Article contents

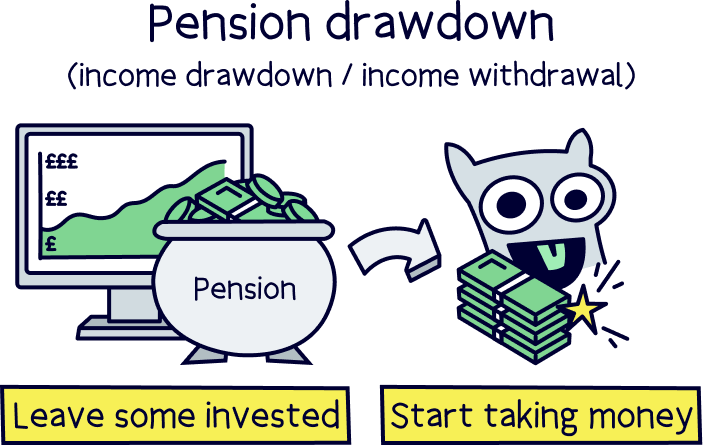

A drawdown pension (or income drawdown) is where you withdraw money from your pension (e.g. monthly), while leaving the remaining money in your pension to keep growing over time (in retirement). It’s a popular way of getting a pension income, while having the flexibility and control over your pension pot (e.g. how much to withdraw and when).

Planning for retirement around the corner? Or just planning far ahead? You’re in the right place. Here’s everything you need to know about a drawdown pension (also called income drawdown), and whether it might be the right option for you.

Pension drawdown is where, when it comes to retirement (or even before retirement), you simply withdraw money from your pension as and when you like (e.g. monthly), while leaving the rest of your pension where it is so it can keep growing. You ‘drawdown’ from your pension.

Note: you’ll need to be over 55 years old to start withdrawing from your pension (and 57 from 2028).

Sounds pretty simple right? It’s becoming very popular these days, and was only possible since 2015 when the Government changed the law to allow people to have more freedom over their pension.

It’s got some very good benefits, which we’ll run through in detail below. Before that, if you’re only here to find out which the best pension drawdown providers are, well, here they are:

Where the experts will continue to grow your pension while you withdraw.

We recommend PensionBee, it’s easy to set up and use, low cost, with simple, easy to understand drawdown options.

Get £50 added to your pension

PensionBee is our recommended provider – they’ve thought of everything.

Their 5 star rated app (and website) makes it easy to set up and use. You can open a brand new pension, or transfer your existing pensions across (they’ll handle all the paperwork).

Simply pick from an easy to understand range of pension plans, and that’s it, the experts manage everything from there.

It’s low cost, with one simple annual fee. The customer service is excellent, and you’ll get a dedicated account manager for any questions you might have.

And, when the time comes to retire, withdrawing from your pension is easy too.

You can also use them if you're self-employed or a company director.

Moneyfarm is a great option for saving and investing (both ISAs and pensions). It's easy to use and their experts can help you with any questions or guidance you need.

They have one of the top performing investment records, and great socially responsible investing options too. Plus, you can save cash and get a high interest rate.

The fees are low, and reduce as you save more. Plus, the customer service is outstanding.

We recommend PensionBee, it’s easy to set up and use, low cost, with simple, easy to understand drawdown options.

Where you make the investment decisions.

0% fees

InvestEngine is a super low cost investment platform allowing you to save and invest within a pension and an ISA, and with a great range of investment options.

There's no fees for an account, and no commission to buy and sell investments. And there’s a wide range of investment options, with over 700 investment fund options (ETFs only).

It's more than just low cost though, it’s pretty easy to use, there’s some great features to help you invest, and the customer service is excellent.

Minimum deposit: £100

Best for: those looking for a low cost platform with a range of fund options

• Easy to use

• Very low cost

• Commission-free

• Great range of ETFs

• Great customer support

• Only ETFs (but a wide range)

• No financial advice

AJ Bell is well established, with a good reputation.

It's one of the cheapest SIPPs out there (charging a low annual fee).

There's a huge range of investment options – pretty much every investment out there (including both funds and shares).

The customer service is excellent too.

Overall, it's one of the best options for a SIPP.

Offers available

Interactive Investor is a well established company, and very popular.

Instead of paying a percentage of the investments in your account (like other investment companies), you’ll instead pay a fixed fee per month – and it’s pretty low, starting at just £5.99 per month for a pension (SIPP).

This makes it one of the cheapest SIPP providers out there, especially if you have a fairly sizeable amount within your pension (e.g. over £30,000).

On top of that, there’s a huge range of investment options (e.g. shares and funds) – one of the largest.

It's easy to use, and the website and app are great. The customer service is excellent too.

A great choice overall.

We recommend PensionBee, it’s easy to set up and use, low cost, with simple, easy to understand drawdown options.

If you're a bit unsure about pensions and would prefer to speak to an expert, check out Unbiased¹ – it's a free service to find pension experts (financial advisors) in your local area.

If you’re over 50, you can also speak to a pensions expert for free with Pension Wise, a service provided by MoneyHelper (a Government scheme).

