Review contents

Nutmeg is a good digital wealth manager. Their experts will handle everything for you. However, the investment track record isn’t the best, and they’re one of the most expensive. There’s better options out there (we’ll run through them).

Nutmeg. How does it work? Are they any good? Is my money safe? And are there better options? Let’s find out.

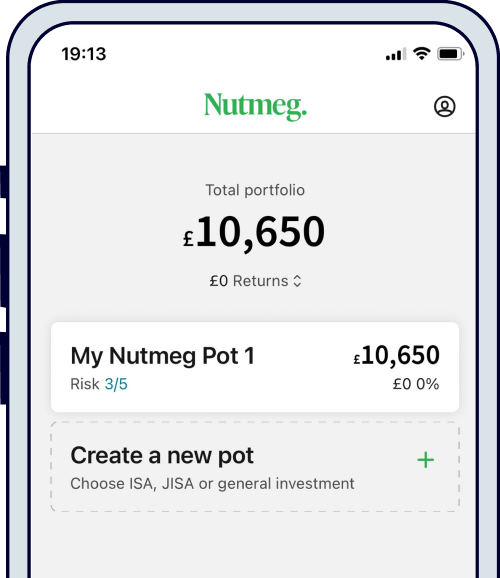

Nutmeg is one of the larger ‘digital wealth advisors’ in the UK. That means a mobile phone app and website that invests your hard earned money for you – putting your savings to work and hopefully making you more money as you go through life. If you don’t do this already, you should be!

All you have to do is simply choose the type of savings account you’d like. These range from a Junior ISA to a pension and everything in between (explained below). Add your money, select an investment style (again, more on that later), and done! Sit back and watch your money grow.

But is it right for you and are they the best out there? Let’s find out.

Spoiler: we think there's some great alternatives out there. Check out Beach¹ if you're looking for an easy to use app, where the experts manage the investments (open an ISA and a pension). They'll find lost pensions too.

If you’re only looking to save into a pension, check out PensionBee¹, they’re 5* rated, easy to use, have a great investment record and low fees (and get £50 added to your pension for free).

Your capital is at risk wherever you choose to invest.

Check out Beach. It's an easy to use app where the experts manage the investments. You can open both an ISA and a pension. The customer service is excellent too.

Nutmeg has been around for a while now, since 2012 in fact. And have over 150,000 customers. Pretty popular! With a combined amount invested of over £2 billion.

They started with a mission to make investing a ‘clear and straightforward experience’. We love that. And it’s what Nutmeg built with their app and website. You’ll always be able to see how your investments are performing, and have the flexibility to change how and where your money is invested.

In 2021, Nutmeg was bought by the American bank J.P. Morgan Chase, and all the investments behind the scenes at Nutmeg are with J.P. Morgan.

So, by being a customer you won’t be supporting a growing UK business anymore, you’ll be funding a mega-corporation. They also don’t have the best reputation when it comes to investing and climate change (they’re one of the biggest investors in fossil fuels).

If this concerns you, check out Beach¹. They're from the UK, and similar to Nutmeg, but easier to use and great customer support.

Yep, it’s a good option for beginners, mostly because you don't need any previous knowledge or experience in investing. It’s all managed for you by professionals, you can just sit back, relax and watch your money grow.

However, you do need to add a minimum of £500 to open your account (£100 for Lifetime ISAs).

If you want to start with less than this, check out Moneybox¹, they’re great too, and you can start with just £1. Here’s our Moneybox review to learn more.

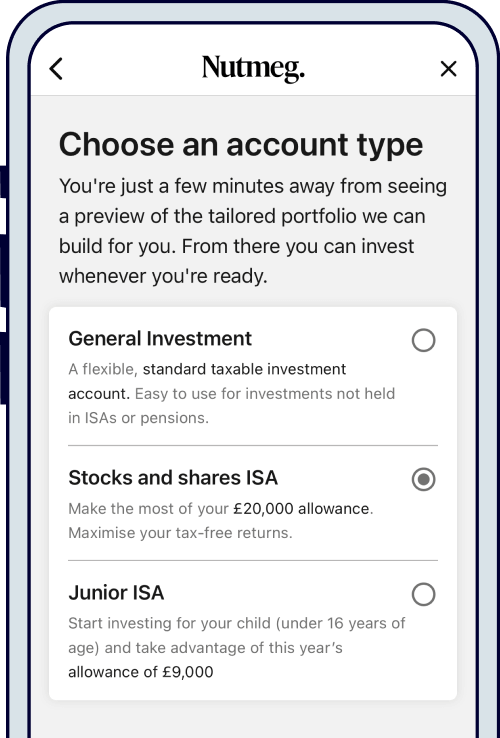

Nutmeg offer the full range of investment account options in the UK, which are:

