advisors). This is for ‘one-off’ advice.

Or, they’ll charge a fee to manage your investments on an ongoing basis (if you decide to go with them), this is often 3% of your pension as an initial payment (but can be 5%), and then anywhere from 0.50% to 1.50% per year as an ongoing basis – and there will also be fees within the investments themselves (taken directly from the investment), which can vary but often around 0.50-1%.

The average cost of using a financial advisor is 2.14% per year according to the Financial Conduct Authority (FCA) – the people who manage the financial services industry.

Note: you might get offered a free consultation, but this isn’t the financial advice bit, it’s often simply an overview of their services. Personal advice is a paid service.

So, using a financial advisor is your most expensive option by far – and really, it’s only worth opting for if you have large sums of money (e.g. £50,000+, but often much more). Or, if you didn’t get the help you needed from the previous options (such as PensionBee¹).

Or, a good idea if you would simply prefer to have a full assessment of your personal circumstances and a personal recommendation of what to do, and then have the advisor manage things for you. (Perhaps more than just pension advice, but tax and investing too.)

If this option is for you, you can find a financial advisor in your local area with Unbiased¹, or learn more with our guide to financial advisors.

Unbiased is a great online service to help you find expert financial advisors who can help with your pension.

It’s very popular, with over 10 million customers, and pretty much the go-to-place to find pension advisors local to you.

All advisors are fully vetted, qualified and have years of experience.

You’ll be able to chat on the phone, video call, or visit in person (depending on the advisor).

It’s free to use the service, you’ll pay the advisor directly if you choose to use them (fees vary per advisor and service you’d like).

Check out PensionBee – their experts can explain the ins-and-outs of pensions and their pension options for you to make the right choice.

Note: if you do have a defined benefit pension, and you think you might want to transfer it, and if the estimated value is over £30,000, a financial advisor is your only option (this is by law and it's the only way to do it).

Although pensions seem complicated, underneath they’re really quite simple, and most people have the same goal – to grow their money sensibly all ready for a comfortable retirement – and the modern pension providers do exactly that, and really well.

If you’ve got a defined benefit pension (for instance a pension from a government job) then things change a bit, as you might have some great benefits, and it’s not worth transferring it. You'll have to speak to a financial advisor if you do have one of these and are considering moving it (if the estimated value is over £30,000).

Otherwise, with a ‘regular’ pension (defined contribution pension), you can typically transfer it to any other pension provider you like, as long as it’s not a pension with your current job – you can only move pensions from old jobs. This is called pension consolidation.

It’s often a good idea to transfer your pensions to a single pot, with one provider, that way all your pensions are together and there’s no chance you’ll forget them when the time comes to retire (it happens more than you think!).

And, you can potentially benefit from lower fees, an easy to use service, with a great mobile app and a great record of growing pensions over time.

With that in mind, we recommend checking out PensionBee¹, for all of those reasons – and they can give you free guidance over the phone from their experts.

Or, check out Moneyfarm¹, they’ve got free expert advice too, and a great modern pension provider overall.

And with both, you can keep your pension invested even after you retire, and simply withdraw your pension as and when you like, called pension drawdown – which is becoming a great option for many people. If you’d like to learn more about that, here’s our guide to the best pension drawdown providers.

The alternative to drawdown is an annuity, which is where you exchange your pension (or part of it) for a guaranteed income for the rest of your life, or a set number of years (e.g. 20 years). They were often your only option until drawdown came along in 2015 from government changes. If you want to learn more about that, here's our guide to annuity vs drawdown.

So, there you go – you don’t really need to shell out for expensive financial advice unless you really want to, have large sums of money, or have very complicated circumstances. The days of expensive financial advisors in stuffy suits are on the way out, and modern pension providers with great service are becoming very popular.

All the best with your pension and for a happy retirement!

Check out PensionBee – their experts can explain the ins-and-outs of pensions and their pension options for you to make the right choice.

Check out PensionBee – their experts can explain the ins-and-outs of pensions and their pension options for you to make the right choice.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Check out PensionBee – their experts can explain the ins-and-outs of pensions and their pension options for you to make the right choice.