On the surface, pension drawdown is simple. It's a normal pension where you have the option to simply withdraw from your pension pot as and when you need it, or when you’d like to (e.g. setting up a monthly payment to your bank account).

Note: pension drawdown can also be called income drawdown, flexible drawdown, and flexi-access drawdown – they’re all the same thing.

Nuts About Money tip: You can estimate your yearly retirement income based on your pension pot with our retirement income calculator.

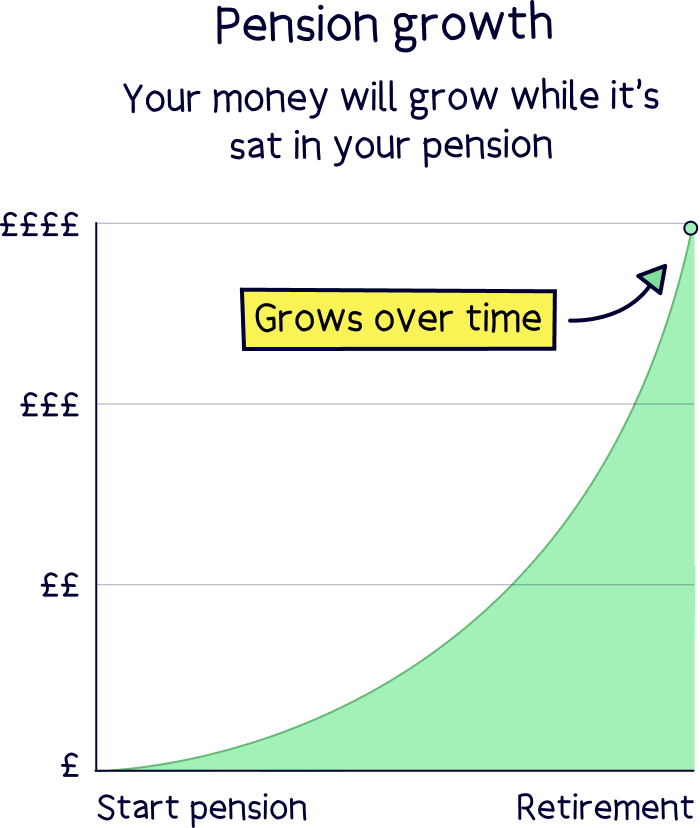

Your pension pot (all the remaining money you have in your pension) stays within your pension account, and so it can keep growing over time.

If you weren't aware, your pension (right now) is invested in order for it to grow over time – this is all handled by the experts at your pension company, and you may have the option to pick which pension plan you’d prefer (where the money is invested).

This is exactly the same with a drawdown pension. You’ll be able to choose which pension plan your money is invested in, from a few easy to understand options (with help on hand) – which is often one that provides a stable income (think like interest payments within a savings account), with very low, or no ups-and-downs in value over time (but it doesn't have to be).

Less complicated than you thought right?

You’ll also be able to start withdrawing from your pension at age 55 (57 from 2028), although it’s often a good idea to keep it in your pension so it can keep growing until you do eventually retire.

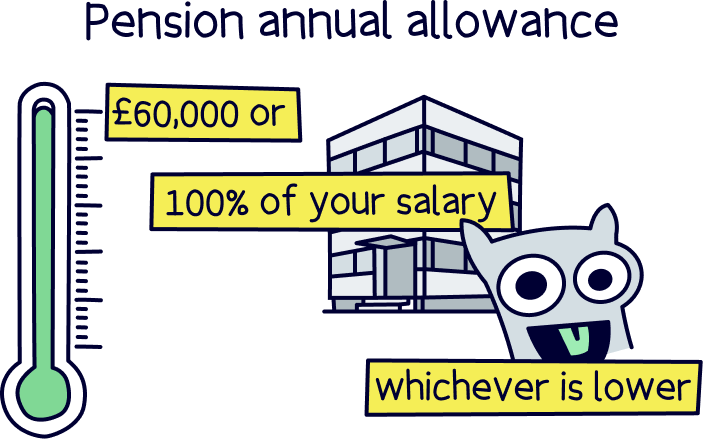

It's important to note, that when you start withdrawing it, the amount you’ll be able to save into it will reduce to £10,000 per year – before that, you can save up to £60,000 per year, or your annual salary (whichever is lower), as a total across all your pension pots.

Note: the new lower limit is called the Money Purchase Annual Allowance (MPAA).