You’ll always be able to see how your investments are performing and you get the flexibility to change how and where your money is invested, and how much risk you want to take (more on this later).

Let’s dive into each one briefly:

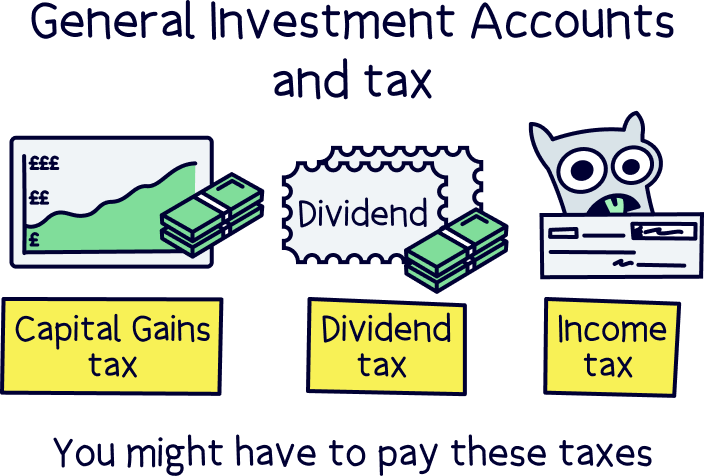

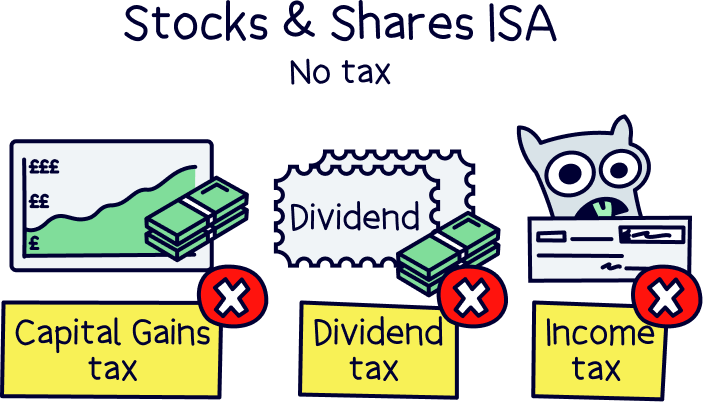

This is a ‘normal’ account with no tax-free benefits. You’ll pay Capital Gains Tax on any money you make over £3,000 (if you sell), and you’ll pay 10% if you earn less than £50,270 per year (in income), or 20% if you earn more. This is from all of your investments, not just with Nutmeg (except investments in an ISA).

Here’s where to learn more about General Investment Accounts.

This is the most popular account for investing. You can invest £20,000 per year (your ISA allowance), and all the money you make in the future is completely tax free!

We’ve got a great guide to Stocks & Shares ISAs if you want to learn more.

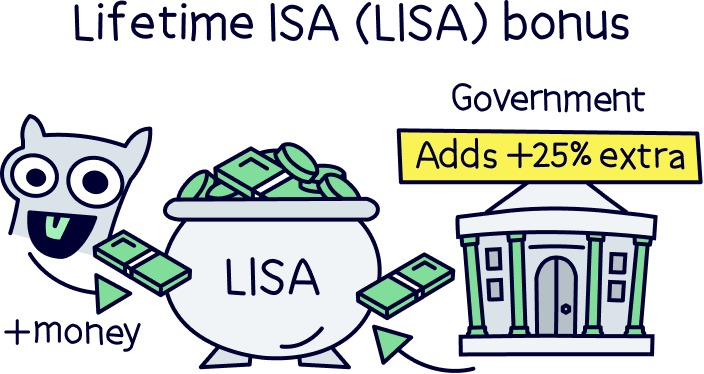

This is Stocks & Shares ISA on steroids! Not only is everything you make completely tax-free, but you’ll also automatically get a 25% bonus from the government on all the cash you put in.