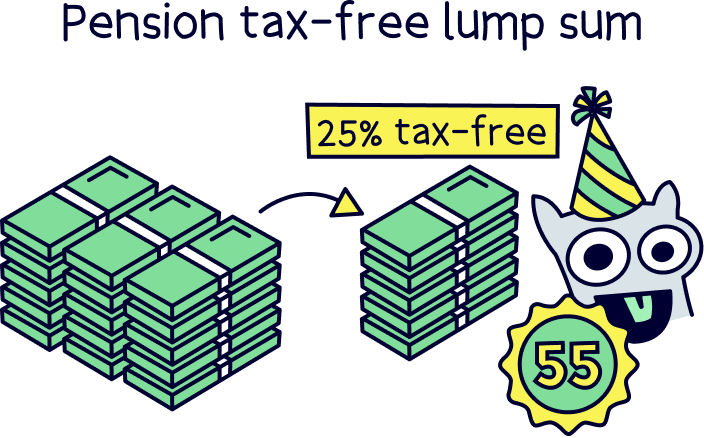

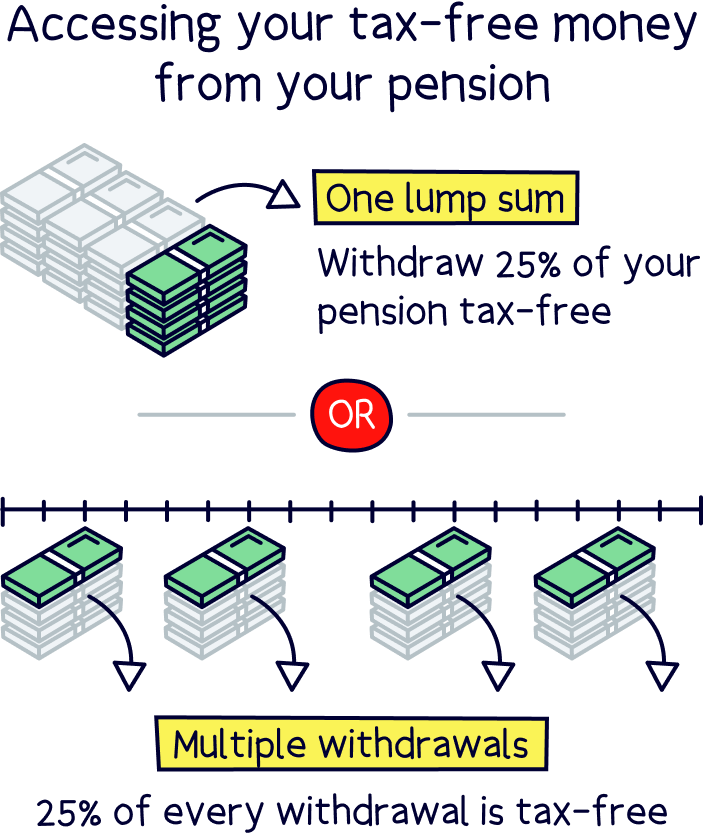

As a great benefit, you'll be able to withdraw 25% of your pension completely tax-free, and take it as a tax-free lump sum if you want to. Or, make regular withdrawals, and 25% of each withdrawal will be tax-free.

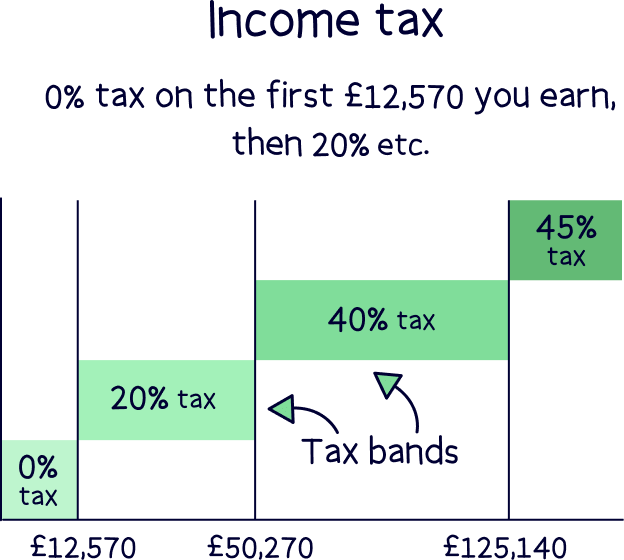

You’ll pay Income Tax on the remaining 75%, just like your salary now. So, how much tax you’ll actually pay will depend on your income at the time (which is all automatically handled for you by your pension provider).

You’ll still have the personal allowance of £12,570 before any tax is paid, just like your job now too.

There is a limit on how much will be tax-free however, which is £268,275. So, if you're lucky enough to have more than £1,073,100 in your pension, only £268,275 will be tax-free. Although that’s a pretty hefty pension!

Note: the tax-free lump sum is technically called the pension commencement lump sum (PCLS). If you take this tax-lump sum, you can still buy an annuity (a guaranteed income) – but we're jumping the gun, more on those later.

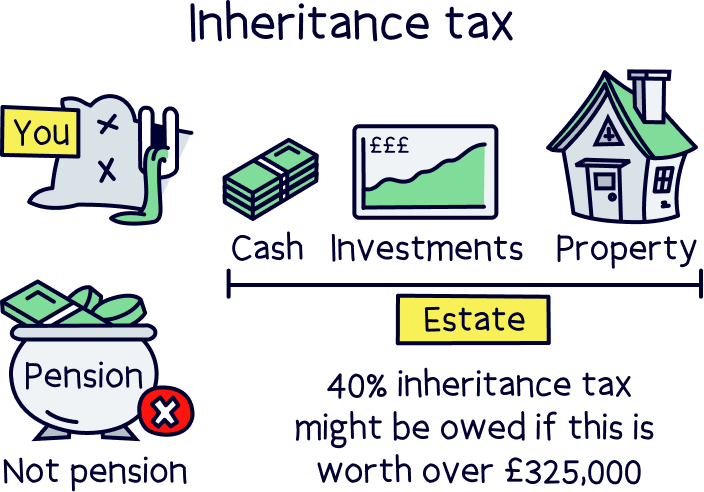

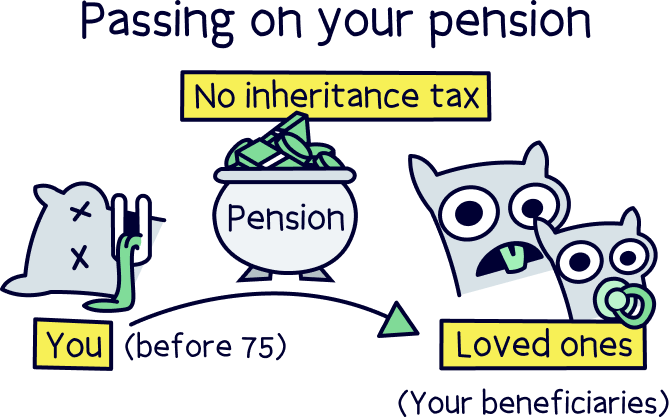

When you sadly pass away, your private pension savings will still remain, and will pass to your family (or whoever you decide).

Amazingly, your pension savings won’t count towards Inheritance Tax, as it doesn’t count as part of your ‘estate’, which is all your money and possessions added together. Pensions remain completely separate.

If you pass away before the age of 75, there will be no tax to pay at all on your pension. After 75, whoever receives your pension may have to pay Income Tax on what they withdraw (the same tax as their salary now – we’ve got the tax rates listed below).

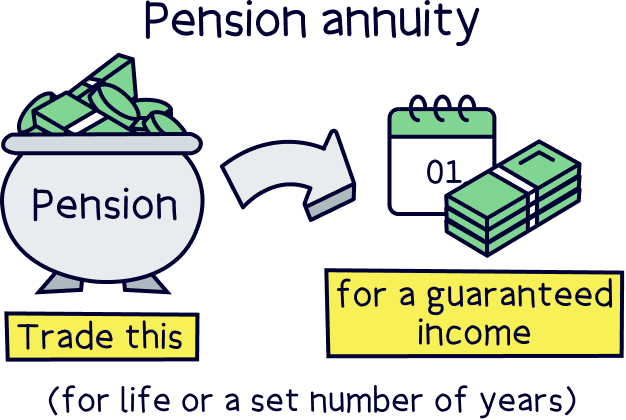

The alternative to pension drawdown is using your pension pot to buy a pension annuity (so you trade in your pension). This is a guaranteed income for the rest of your life (or a set period of time, e.g. 20 years).

They’re a great way to have certainty of a regular income when you retire, and traditionally, they were your only option (before 2015, when the pension rules changed).

The amount you’ll get each month as a pension income will all depend on the size of your pension pot when you retire (and buy an annuity), but your health and age also play a part.

If you’re older, for instance 70 rather than 60, you’ll get bigger monthly payments (as you're likely not to live as long). And if you’re in worse health, or a smoker or overweight, you’ll likely get bigger payments too (for not so great reasons).

Note: the amount you’ll get is sometimes called an ‘annuity rate’. And, an annuity is technically a form of insurance, so you may see it called insurance in some places.

Your annuity can also increase each year, often in-line with inflation (the price of things like food going up), however this often means the income you’ll start with is much lower (this is called your starting income).

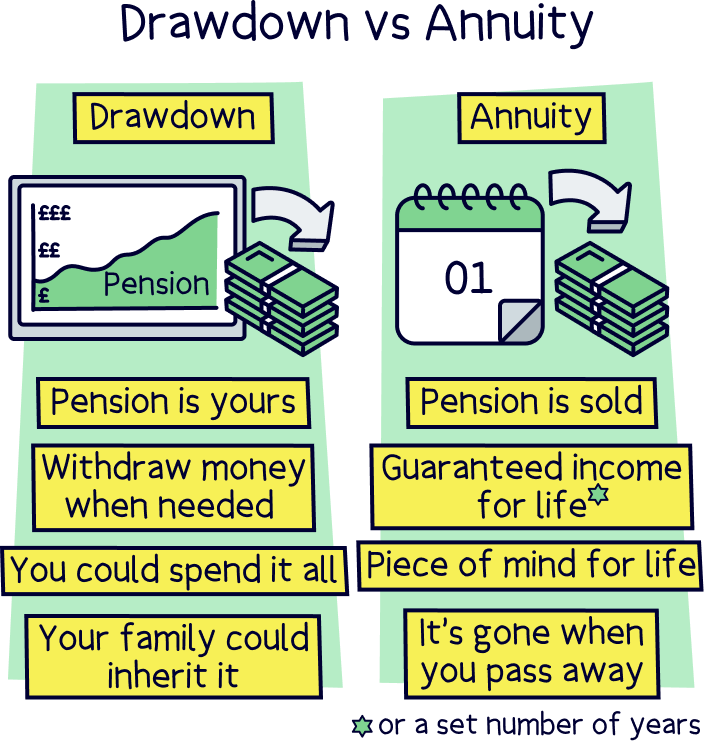

There are some downsides though (hence why pension drawdown is becoming more popular). Once you decide to take an annuity, you can’t change your mind after, there’s no refunds. With pension drawdown, you can later decide to buy an annuity.