There is a £4,000 per year limit though, and it’s only for buying your first home, or saving for later in life (not as a replacement for a pension).

If you're interested in getting a Lifetime ISA, check outMoneybox¹. They've got one of the highest interest rates out there, the app is easy to use, it’s low cost overall (free to save cash), and the customer service is excellent. Here's where to learn more about the best Lifetime ISAs.

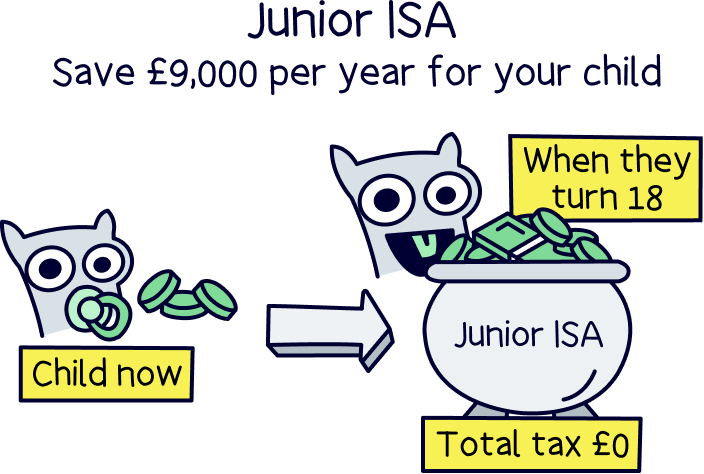

These are perfect for saving for your children. You can save up to £9,000 per year, completely separate from your own £20,000 ISA allowance. It will all be in your kids name, and they’ll get access to it when they turn 18.

Check out the Best Stocks and Shares Junior ISA, and learn more about Junior ISAs here.

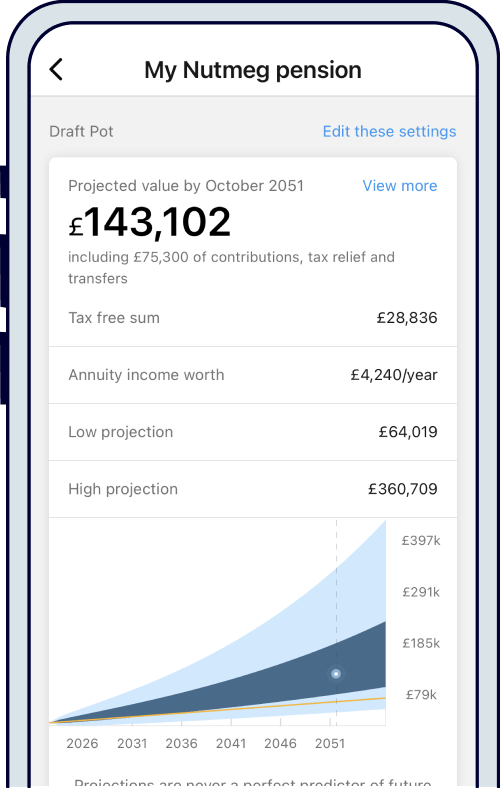

You can create a personal pension with Nutmeg.

A personal pension gives you control over where your pension money is invested, and you get a bonus from the government of 25% for everything you pay in.

And if you’re a higher rate tax payer, earning more than £50,270 per year, you can claim 40% back on some of it too (and 45% if you’re an additional rate taxpayer).

Nuts About Money tip: if you’re just looking to open a pension, check out Beach¹, the fees can be cheaper depending on your pension pot size (roughly anywhere from £7k to £250k), and has an easy to use app, and pension plan managed by BlackRock (one of the largest investment companies in the world).

it’s also worth checking out pension-specific providers. Pensionbee¹ is one of the most popular, has a great track record and lower fees than Nutmeg. Here’s our Pensionbee review to learn more.

You can also learn more about pensions and find all your options with our guide to the best personal pensions.