And, when you sadly pass away, there’s no money left over for you family – the annuity provider (company) keeps it all. Even if you pass away just a few years after buying the annuity. With pension drawdown, your pension pot remains, and will be passed on to whoever you decide, there also won’t be any tax to pay if you pass away under the age of 75 (with drawdown).

It is possible to get a joint pension annuity, which is where your annuity income will pass to your partner when you pass away – but the monthly payments will typically start lower overall. This is called a survivors annuity. For one person only, it’s called a single life annuity.

If you’re keen to learn more about all the differences, and which might be best for you, here’s our guide to drawdown vs annuity.

There’s no definitive answer here unfortunately. It all comes down to your personal circumstances and what you prefer, and what’s important to you.

If having the certainty and guarantee of a regular income each month is your highest priority, and you’re happy to trade in the whole or part of your pension pot for it, then a pension annuity is probably best for you.

If the flexibility of withdrawals, and having a pension pot for emergencies or perhaps to support loved ones later on (such as with their first home), then pension drawdown might be a better option for you. It also provides the assurance your family will get something when you pass away.

If you do think pension drawdown is for you, check out PensionBee¹ – it’s easy to use, low cost and a great record of growing pensions over time – and of course, offers pension drawdown (not many providers do).

You’ll also get a dedicated account manager to help you with any help you need. And, as an extra bonus, you’ll get £50 added to your pension for free with Nuts About Money.

Nuts About Money tip: it's worth taking the time to have a real think about what the benefits and disadvantages are of each, in relation to your own circumstances.

If you do want expert help, speak with a financial advisor (you can find great ones local to you with Unbiased¹), or chat with a pension expert from Pension Wise for free (if you’re over 50).

There’s another less popular alternative that's worth mentioning, which is to take your pension out all in one go, or to take it out as a series of lump sums, instead of setting up a regular retirement income (e.g. monthly payment), like pension drawdown or an annuity.

Getting technical, this is called uncrystallised funds pension lump sum (UFPLS), and instead of having a 25% tax-free lump sum initially, every lump sum would have 25% tax-free, and the remaining 75% would be liable for Income Tax (so depends on your total income at the time how much you’d actually pay).

It’s best to speak to a financial advisor if you are considering this, as it can get complicated.

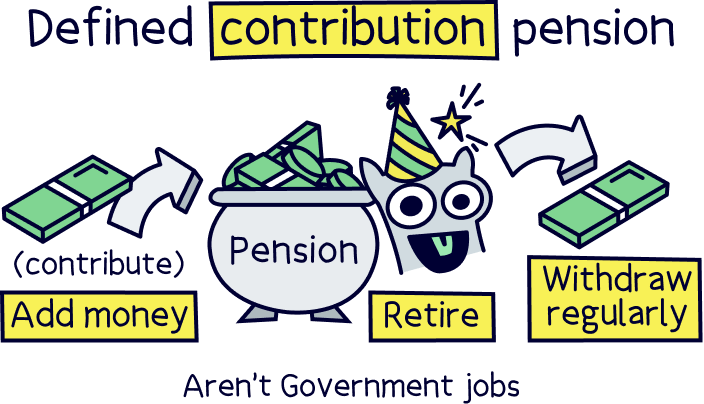

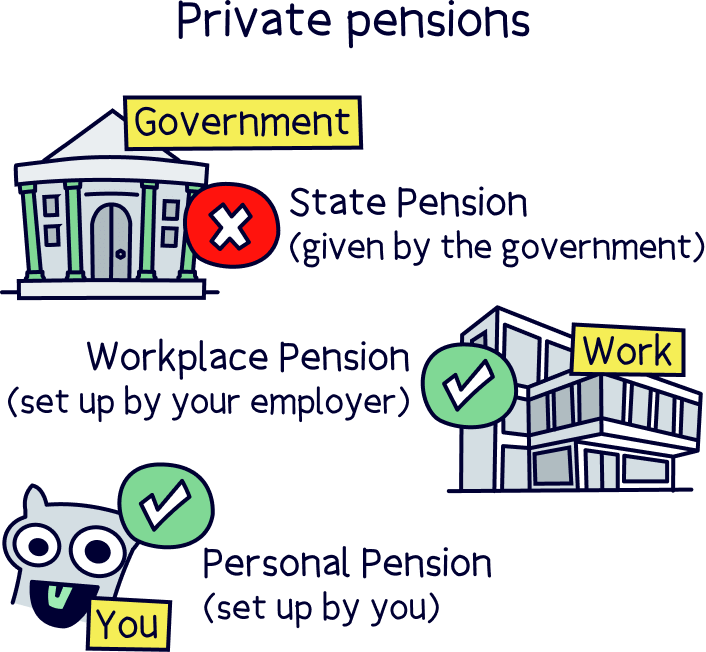

By the way, we’re talking about defined contribution pensions, rather than defined benefit pensions.

Defined contribution pensions are where you save into your pension throughout your life, and this builds up into a big pension pot which has a financial value (e.g. a £100,000 pension pot). You can then decide what to do with this pension pot (e.g. annuity vs drawdown).

These are common in most jobs that aren’t Government jobs.

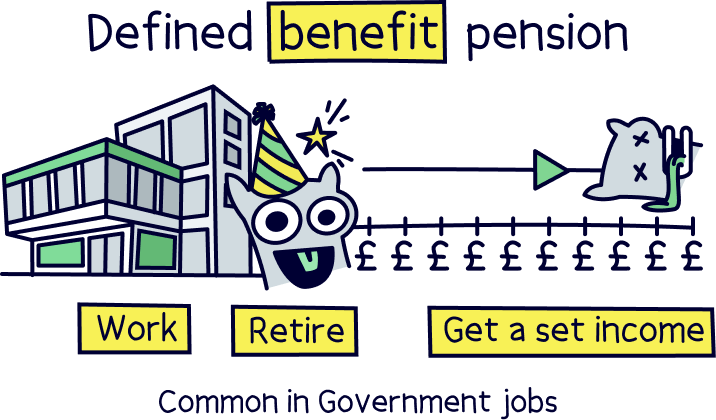

A defined benefit pension is where you get a set retirement income after you retire, for instance, a final salary pension, or average salary pension – and the amount you get is determined by how long you’ve worked somewhere, and how much you earned. These are common in Government jobs and places like the NHS.

You can transfer your defined benefit pension to a defined contribution pension sometimes, although it’s often not a good idea as the benefits (the regular income) can often be pretty great. It’s best to speak to a financial advisor if you are considering this.

If you’re keen to get cracking setting up a drawdown pension, here’s how to do it in 5 easy steps…

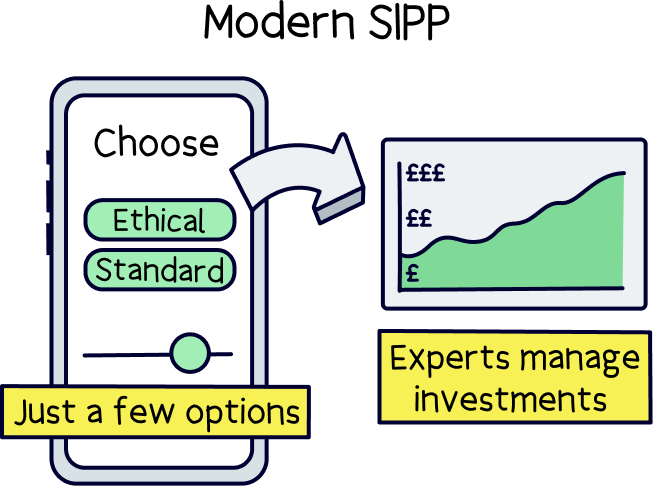

This decision should be a pretty simple one, for most people simply let the experts handle the investments for you after you retire (and the common choice).

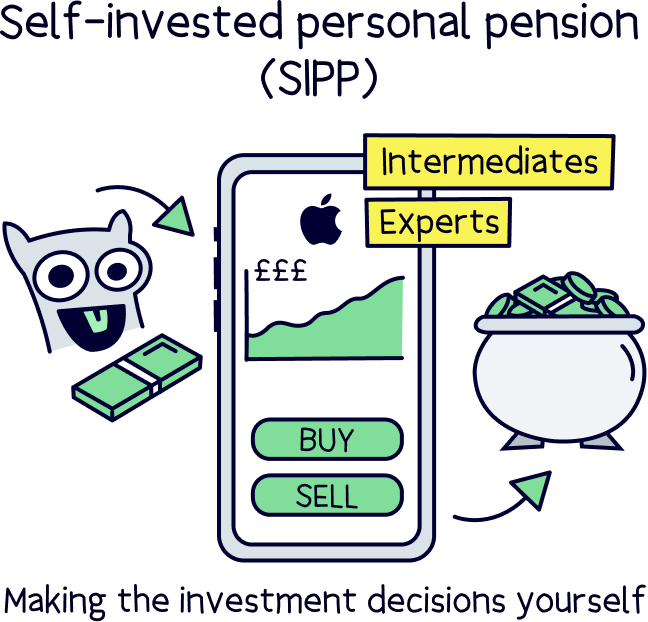

If you’re an experienced investor, you could opt to manage the investments yourself (by getting a self-invested personal pension (SIPP)), although there’s not too much benefit, the experts know what they’re doing and have pension plans designed exactly for those who have retired and want drawdown pensions.

Anyway, with drawdown pension providers, they typically have pension plans suited to pension drawdown (usually around 3 easy to understand options) – we’ll cover these just below.

By the way, most modern pension providers will be classed as a ‘self-invested personal pension’, or SIPP. This simply means a pension that you open and manage yourself (e.g. how much to withdraw, and which investments to make). That’s the same whether the experts are handling things, or you’re making your own investment choices.

The alternative is a workplace pension, which is what you’ll likely be familiar with, which is a pension from your work if you are employed.

When you retire and want to access money from your pension, you likely won’t be able to keep your pension exactly where it is.