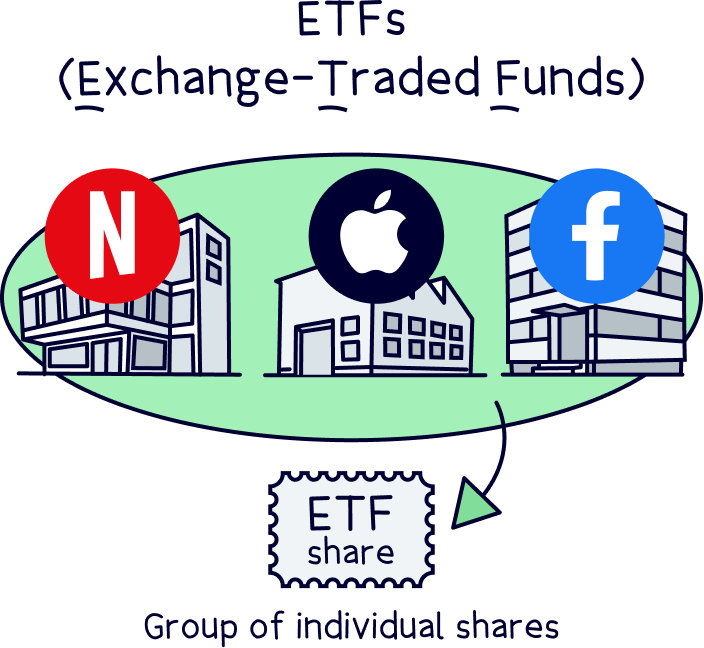

Nutmeg invests your money in exchange-traded funds (ETFs). This means your money is invested in a wide range of investments (such as shares of a company), all grouped into a single investment, a ‘fund’. This helps manage risk and makes it much safer than investing directly into one or a few companies.

Which ETFs your money goes into is decided by the experts at Nutmeg, who then use technology to buy and sell investments. Your money is managed by safe, human, hands. Well, all except for one investment style, where the robots reign! (More on that below).

ETFs are low cost, transparent and flexible. So, you get low investment fees and transparency using Nutmeg too (and all the best robo-advisors).

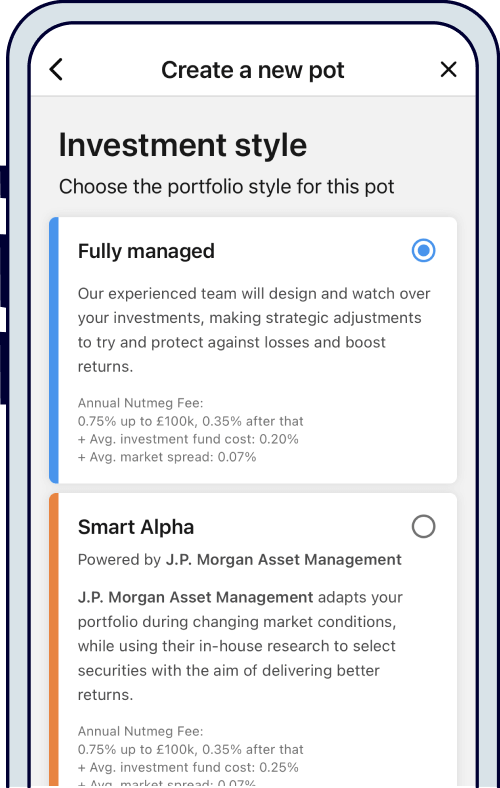

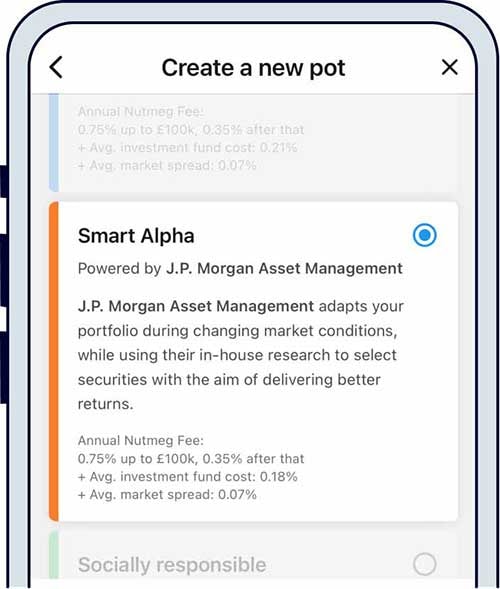

There’s four ‘investment styles’ you can pick from when opening your Nutmeg account.