Your provider will move you over to a self-investment personal pension (only if they offer drawdown), or you’ll need to transfer it to a brand new pension in order to start withdrawing from it (which means you can pick a great one).

Next, it’s time to pick the pension provider.

We’ve done the hard work for you, and reviewed all the best pension providers (that offer pension drawdown)…

If you’re opting to let the experts handle things, we recommend checking out PensionBee¹, it’s easy to use, low cost, and a great track record of growing pensions over time. And, you’ll get a dedicated account manager to help you if you’d like it.

If you’re keen to learn more about making your own investments, check out or guide to the best SIPPs (self-invested personal pensions).

Right, once you've picked your pension provider, or have an idea of which one you want to use, now it’s time to pick the right pension plan – that’s where your money will be invested within your pension, and can also be called pension funds.

It can be a complicated topic, so to help you make the right pension, the Government has devised 4 common options for retirement, called ‘Investment Pathways’.

The Investment Pathways are:

And then pension providers are able to match up their pension plans with one of these 4 options, making your pension plan choice quite easy.

For instance, if you’re looking to take pension drawdown, you’ll likely be looking at option 3 (a long-term income), and so simply pick the pension plan from the provider that matches that.

For instance, with PensionBee¹, a popular pension provider, here’s their plans they’ve matched to the Investment Pathways:

For pension drawdown, you’d simply pick option 3, ‘4Plus’, which aims to grow your money steadily over time.

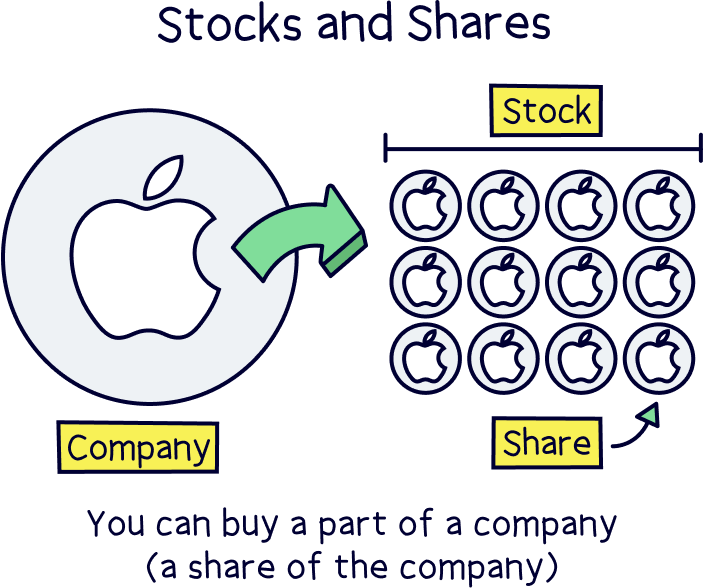

Note: equities means shares in companies (a share represents the ownership of the company), and fixed income means investments that provide a regular income (kind of like a salary), and are considered safe, such as loans to Governments and large corporations in return for interest payments.

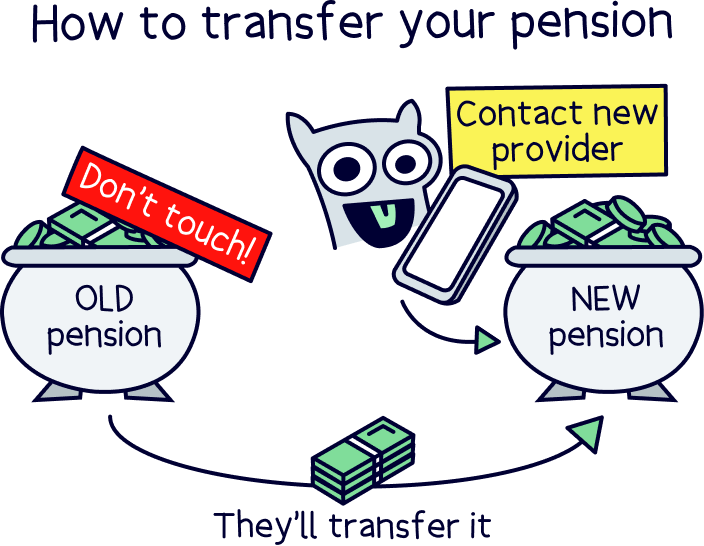

Now it’s time to get your pension money over to your new provider so you’re all set to start withdrawing from it when you’re ready to.

This step is easier than it sounds! Your new pension provider will handle everything for you. All you need to do is let them know where your old pensions are (which pension company), and they’ll take care of the rest.

Your pension(s) should all turn up in your new pension after a few weeks (sometimes a few months).

If you’re not quite sure where your pensions are (don’t worry, you’re not alone), use the Government’s pension tracing service, or Gretel, a free service to find lost pensions.

That’s it! All that’s left to do is finally retire. You’ve earned it.

Your pension is all set to give you a regular income – and keep growing (invested) over time too. And, it’s there if you need a bit more later on (like a one-off withdrawal).

As a bonus too, your pension provider will actually handle all the tax payments for you too – it works just like your job now, all taken before it arrives in your bank account. Handy right?

And don’t forget that 25% tax-free lump sum if you want it.