It's how you’d like to invest your money on the platform (app or website), so your options are:

This investment style is where the experts at Nutmeg are looking at news, data and analysis to manage your money day-to-day and decide where to put your money.

So this is where it gets a little confusing. ‘Alpha’ in finance is a measure of how much an investment has ‘beaten the market’ i.e. how much it has beaten investing in all of the companies within a stock market (called an index).

What this means for Nutmeg, is the Smart Alpha investment style aims to return more than just investing in an ETF that tracks the stock market. They do this by following an investment strategy by J.P. Morgan’s global research team.

This is very similar to the ‘fully managed’ investment style, with experts selecting which investments (ETFs) to put your money into, however the ‘robots’, aka the technology, will decide when to make changes to the investments, rather than the human experts. And as a result, this style is actually cheaper for you.

Conscious about the environment and climate change? We are too! This investment style will only invest in environmental and socially responsible businesses, so no fossil fuels or tobacco companies, or anything that has a negative impact on the environment or society.

However, just because there’s one option to be socially responsible, doesn’t mean Nutmeg, or their parent company, J.P. Morgan Chase is socially responsible. In fact, they're one of the biggest investors in fossil fuels out there.

If this concerns you, check out Beach¹, their investment plans aim to reduce carbon emissions, so you can feel good your money is having an impact too.

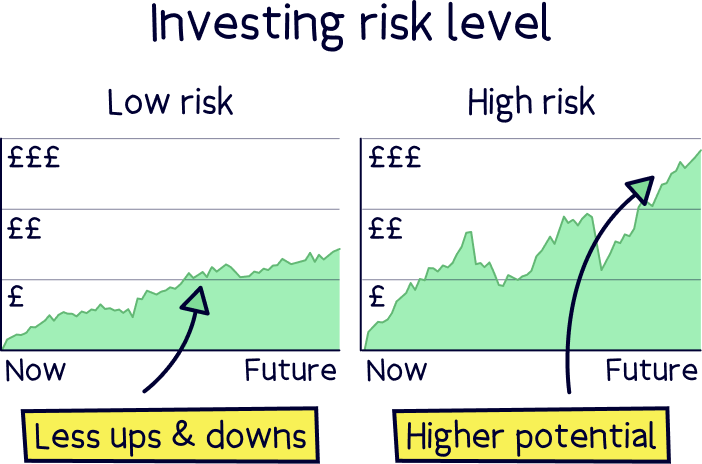

So the above is about investment styles, but within these styles, there are comfort levels of risk (meaning how you feel about keeping your money safe vs risking some for more money) you can choose from, on a scale of 1-10 (10 being most risky).

Typically, as in almost all investments, the higher the risk, the higher reward you can expect over a long period of time. Although it doesn't mean you will actually get a higher return, it depends on the success of the investments.

And with a lower risk option, there will be fewer up-and-downs, but your money is likely to grow less over time.

It’s up to you which risk level you choose, however it’s often dictated by your age. As investments are a long term strategy, if you’re younger, time’s your oyster and you can have a higher risk strategy as you shouldn’t need the money any time soon and so can hold out if your investments drop in value over the short term (1-5 years).

Whereas if you think you need the money back at some point soon, such as for a large purchase or even retirement, you might consider a lower risk investment strategy which aims to steadily increase your investment.

As part of our analysis into the best Stocks and Shares ISAs, we carried out a review of the investment performance of the 3 most popular investment apps: Wealthify, Nutmeg and Moneyfarm. And, we compared with the industry average.

We covered the last 5 years, and 4 categories: low risk, medium risk, higher risk and highest risk.

We’ll cover the results below, but overall, Nutmeg didn’t perform well. In all but the highest risk level they performed worse than the industry average, and across all risk categories, significantly worse than Moneyfarm (who wins every category).

Here’s the results, and for a full review, check out the best performing Stocks and Shares ISAs.

It’s worth noting investing is very difficult, that’s why we recommend using expert managed investment platforms. They’re here to use tried and tested investment strategies to grow your money over the long term. And Nutmeg does that.

However, as a trend, it does appear that other providers are growing their customer’s money a bit more (over the last 5 years). And over the long-term those small differences can add up to a big difference in your total balance.

As Nutmeg is built on exchange-traded funds (ETFs) that are relatively cheap fees wise, it means Nutmeg can offer you low fees too.

However, you’ll also be paying a fee on the investment funds your money is in (ETFs), and what’s known as market spread, which is a cost to buy and sell these funds.

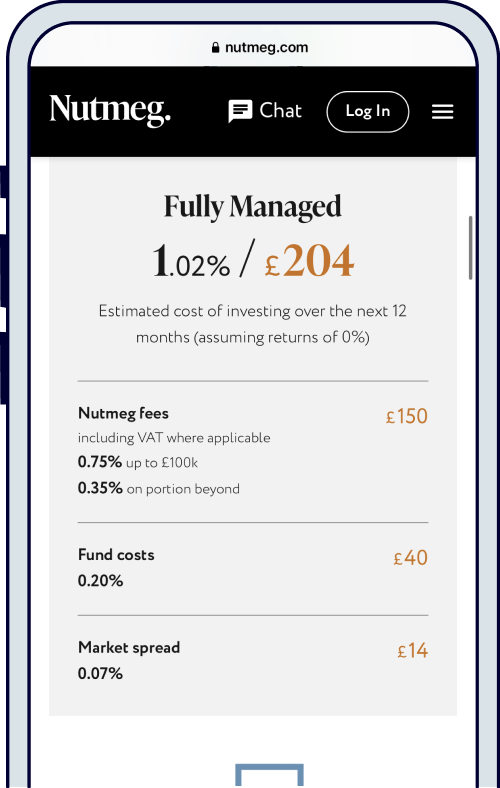

So, add all the fees together and that’s what you’ll ultimately pay. Just over 1% per year. Which is reasonable.

If you invested with an investment advisor (a real person) instead of Nutmeg, you’d be looking considerably more, as much as 5% on your initial investment and then ongoing management fees.

Here’s a full breakdown of the fees for each investment style:

Nutmeg fee: 0.75% up to 100k, 0.35% on the total after this.

Fund cost: 0.20%

Market spread: 0.07%

Nutmeg fee: 0.75% up to 100k, 0.35% on the total after this.

Fund cost: 0.25%

Market spread: 0.07%

Nutmeg fee: 0.45% up to 100k, 0.25% on the total after this.

Fund cost: 0.22%

Market spread: 0.07%

Nutmeg fee: 0.75% up to 100k, 0.35% on the total after this.

Fund cost: 0.28%

Market spread: 0.07%

However, in comparison with other digital investment providers, Nutmeg is one of the most expensive.

With Moneyfarm, fees start the same at 0.75% per year, but scale down as you save more, for instance if you have £20,000 saved, the fee is 0.65%, and this is applied to your whole balance. The fees also go as low as 0.35%.

With Beach, the annual management fee is 0.50%, however much you have invested.

And with Wealthify, the annual management fee is 0.60%, however much you have invested.

With Nutmeg, you have to save £100,000 before fees reduce, and they only reduce on the amount above that.

And with PensionBee, who just do pensions. The total fee is 0.75% (and reduces on larger balances), which includes all the investment fees too. Which is a very good deal. You can learn more about them with our PensionBee review, or check out the PensionBee website¹.

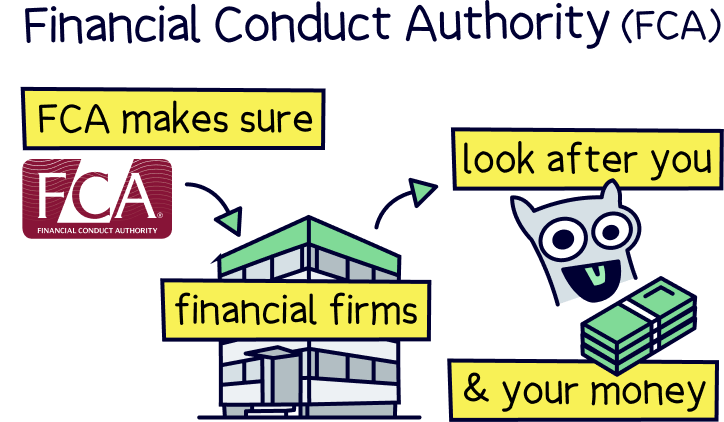

Yep! It’s perfectly safe to use Nutmeg. They are authorised by the Financial Conduct Authority (FCA), which means they’ve been approved and trusted to look after your money.