Note: you may find your first pension payment is taxed at a higher rate (called emergency tax). This is because your pension provider won’t know the right tax code for you until after the payment is made and they get it from HMRC. Don’t worry, it will resolve itself in the following payments.

How much will you actually pay on your pension income then?

Well your pension income counts as ‘taxable’ income, so it all depends on how much your total income is at the time and you’ll pay exactly the same rate of Income Tax as your salary now, which is:

So, you’ll still get the personal allowance of £12,570 before any tax is paid, and then pay tax on anything above that.

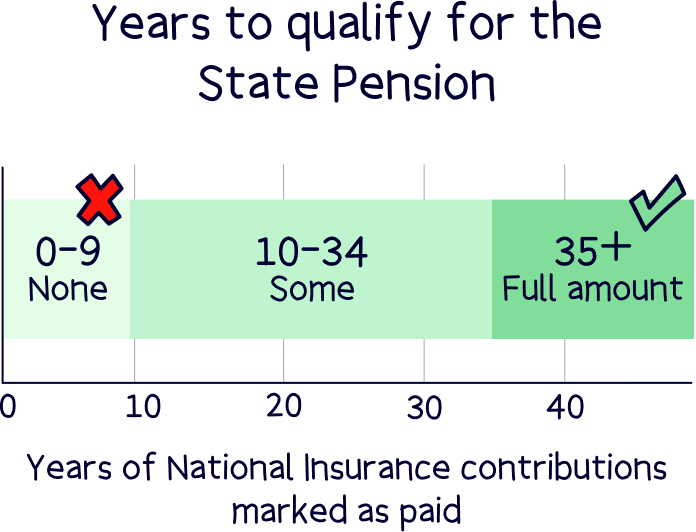

However, if you’re getting the State Pension, which is the Government pension, this goes towards your income too, and you’ll get if you’ve paid at least 10 years National Insurance contributions, but 35 years for the full amount.

Currently, the full State Pension is £11,973 per year, or £230.25 per week – so it’s not a lot.

If you’re not planning to retire soon, keep saving as much as you can, as you’ll need a big pension pot to tide you over in retirement these days.

In fact, you’ll need a substantial amount to provide a comfortable retirement. We won’t scare you here, but to learn more, here’s our guide to how much you’ll need in retirement.

You can estimate your total pension pot at retirement and your yearly retirement income with our pension calculator.

Yep, you can still pay into it if you want to (for instance if you’re still working). However, withdrawing from it typically triggers the ‘money purchase annual allowance’ (MPAA), which means the amount you can add to it reduces.

Instead of your maximum annual limit being £60,000 or your yearly salary (whichever is lower), your limit will reduce to £10,000 per tax year (April 6th to April 5th the following year).

All private pensions (that’s pensions in your name, rather than the Government pension), are separate to all of your other money and property, which is often called your ‘estate’.

Only your estate counts towards any Inheritance Tax, which is a tax your family might pay if your estate is over £325,000 (the tax rate is 40%).

Your pension is its own special thing, and can be passed to anyone you specify (called your beneficiary, and can be more than one person).

If you sadly pass away before the age of 75, there’s no tax to pay. If you pass away after 75, whoever receives the money may pay Income Tax on it, just like their salary (tax rates above).

Although if you take the 25% tax-free lump sum out, and still have the cash when you die, that will count towards your estate.

And there we have – everything you need to know about drawdown pensions (also called income drawdown). Hopefully less complicated than you thought...

Simply put, pension drawdown is where your pension pot stays exactly as it is, within your pension account, and you withdraw money from it as, and when you need it (e.g. monthly withdrawals as a pension income).

You will have to find a great provider who does offer pension drawdown (as not every provider does), and a pension plan designed for pension income (if you want stable growth). But that’s easy to do – your new provider will handle all the paperwork, all you need to do is let them know where your old pensions are.

As a recap, our top recommendation is PensionBee¹ – it’s easy to use, low cost, a great record of growing pensions over time, and you’ll get a dedicated account manager to help you with any questions.

And here's all our top private pensions.

The alternative to pension drawdown is pension annuity, where you trade in your pension for a guaranteed income for the rest of your life (or a set number of years). You can learn more about the differences with our guide to annuity vs drawdown.

And that’s all there is to it – all that’s left to do is enjoy retirement!

We recommend PensionBee, it’s easy to set up and use, low cost, with simple, easy to understand drawdown options.

We’d love to hear from you, and it will help others too.

Edward Savage is a leading expert on money, with a background of 8 years working in financial services in London, has a business, accounting and finance degree, runs an investing community, and teaches people about money. He writes about all aspects of personal finance, including pensions, investing, mortgages and insurance.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things pensions, with many years of combined experience writing and talking about pensions and retirement, and some of our team were top financial advisors with professional pension qualifications. We love writing about pensions, they’re pretty much the best thing you can do for your future.

More than 20 years of combined experience researching and writing about pensions

Qualified team (APFS - Advanced Diploma in Financial Planning)

A wide range of pension companies researched and reviewed, and a transparent review process

We follow a strict editorial code to ensure you get the best information possible

We recommend PensionBee, it’s easy to set up and use, low cost, with simple, easy to understand drawdown options.