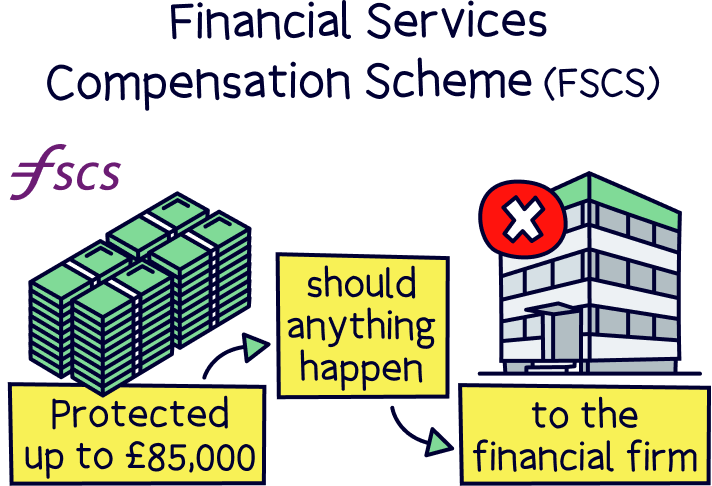

Your money is also protected by the Financial Services Compensation Scheme (FSCS). This means that should anything bad happen to Nutmeg, such as going out of business. You’ll get up to £85,000 back.

However, your money is actually held in the investments themselves, and these have extra protection. They’re held with the bank, J.P. Morgan, and are all in your name, and can only be returned back to you.

Here’s a recap of Nutmeg, and the pros and cons:

Nutmeg is rated 3.8 out of 5 on Trustpilot, the popular reviews website, from over 1,450 reviews. That’s not great compared to other companies. There’s a lot of complaints about customer service and the poor track record of investing. However the app itself is good, and gets good reviews.

What we really like about Nutmeg is it gives everybody the chance to invest their money, and build up their savings easily, simply and automatically. And everybody should!

But more than just the ability to invest, it has a great phone app and website to easily manage your accounts – providing easy access, and transparency to see how your money is performing over time.

The fees are reasonable, and transparent. Although there are cheaper options depending on how much you have invested, such as Beach¹, Moneyfarm and PensionBee (for pensions). In fact, Nutmeg is one of the most expensive digital wealth managers you’ll find.

Overall, we’re giving Nutmeg 3 stars. It’s good, but ultimately there’s better options out there. Ones that have a better track record of investing, have cheaper fees, easier to use, and have better socially responsible investment options. Plus, experts on hand to guide you through the process and answer any questions you might have.

We recommend checking out Beach¹ for investing and a pension, and PensionBee¹ just for pensions – they’re all of the above, and really great options.

Check out Beach. It's an easy to use app where the experts manage the investments. You can open both an ISA and a pension. The customer service is excellent too.

Check out Beach. It's an easy to use app where the experts manage the investments. You can open both an ISA and a pension. The customer service is excellent too.

Check out Beach. It's an easy to use app where the experts manage the investments. You can open both an ISA and a pension. The customer service is excellent too.

We’d love to hear from you, and it will help others too.

Christopher Dowling combines a communications degree with over 10 years experience in the financial services industry in London – with focus on educating people on a wide range of money topics in an easy to understand way. He writes about savings, investing, pensions, mortgages, insurance, banking, loans, business finance and other money topics.

This article was written, reviewed and fact checked by the expert team at Nuts About Money. You’re in safe hands. Learn more.

We're experts in all things money, with years of combined experience working in the finance industry and writing about money. We understand the ins and outs, how to get the best deals, save money, and how to communicate money in an easy to understand way (we hope you agree).

More than 20 years of combined experience researching and writing about money

Researched and reviewed a wide range of financial services companies, and have a transparent review process

We follow a strict editorial code to ensure you get the best information possible

Check out Beach. It's an easy to use app where the experts manage the investments. You can open both an ISA and a pension. The customer service is excellent too.